We issued an updated research report on Vale S.A. VALE on Mar 16.

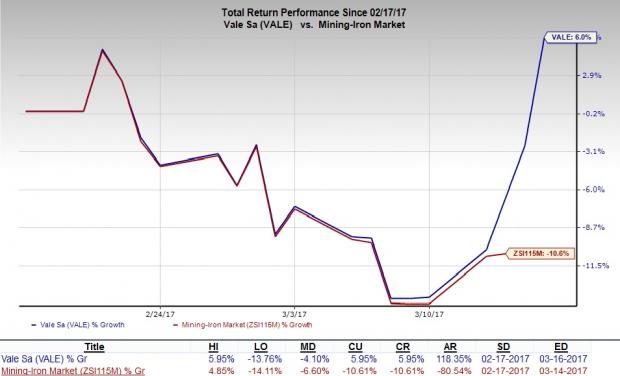

This Zacks Rank #1 (Strong Buy) stock looks bullish at the moment. Over the last one month, Vale’s shares yielded a return of 5.95%, as against the loss of 10.61% incurred by the Zacks categorized Mining-Iron industry.

Why Should You Pick this Stock?

Vale reported robust fourth-quarter 2016 results. The company noted that quarterly sales improved both on a sequential and year-over-year basis, backed by higher selling prices of products such as pellets, iron ore fines, nickel, copper and coal. Moreover, increased sales of fertilizers and ferrous minerals supported the top-line increment. Quarterly earnings also improved on the back of solid revenues.

Higher demand for core metals and gradual global economic recovery are expected to support the company’s top- and bottom-line growth in the quarters ahead.

Further, Vale has been trying to bring down its exploration and mining expenses by maximizing the productivity of major mines. The company is aimed at enhancing its production capacity by investing in new projects. Its major ferrous mineral and coal projects have either just commenced operations or are on the verge of completion.

For instance, the company’s new iron ore mine and processing plant, built under the Carajás Serra Sul S11D project, began its operations in third-quarter 2016. Also, the initial ramp-up of the new Moatize II coal mine was good in fourth-quarter 2016. Successful ramp-up and stable productivity of major mines are likely to boost Vale’s production capability. This will enable the company to capture increased mining market demand in the near term.

Vale implements a progressive dividend policy in its business, which reflects its commitment to increase shareholders’ wealth. It should be noted that the company’s lucrative dividend policy is supported by its superior capital management system. By investing in high-return growth opportunities, Vale aims to strengthen its cash position, which would enable it to offer attractive share buyback and dividend return programs to its shareholders.

Over the last 60 days, the Zacks Consensus Estimate for the stock moved north for both 2017 and 2018, reflecting positive market sentiments.

Other Stocks to Consider

Other favorably placed stocks within the industry are listed below:

The Chemours Company CC has a whopping average earnings surprise of 151.56% for the last four quarters and currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here .

Arconic Inc. ARNC , which also carries a Zacks Rank #2, has an average earnings surprise of 79.97% for the trailing four quarters.

Monsanto Company MON holds a Zacks Rank #2 and has an impressive average earnings surprise of 309.71% for the past four quarters.

More Stock News: 8 Companies Verge on Apple-Like Run

Did you miss Apple’s 9X stock explosion after they launched their iPhone in 2007? Now 2017 looks to be a pivotal year to get in on another emerging technology expected to rock the market. Demand could soar from almost nothing to $ 42 billion by 2025. Reports suggest it could save 10 million lives per decade which could in turn save $ 200 billion in U.S. healthcare costs.

A bonus Zacks Special Report names this breakthrough and the 8 best stocks to exploit it. Like Apple in 2007, these companies are already strong and coiling for potential mega-gains. Click to see them right now >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

VALE S.A. (VALE): Free Stock Analysis Report

Monsanto Company (MON): Free Stock Analysis Report

Chemours Company (The) (CC): Free Stock Analysis Report

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Plantations International