Scalper1 News

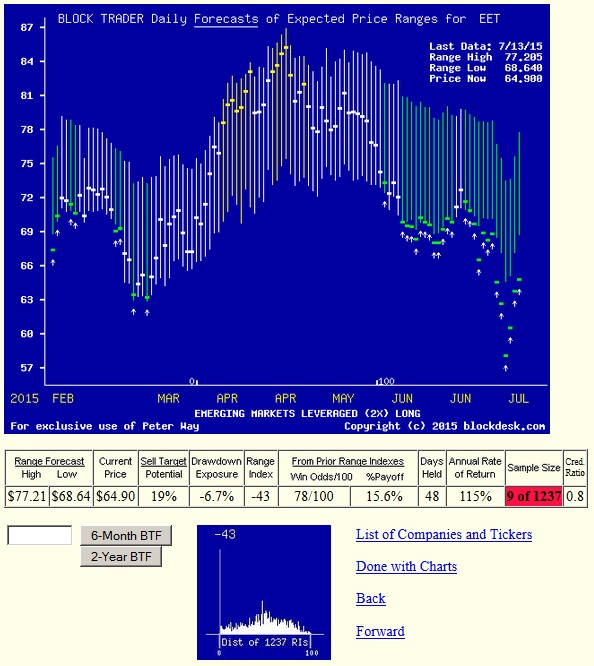

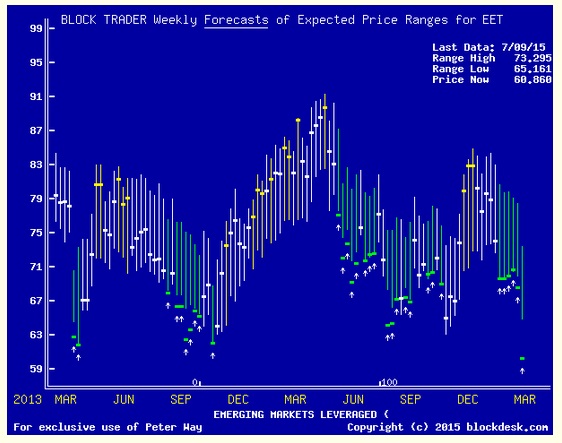

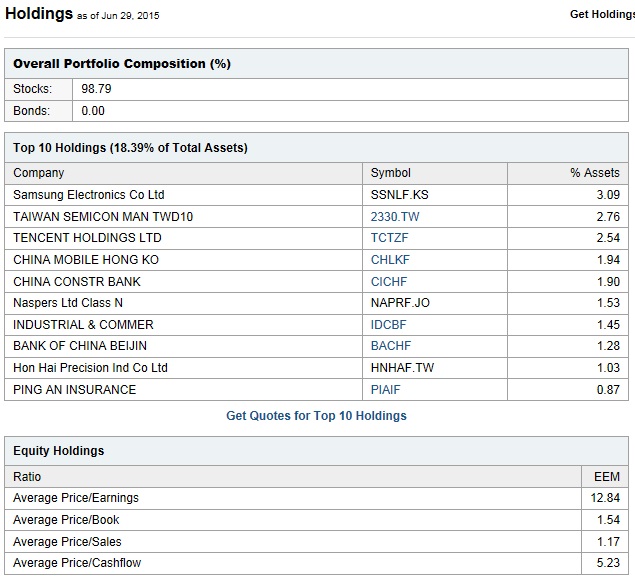

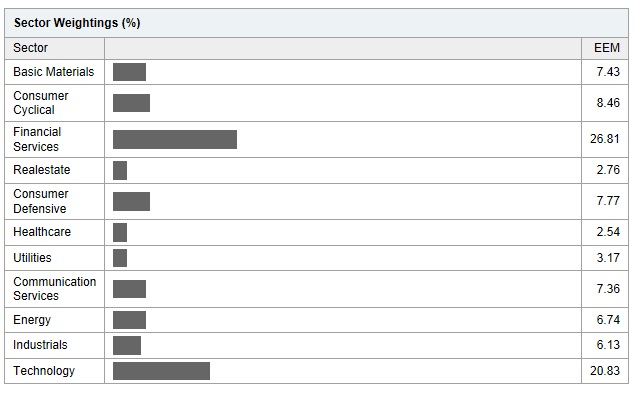

Summary From a population of some 350 actively-traded, substantial, and growing ETFs this is a currently attractive addition to a portfolio whose principal objective is wealth accumulation by active investing. We daily evaluate future near-term price gain prospects for quality, market-seasoned ETFs, based on the expectations of market-makers [MMs], drawing on their insights from client order-flows. The analysis of our subject ETF’s price prospects is reinforced by parallel MM forecasts for each of the ETF’s ten largest holdings. Qualitative appraisals of the forecasts are derived from how well the MMs have foreseen subsequent price behaviors following prior forecasts similar to today’s. Size of prospective gains, odds of winning transactions, worst-case price drawdowns, and marketability measures are all taken into account. Today’s most attractive ETF Is the ProShares Ultra MSCI Emerging Markets ETF (NYSEARCA: EET ). Yahoo Finance profiles this ETF as follows: The investment seeks daily investment results, before fees and expenses, that correspond to two times (2x) the daily performance of the MSCI Emerging Markets Index®. The fund invests in securities and derivatives that ProShare Advisors believes, in combination, should have similar daily return characteristics as two times (2x) the daily return of the index. The index includes 85% of free float-adjusted market capitalization in each industry group in emerging market countries. The fund is non-diversified. The fund currently holds assets of $37.5 million and has had a YTD price return of +1.9%. Its average daily trading volume of 14,205 produces a complete asset turnover calculation in 41 days at its current price of $64.90. A typical bid~offer spread is 0.6%. Behavioral analysis of market-maker hedging actions while providing market liquidity for volume block trades in the ETF by interested major investment funds has produced the recent past (6 month) daily history of implied price range forecasts pictured in Figure 1. Figure 1 (used with permission) The vertical lines of Figure 1 are a visual history of forward-looking expectations of coming prices for the subject ETF. They are NOT a backward-in-time look at actual daily price ranges, but the heavy dot in each range is the ending market quote of the day the forecast was made. What is important in the picture is the balance of upside prospects in comparison to downside concerns. That ratio is expressed in the Range Index [RI], whose number tells what percentage of the whole range lies below the then current price. Today’s Range Index is used to evaluate how well prior forecasts of similar RIs for this ETF have previously worked out. The size of that historic sample is given near the right-hand end of the data line below the picture. The current RI’s size in relation to all available RIs of the past 5 years is indicated in the small blue thumbnail distribution at the bottom of Figure 1. The first items in the data line are current information: The current high and low of the forecast range, and the percent change from the market quote to the top of the range, as a sell target. The Range Index is of the current forecast. Other items of data are all derived from the history of prior forecasts. They stem from applying a T ime- E fficient R isk M anagement D iscipline to hypothetical holdings initiated by the MM forecasts. That discipline requires a next-day closing price cost position be held no longer than 63 market days (3 months) unless first encountered by a market close equal to or above the sell target. The net payoffs are the cumulative average simple percent gains of all such forecast positions, including losses. Days held are average market rather than calendar days held in the sample positions. Drawdown exposure indicates the typical worst-case price experience during those holding periods. Win odds tells what percentage proportion of the sample recovered from the drawdowns to produce a gain. The cred(ibility) ratio compares the sell target prospect with the historic net payoff experiences. Figure 2 provides a longer-time perspective by drawing a once-a week look from the Figure 1 source forecasts, back over two years. Figure 2 (used with permission) What does this ETF hold, causing such price expectations? Figure 3 is a table of securities held by the subject ETF, indicating its concentration in the top ten largest holdings, and their percentage of the ETF’s total value. Figure 3 (click to enlarge) Source: Yahoo Finance This shows how leveraged ETFs do their magic. The top ten holdings of EET are mainly swaps contracts in the iShares MSCI Emerging Markets ETF (NYSEARCA: EEM ), with a value per share of 184.57% of the EET share. The 4.01% in bonds helps balance out the 2x relationship of price change in EET with the underlying Emerging Markets Index security. But that doesn’t tell much about what the investor has driving his investment. To find that out, we look at the holdings of EEM: Source: Yahoo Finance That’s better, and shows the emphasis on Financial Services and Technology, making up almost half of the portfolio. Unfortunately, the offshore nature of virtually all the underlying equity holdings are ones that we do not have information support from arbitrage activities in derivative markets, so our analysis of this dimension of EET must stop here. In markets as unpredictably dynamic as this, wide variations in market experience seem to be the rule. A comparison of the data row for EET from Figure 1 with a similar one from an ETF proxy for the U.S. market helps to highlight the unique and attractive features of EET. For EET: For the SPDR S&P 500 Trust ETF (NYSEARCA: SPY ) : The Sell Target for EET offers 3 times as much potential gain as the U.S. market proxy, SPY. But it exposes the investor to worst-case price drawdown exposure that is more than twice as large. Still, taking Sell Target and Drawdown as Reward and Risk elements, EET is favored with a ratio of 3 to 1, rather than SPY’s 2 to 1. Just as importantly, the ability to recover from extreme price drawdowns and achieve some or all of the upside potential is indicated by each one’s Win Odds out of 100. For the U.S. market proxy that desired objective has been accomplished 7 out of every 8 times. EET has achieved it a bit better than 6 out of 8. But the payoff for EET at a net (including losses) average of +15.6% is 5 times bigger than the U.S. market’s +3.5%. Since both alternative investments took 9-10 weeks to achieve their gains, the Annual Rates of Return [AROR] from price change gains is also 5 times better, 115% to 21%. EET’s relatively small sample of prior experiences, only 9 in the past 5 years is not surprising or troubling, given its presently depressed price, relative to its forecast. That is measured by its Range Index. When negative, it tells by how much the current market quote is below the least justifiable forecast price. Here a -43 means it is cheap by nearly half its total forecast price range. The U.S. market proxy, on the other hand is presently priced right about at its mid-point, with only slightly more upside than downside. A quick reference to the small thumbnail picture in Figure 1, of the past 5 years distribution of Range indexes, emphasizes how extreme (and opportune) is the current pricing. Conclusion EET provides attractive forecast price gains, supported by a recognized index of major established investments in emerging countries. The daily forecast graphic and its weekly extracts over the longer period of two years demonstrate the cyclic nature of the ETF. Its dynamic character offers an opportune point in time to take advantage of world events that may be distracting investors’ attention from the potentials presented here. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Scalper1 News

Summary From a population of some 350 actively-traded, substantial, and growing ETFs this is a currently attractive addition to a portfolio whose principal objective is wealth accumulation by active investing. We daily evaluate future near-term price gain prospects for quality, market-seasoned ETFs, based on the expectations of market-makers [MMs], drawing on their insights from client order-flows. The analysis of our subject ETF’s price prospects is reinforced by parallel MM forecasts for each of the ETF’s ten largest holdings. Qualitative appraisals of the forecasts are derived from how well the MMs have foreseen subsequent price behaviors following prior forecasts similar to today’s. Size of prospective gains, odds of winning transactions, worst-case price drawdowns, and marketability measures are all taken into account. Today’s most attractive ETF Is the ProShares Ultra MSCI Emerging Markets ETF (NYSEARCA: EET ). Yahoo Finance profiles this ETF as follows: The investment seeks daily investment results, before fees and expenses, that correspond to two times (2x) the daily performance of the MSCI Emerging Markets Index®. The fund invests in securities and derivatives that ProShare Advisors believes, in combination, should have similar daily return characteristics as two times (2x) the daily return of the index. The index includes 85% of free float-adjusted market capitalization in each industry group in emerging market countries. The fund is non-diversified. The fund currently holds assets of $37.5 million and has had a YTD price return of +1.9%. Its average daily trading volume of 14,205 produces a complete asset turnover calculation in 41 days at its current price of $64.90. A typical bid~offer spread is 0.6%. Behavioral analysis of market-maker hedging actions while providing market liquidity for volume block trades in the ETF by interested major investment funds has produced the recent past (6 month) daily history of implied price range forecasts pictured in Figure 1. Figure 1 (used with permission) The vertical lines of Figure 1 are a visual history of forward-looking expectations of coming prices for the subject ETF. They are NOT a backward-in-time look at actual daily price ranges, but the heavy dot in each range is the ending market quote of the day the forecast was made. What is important in the picture is the balance of upside prospects in comparison to downside concerns. That ratio is expressed in the Range Index [RI], whose number tells what percentage of the whole range lies below the then current price. Today’s Range Index is used to evaluate how well prior forecasts of similar RIs for this ETF have previously worked out. The size of that historic sample is given near the right-hand end of the data line below the picture. The current RI’s size in relation to all available RIs of the past 5 years is indicated in the small blue thumbnail distribution at the bottom of Figure 1. The first items in the data line are current information: The current high and low of the forecast range, and the percent change from the market quote to the top of the range, as a sell target. The Range Index is of the current forecast. Other items of data are all derived from the history of prior forecasts. They stem from applying a T ime- E fficient R isk M anagement D iscipline to hypothetical holdings initiated by the MM forecasts. That discipline requires a next-day closing price cost position be held no longer than 63 market days (3 months) unless first encountered by a market close equal to or above the sell target. The net payoffs are the cumulative average simple percent gains of all such forecast positions, including losses. Days held are average market rather than calendar days held in the sample positions. Drawdown exposure indicates the typical worst-case price experience during those holding periods. Win odds tells what percentage proportion of the sample recovered from the drawdowns to produce a gain. The cred(ibility) ratio compares the sell target prospect with the historic net payoff experiences. Figure 2 provides a longer-time perspective by drawing a once-a week look from the Figure 1 source forecasts, back over two years. Figure 2 (used with permission) What does this ETF hold, causing such price expectations? Figure 3 is a table of securities held by the subject ETF, indicating its concentration in the top ten largest holdings, and their percentage of the ETF’s total value. Figure 3 (click to enlarge) Source: Yahoo Finance This shows how leveraged ETFs do their magic. The top ten holdings of EET are mainly swaps contracts in the iShares MSCI Emerging Markets ETF (NYSEARCA: EEM ), with a value per share of 184.57% of the EET share. The 4.01% in bonds helps balance out the 2x relationship of price change in EET with the underlying Emerging Markets Index security. But that doesn’t tell much about what the investor has driving his investment. To find that out, we look at the holdings of EEM: Source: Yahoo Finance That’s better, and shows the emphasis on Financial Services and Technology, making up almost half of the portfolio. Unfortunately, the offshore nature of virtually all the underlying equity holdings are ones that we do not have information support from arbitrage activities in derivative markets, so our analysis of this dimension of EET must stop here. In markets as unpredictably dynamic as this, wide variations in market experience seem to be the rule. A comparison of the data row for EET from Figure 1 with a similar one from an ETF proxy for the U.S. market helps to highlight the unique and attractive features of EET. For EET: For the SPDR S&P 500 Trust ETF (NYSEARCA: SPY ) : The Sell Target for EET offers 3 times as much potential gain as the U.S. market proxy, SPY. But it exposes the investor to worst-case price drawdown exposure that is more than twice as large. Still, taking Sell Target and Drawdown as Reward and Risk elements, EET is favored with a ratio of 3 to 1, rather than SPY’s 2 to 1. Just as importantly, the ability to recover from extreme price drawdowns and achieve some or all of the upside potential is indicated by each one’s Win Odds out of 100. For the U.S. market proxy that desired objective has been accomplished 7 out of every 8 times. EET has achieved it a bit better than 6 out of 8. But the payoff for EET at a net (including losses) average of +15.6% is 5 times bigger than the U.S. market’s +3.5%. Since both alternative investments took 9-10 weeks to achieve their gains, the Annual Rates of Return [AROR] from price change gains is also 5 times better, 115% to 21%. EET’s relatively small sample of prior experiences, only 9 in the past 5 years is not surprising or troubling, given its presently depressed price, relative to its forecast. That is measured by its Range Index. When negative, it tells by how much the current market quote is below the least justifiable forecast price. Here a -43 means it is cheap by nearly half its total forecast price range. The U.S. market proxy, on the other hand is presently priced right about at its mid-point, with only slightly more upside than downside. A quick reference to the small thumbnail picture in Figure 1, of the past 5 years distribution of Range indexes, emphasizes how extreme (and opportune) is the current pricing. Conclusion EET provides attractive forecast price gains, supported by a recognized index of major established investments in emerging countries. The daily forecast graphic and its weekly extracts over the longer period of two years demonstrate the cyclic nature of the ETF. Its dynamic character offers an opportune point in time to take advantage of world events that may be distracting investors’ attention from the potentials presented here. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Scalper1 News

Scalper1 News