Tag Archives: undefined

Canada And USA Have Lazy Investors And How To Avoid It By Following Buffett’s Method Of Finding, Analyzing And Valuing Stocks

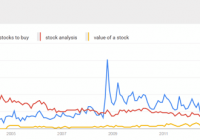

Summary Why most investors get lazy. Interesting data on which country has lazy investors. 7 Ways that Buffett finds, analyzes and values stocks. I definitely have lazy areas. When it’s cold and raining, I don’t want to take my dogs out to the park where they’ll get wet and muddy and I end up having to bathe them. Being in Seattle, it’s a huge hassle during the winter months where it drizzles constantly. So I have a lazy man’s way of giving them exercise. Playing fetch up and down a flight of stairs Hiding treats inside their ball and then playing fetch Setting up a fake grass patch on the balcony for them to do their business But don’t you find that this is so similar to what we do when it comes to investing? Instead of performing the daily practice of finding companies, going through their financials or numbers, reading reports and making a decisions, we tend to take the lazy man’s approach to investing. Copying other people’s ideas Looking for stocks to buy, instead of looking at ways to improve processes Buying a tiny position of 30-40 stocks to diversify against ignorance Investing is hard. But the process and rewards are worth it if practiced regularly. I’ve been writing regularly on this blog since 2008. That’s 7 years of writing one or more articles a week at an average of over 1000 words per article. But even after 7 years, if I go a week or two without writing, my brain feels slow. When I don’t go through financial statements for a week, or fall out of rhythm in reading reports, the speed at which I pick up information feels very sluggish. And when my head feels drained and slow, what do I feel like doing? I start looking for short cuts and easy ways out. But I take pride in being a value investor and doing the work when picking stocks. It’s not the same for everyone though. If you’re reading this blog, it’s because you like to learn about investing and enjoying being empowered to value your own stocks without seeking others’ approval. Take a look at these interesting trends on investor sentiment by comparing 3 approaches. stocks to buy stock analysis value a stock (click to enlarge) Stocks to Buy The huge blue spike is from the 2008 and it’s actually very interesting to see how many people were looking for stocks to buy during the crash. But you can also see how much more volume there is (not surprisingly) compared to “stock analysis” and “value of a stock”. The interest also looks to be going up with plenty of interest in 2014 and 2015. Based on the latest data from Google Trends, most of the queries on “stocks to buy” is coming from Canada and USA. (click to enlarge) Stock Analysis Going back to the line chart, the interest for stock analysis looks to be steady with a slow downtrend. I’m not surprised because most people don’t care about analyzing a stock . Even though analyzing and valuation is more important than ever. You can even download a collection of investment checklists , but anything that requires work will see a downtrend over time. What’s surprising is where all the interest comes from. (click to enlarge) People in Bangladesh and India make up the bulk of the data but I’ve also found that I get a lot of emails and questions from Indian investors with strong desires to learn. Value a Stock Stock analysis and valuing stocks should go hand in hand right? Not so fast. (click to enlarge) It’s back to the USA on how to value a stock. And this is my biggest surprise because valuing a stock and stock analysis go together. You can’t value a stock 100% effectively unless you’ve analyzed the company. Or it could be people in the US are more interested in knowing what stock to buy and at what price, while people in India are more interested in learning the process. Either way, it goes to show how one dimensional the thought process of a human can be. The Investor Trait “Just tell me what to buy” “Show me how to analyze stocks” “I just want to know what this stock is worth” Goes to show how difficult stock picking really is because you first have to find something that looks good enough to buy, know how to analyze it to come to an intrinsic value. Something like this. (click to enlarge) I find zone 1 to be the worst. It’s where all the superficial articles live and you see a ton of these noisy ones everywhere. The ones based recapping what earnings came out to be compared to analyst expectations because of competition and blah blah. Zone 2 is the area where I tend to live most of the time. I have plenty of stock ideas but before I get to any analyzing I want to make sure that the numbers make sense before I put in the time to start reading reports and analyzing the details. Zone 3 is even better when instead of working on so many ideas, the investors that party in this block are very focused on understanding a stock completely. The best investors and gurus live here. And then there’s zone 4 . In any sport, there’s always a sweet spot. Whether it’s in your golf club, tennis racket or bat, the one spot where everything works in harmony. A place that I want to be. Who doesn’t? In Buffett’s prime, he easily waltzed around zone 4. He and his band of super investors dominated this territory and if you’ve read his letters, it’s not hard to see why and thankfully, we have Buffett’s wisdom on picking stocks from decades of experience. What would Buffett do in this market? Well here’s a collection of Buffett’s thoughts on how he goes about analyzing and valuing stocks. 7 Wise Thoughts from Buffett on Finding Stocks 1. I started at page one [of these manuals] and went through every company that traded, from A to Z. When I was done I knew something about every company in the book. 2. I like businesses that I can understand. Let’s start with that. That narrows it down by 90%. There are all types of things I don’t understand, but fortunately, there is enough I do understand. You have this big wide world out there and almost every company is publicly owned. So you have all American business practically available to you. So it makes sense to go with things you can understand. 3. First, you need two piles. You have to segregate businesses you can understand and reasonably predict from those you don’t understand and can’t reasonably predict. An example is chewing gum versus software. You also have to recognize what you can and cannot know. Put everything you can’t understand or that is difficult to predict in one pile. That is the too-hard pile. Once you know the other pile, then it’s important to read a lot, learn about the industries, get background information, etc. on the companies in those piles. Read a lot of 10Ks and Qs, etc. Read about the competitors. I don’t want to know the price of the stock prior to my analysis. I want to do the work and estimate a value for the stock and then compare that to the current offering price. If I know the price in advance it may influence my analysis. We’re getting ready to make a $5 billion investment and this was the process I used. 4. You have to turn over a lot of rocks to find those little anomalies. You have to find the companies that are off the map – way off the map. You may find local companies that have nothing wrong with them at all 5. Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well. 6. I don’t look to jump over 7-foot bars: I look around for 1-foot bars that I can step over. 7. If we were to do it over again, we’d do it pretty much the same way. The world hasn’t changed that much. We’d read everything in sight about businesses and industries we think we’d understand. And, working with far less capital, our investment universe would be far broader than it is currently. 7 Gems from Buffet on Analyzing Stocks 1. You don’t need to be an expert in order to achieve satisfactory investment returns. But if you aren’t, you must recognize your limitations and follow a course certain to work reasonably well. Keep things simple and don’t swing for the fences. When promised quick profits, respond with a quick “no.” 2. There’s nothing different, in my view, about analyzing securities today vs. 50 years ago. 3. We favor businesses where we really think we know the answer. If we think the business’s competitive position is shaky, we won’t try to compensate with price. We want to buy a great business, defined as having a high return on capital for a long period of time, where we think management will treat us right. We like to buy at 40 cents on the dollar, but will pay a lot closer to $1 on the dollar for a great business. 4. Munger: Margin of safety means getting more value than you’re paying. There are many ways to get value. It’s high school algebra; if you can’t do this, then don’t invest. 5. If you’re going to buy a farm, you’d say, “I bought it to earn $X growing soybeans.” It wouldn’t be based on what you saw on TV or what a friend said. It’s the same with stocks. Take out a yellow pad and say, “If I’m going to buy GM at $30, it has 600 million shares, so I’m paying $18 billion,” and answer the question, why? If you can’t answer that, you’re not subjecting it to business tests. 6. Capital-intensive industries outside the utility sector scare me more. We get decent returns on equity. You won’t get rich, but you won’t go broke either. You are better off in businesses that are not capital intensive. 7. No formula in finance tells you that the moat is 28 feet wide and 16 feet deep. That’s what drives the academics crazy. They can compute standard deviations and betas, but they can’t understand moats. Maybe I’m being too hard on the academics. 7 Nuggets from Buffett on Valuing Stocks 1. When Charlie and I buy stocks which we think of as small portions of businesses our analysis is very similar to that which we use in buying entire businesses. We first have to decide whether we can sensibly estimate an earnings range for five years out, or more. If the answer is yes, we will buy the stock (or business) if it sells at a reasonable price in relation to the bottom boundary of our estimate. If, however, we lack the ability to estimate future earnings which is usually the case we simply move on to other prospects. In the 54 years we have worked together, we have never foregone an attractive purchase because of the macro or political environment, or the views of other people. In fact, these subjects never come up when we make decisions. 2. In 1986, I purchased a 400-acre farm, located 50 miles north of Omaha, from the FDIC. It cost me $280,000, considerably less than what a failed bank had lent against the farm a few years earlier. I knew nothing about operating a farm. But I have a son who loves farming, and I learned from him both how many bushels of corn and soybeans the farm would produce and what the operating expenses would be. From these estimates, I calculated the normalized return from the farm to then be about 10%. I also thought it was likely that productivity would improve over time and that crop prices would move higher as well. Both expectations proved out. 3. Intrinsic value is terribly important but very fuzzy. We try to work with businesses where we have fairly high probability of knowing what the future will hold. If you own a gas pipeline, not much is going to go wrong. Maybe a competitor enters forcing you to cut prices, but intrinsic value hasn’t gone down if you already factored this in. We looked at a pipeline recently that we think will come under pressure from other ways of delivering gas [to the area the pipeline serves]. We look at this differently from another pipeline that has the lowest costs [and does not face threats from alternative pipelines]. If you calculate intrinsic value properly, you factor in things like declining prices. 4. Investors making purchases in an overheated market need to recognize that it may often take an extended period for the value of even an outstanding company to catch up with the price they paid. 5. We use the same discount rate across all securities. We may be more conservative in estimating cash in some situations. 6. Just because interest rates are at 1.5% doesn’t mean we like an investment that yields 2-3%. We have minimum thresholds in our mind that are a whole lot higher than government rates. When we’re looking at a business, we’re looking at holding it forever, so we don’t assume rates will always be this low. 7. The appropriate multiple for a business compared to the S&P 500 depends on its return on equity and return on incremental invested capital. I wouldn’t look at a single valuation metric like relative P/E ratio. I don’t think price-to-earnings, price-to-book or price-to-sales ratios tell you very much. People want a formula, but it’s not that easy. To value something, you simply have to take its free cash flows from now until kingdom come and then discount them back to the present using an appropriate discount rate. All cash is equal. You just need to evaluate a business’s economic characteristics. More Reading Most of these quotes came from Buffett FAQ which contains the Q&A from shareholder meetings and goes beyond what you’ll find in the annual letters. Just from these small selection of quotes, you can see how Buffett manages to dance in zone 4. Take his words to heart and let’s join him on the dance floor because the sweet spot is where we belong. Question for You What zone do you think you are in and what is one area that you want to get better at to be the ultimate zone 4 investor? Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Catalyst To Convert Fourth Hedge Fund, Acquire SMA Business

By DailyAlts Staff Catalyst Funds has already converted three hedge funds into mutual funds, including the Catalyst Hedged Futures Strategy Fund (MUTF: HFXAX ), which was in the top 12% of funds in Morningstar’s Managed Futures category for the first half of 2015. On July 31, the firm will add a fourth former hedge fund to its lineup of liquid alts, when it converts Auctos Capital Management’s managed futures strategy into a ’40 Act fund. The new fund will be called the Catalyst/Auctos Managed Futures Multi-Strategy Fund. “With this transaction, Catalyst is bringing a successful managed futures strategy to the retail market,” said Catalyst CEO Jerry Szilagyi, in a July 28 press release. “This strategy is another example of our ‘intelligent alternative’ investment approach and we’re proud to add the accomplished Auctos investment team to the Catalyst family.” The fund conversion comes as the result of Catalyst’s acquisition of Auctos, which not only includes its managed-futures strategy hedge fund, but also its separately managed accounts (NYSE: SMA ) business. Catalyst will take on the SMA business as a wholly owned subsidiary and continue to operate it under the Auctos name. The firm will also take on five Auctos employees, including Auctos president Kevin Jamali, who will continue to be portfolio manager of the new mutual fund and head of the SMA subsidiary. “We are thrilled to join the Catalyst team and to bring our investment strategy to the retail marketplace,” said Mr. Jamali. He and his four colleagues, which include two PhDs, will continue to work out of Auctos’s Chicago office. Both firms stand to benefit from the acquisition. While Auctos will benefit from what Mr. Jamali calls a “vast operational and distribution infrastructure,” Catalyst will expand its investment management and research capabilities, according to Mr. Szilagyi. For more information, visit catalystmf.com . Share this article with a colleague