Ivy Portfolio August Update

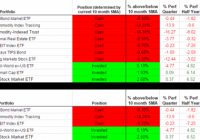

The Ivy Portfolio spreadsheet tracks the 10-month moving average signals for two portfolios listed in Mebane Faber’s book, The Ivy Portfolio: How to Invest Like the Top Endowments and Avoid Bear Markets . Faber discusses 5, 10, and 20 security portfolios that have trading signals based on long-term moving averages. The Ivy Portfolio spreadsheet tracks both the 5 and 10 ETF portfolios listed in Faber’s book. When a security is trading below its 10-month simple moving average, the position is listed as “Cash”. When the security is trading above its 10-month simple moving average, the positions is listed as “Invested”. The spreadsheet’s signals update once daily (typically in the late evening) using the dividend/split adjusted closing price from Yahoo Finance. The 10-month simple moving average is based on the most recent 10 months, including the current month’s most recent daily closing price. Even though the signals update daily, it is not an endorsement to check signals daily or trade based on daily updates. It simply gives the spreadsheet more versatility for users to check at his or her leisure. The page also displays the percentage each ETF within the Ivy 10 and Ivy 5 Portfolio is above or below the current 10-month simple moving average, using both adjusted and unadjusted data. If an ETF has paid a dividend or split within the past 10 months, then when comparing the adjusted/unadjusted data you will see differences in the percent an ETF is above/below the 10-month SMA. This could also potentially impact whether an ETF is above or below its 10-month SMA. Regardless of whether you prefer the adjusted or unadjusted data, it is important to remain consistent in your approach. My preference is to use adjusted data when evaluating signals. The current signals based on July 31st’s adjusted closing prices are below. This month the Vanguard Total Bond Market ETF (NYSEARCA: BND ), the SPDR Dow Jones International Real Estate ETF (NYSEARCA: RWX ), the Vanguard FTSE Emerging Markets ETF (NYSEARCA: VWO ), the PowerShares DB Commodity Index Tracking ETF (NYSEARCA: DBC ), the iShares S&P GSCI Commodity-Indexed Trust ETF (NYSEARCA: GSG ), the Vanguard REIT Index ETF (NYSEARCA: VNQ ) and the iShares TIPS Bond ETF (NYSEARCA: TIP ) are below their 10-month moving average. The spreadsheet also provides quarterly, half yearly, and yearly return data courtesy of Finviz. The return data is useful for those interested in overlaying a momentum strategy with the 10-month SMA strategy: (click to enlarge) I also provide a “Commission-Free” Ivy Portfolio spreadsheet as an added bonus. This document tracks the 10-month moving averages for four different portfolios designed for TD Ameritrade, Fidelity, Charles Schwab, and Vanguard commission-free ETF offers. Not all ETFs in each portfolio are commission free, as each broker limits the selection of commission-free ETFs and viable ETFs may not exist in each asset class. Other restrictions and limitations may apply depending on each broker. Below are the 10-month moving average signals (using adjusted price data) for the commission-free portfolios: (click to enlarge) (click to enlarge) Disclosure: None