Scalper1 News

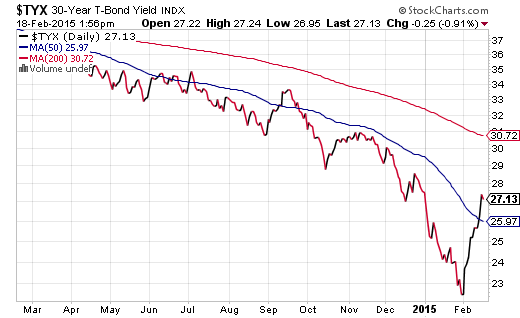

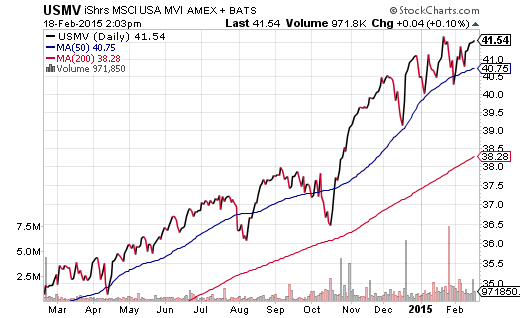

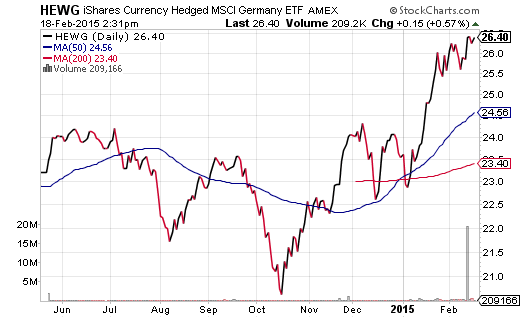

It is hard to believe just how many folks expect the U.S. stock market to rise substantially in the current environment. U.S. stocks and U.S. bonds are extremely overvalued. As long as one has a plan for exiting – rather than foolishly hoping-n-holding – one is able to minimize the risk of remaining invested in overvalued equities. Most people believe that Tom Cruise became an international superstar with the release of the action drama, “Top Gun” back in 1986. However, I remember the actor from an earlier film, “Risky Business.” The popular motion picture capitalized on teenage angst and harebrained ways to make money. In the film itself, the main character, Joel Goodson, turns his family home into a house of ill-repute to finance the repairs of his father’s Porsche – a car that he had been warned not to use, yet inadvertently destroyed. By the end of the movie, increasingly perilous behavior helped Joel get into Princeton, as opposed to him following a straighter-and-narrower path. Fans may recall the risk-taking tagline, “Sometimes you just gotta say, ‘What the Heck.'” In Hollywood, at least for the sake of on-screen comedy, irrational audacity may prove rewarding. In real life, however, investors tend to be compensated for taking reasonable risks. Granted, speculators can sometimes profit from bizarre decisions. Yet an investor who allows over-the-top exuberance to cloud sound judgment typically gets battered by panicky reversals of fortune. Indeed, it is hard to believe just how many folks expect the U.S. stock market to rise substantially in the current environment. Companies are not selling as much as they had anticipated as shown by rising manufacturer, wholesaler and retailer inventories. Companies in the S&P 500 are not profiting as much as executives had hoped either; analysts have been dramatically ratcheting down earnings expectations. Meanwhile, the parade of weak economic reports continue to flow in, from producer prices (excluding food and energy) registering an unexpected decline to smaller-than-expected gains in industrial production. Downward revisions to gross domestic product are a near certainty. What are the implications for the investing public? Sadly, it is a world where the two primary asset classes stateside – U.S. stocks and U.S. bonds – are extremely overvalued. And yet, the choices of how to manage the overvaluation in one’s portfolio are not particularly attractive either. Since there are no meaningful risk-free rates of return in a zero percent interest rate environment, investors have been choosing between risky and riskier alternatives. In one corner, expensive U.S. stocks may continue to appreciate on additional corporate buybacks as well as the possibility of economic acceleration. In the other corner, appallingly low-yielding U.S. bonds may produce total returns that exceed stocks due to the former’s relative value against developed world bonds; most of the developed world’s fixed-income yields are noticeably lower than comparable U.S. maturities. Of the two alternatives, I am still favoring long-term U.S. treasuries in client portfolios. The German 30-year bund yield is under 1%, while the Japanese 30-year is near 1.5%. As silly as those yields are, they are not likely to rise appreciably when the Bank of Japan (BOJ) and the European Central Bank (ECB) are in early stages of bond buying via quantitative easing exercises. Even more alarming? The 30-year yields for France, Canada and Italy are 1.45%, 2.12% and 2.61% respectively. We’re talking about fiscally irresponsible Italy having a lower yield than the U.S. at 2.71%. Does it not make sense to consider long-term U.S. bond exposure via the Vanguard Extended Duration Treasury ETF (NYSEARCA: EDV ) or the PIMCO 25+ Year Zero Coupon U.S. Treasury Index ETF (NYSEARCA: ZROZ ), especially when the 30-year yield has reverted back to a 50-day moving averages? Buying bond dips can be as rewarding as buying stock dips. The increasingly unattractive prospect of robust exposure to U.S. stocks has not kept me from sticking with the trends. My clients will continue to own funds like the iShares S&P 100 ETF (NYSEARCA: OEF ), the Health Care Select Sect SPDR ETF (NYSEARCA: XLV ), the Vanguard Mega Cap Growth ETF (NYSEARCA: MGK ) as well as the iShares MSCI USA Minimum Volatility ETF (NYSEARCA: USMV ) until there is a significant breach of the 200-day moving average on the downside. What-the-heck pricey? You bet. On the other hand, the market can remain insanely effervescent for a whole lot longer than an investor can accept 0% in a money market. As long as one has a plan for exiting – rather than foolishly hoping-n-holding – one is able to minimize the risk of remaining invested in overvalued equities. It is important to recognize, though, that stock uptrends in foreign markets come with lower P/E price-tags. Conservatively speaking, developed world stock assets trade at a 10%-15% P/E discount to the U.S., while broad-based emerging market stock assets may be trading at a 20% to 25% discount. It has been more difficult for me to embrace either the Vanguard FTSE Europe ETF (NYSEARCA: VGK ) or the Vanguard FTSE Emerging Markets ETF (NYSEARCA: VWO ) yet, as both have resistance at their respective 200-day trendlines and both do not have the currency-hedged exposure that I prefer at this moment. In contrast, I have advocated for several months on behalf of the iShares Currency Hedged MSCI Germany ETF (NYSEARCA: HEWG ) on the expectation that as the most successful exporter in the region, Germany will benefit the most from the battered euro. What’s more, HEWG’s uptrend is intact. Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

It is hard to believe just how many folks expect the U.S. stock market to rise substantially in the current environment. U.S. stocks and U.S. bonds are extremely overvalued. As long as one has a plan for exiting – rather than foolishly hoping-n-holding – one is able to minimize the risk of remaining invested in overvalued equities. Most people believe that Tom Cruise became an international superstar with the release of the action drama, “Top Gun” back in 1986. However, I remember the actor from an earlier film, “Risky Business.” The popular motion picture capitalized on teenage angst and harebrained ways to make money. In the film itself, the main character, Joel Goodson, turns his family home into a house of ill-repute to finance the repairs of his father’s Porsche – a car that he had been warned not to use, yet inadvertently destroyed. By the end of the movie, increasingly perilous behavior helped Joel get into Princeton, as opposed to him following a straighter-and-narrower path. Fans may recall the risk-taking tagline, “Sometimes you just gotta say, ‘What the Heck.'” In Hollywood, at least for the sake of on-screen comedy, irrational audacity may prove rewarding. In real life, however, investors tend to be compensated for taking reasonable risks. Granted, speculators can sometimes profit from bizarre decisions. Yet an investor who allows over-the-top exuberance to cloud sound judgment typically gets battered by panicky reversals of fortune. Indeed, it is hard to believe just how many folks expect the U.S. stock market to rise substantially in the current environment. Companies are not selling as much as they had anticipated as shown by rising manufacturer, wholesaler and retailer inventories. Companies in the S&P 500 are not profiting as much as executives had hoped either; analysts have been dramatically ratcheting down earnings expectations. Meanwhile, the parade of weak economic reports continue to flow in, from producer prices (excluding food and energy) registering an unexpected decline to smaller-than-expected gains in industrial production. Downward revisions to gross domestic product are a near certainty. What are the implications for the investing public? Sadly, it is a world where the two primary asset classes stateside – U.S. stocks and U.S. bonds – are extremely overvalued. And yet, the choices of how to manage the overvaluation in one’s portfolio are not particularly attractive either. Since there are no meaningful risk-free rates of return in a zero percent interest rate environment, investors have been choosing between risky and riskier alternatives. In one corner, expensive U.S. stocks may continue to appreciate on additional corporate buybacks as well as the possibility of economic acceleration. In the other corner, appallingly low-yielding U.S. bonds may produce total returns that exceed stocks due to the former’s relative value against developed world bonds; most of the developed world’s fixed-income yields are noticeably lower than comparable U.S. maturities. Of the two alternatives, I am still favoring long-term U.S. treasuries in client portfolios. The German 30-year bund yield is under 1%, while the Japanese 30-year is near 1.5%. As silly as those yields are, they are not likely to rise appreciably when the Bank of Japan (BOJ) and the European Central Bank (ECB) are in early stages of bond buying via quantitative easing exercises. Even more alarming? The 30-year yields for France, Canada and Italy are 1.45%, 2.12% and 2.61% respectively. We’re talking about fiscally irresponsible Italy having a lower yield than the U.S. at 2.71%. Does it not make sense to consider long-term U.S. bond exposure via the Vanguard Extended Duration Treasury ETF (NYSEARCA: EDV ) or the PIMCO 25+ Year Zero Coupon U.S. Treasury Index ETF (NYSEARCA: ZROZ ), especially when the 30-year yield has reverted back to a 50-day moving averages? Buying bond dips can be as rewarding as buying stock dips. The increasingly unattractive prospect of robust exposure to U.S. stocks has not kept me from sticking with the trends. My clients will continue to own funds like the iShares S&P 100 ETF (NYSEARCA: OEF ), the Health Care Select Sect SPDR ETF (NYSEARCA: XLV ), the Vanguard Mega Cap Growth ETF (NYSEARCA: MGK ) as well as the iShares MSCI USA Minimum Volatility ETF (NYSEARCA: USMV ) until there is a significant breach of the 200-day moving average on the downside. What-the-heck pricey? You bet. On the other hand, the market can remain insanely effervescent for a whole lot longer than an investor can accept 0% in a money market. As long as one has a plan for exiting – rather than foolishly hoping-n-holding – one is able to minimize the risk of remaining invested in overvalued equities. It is important to recognize, though, that stock uptrends in foreign markets come with lower P/E price-tags. Conservatively speaking, developed world stock assets trade at a 10%-15% P/E discount to the U.S., while broad-based emerging market stock assets may be trading at a 20% to 25% discount. It has been more difficult for me to embrace either the Vanguard FTSE Europe ETF (NYSEARCA: VGK ) or the Vanguard FTSE Emerging Markets ETF (NYSEARCA: VWO ) yet, as both have resistance at their respective 200-day trendlines and both do not have the currency-hedged exposure that I prefer at this moment. In contrast, I have advocated for several months on behalf of the iShares Currency Hedged MSCI Germany ETF (NYSEARCA: HEWG ) on the expectation that as the most successful exporter in the region, Germany will benefit the most from the battered euro. What’s more, HEWG’s uptrend is intact. Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

Scalper1 News