Dog-Day Summer: Scratch The VIX Fleas

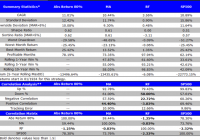

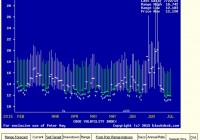

Summary On a go-nowhere market day in mid-summer, the institutional investment management “B” teams are in charge under the remote watchful eyes of the vacationing “A” managers. An SA contributor perfectly times a clearly-written explanation of how several VIX-index derivatives do their thing, presenting numerous onlookers intellectual advancement opportunities for money-making insights. Eager observer participation comments encourage a demonstration of crowd-source strength that makes Seeking Alpha a stand-apart site of internet information exchange. Adding to the present contributions, this article provides a behavioral analysis dimension to the discussion, digging deeper into what makes the securities markets game challenging. Market-makers [MMs] use the VIX in ways that provide expanding opportunities for individual investors to gain market outlook perspective. New ones are about to arrive. The Market-makers’ Game Playbook It’s a game because everyone’s outcomes depend on someone else’s actions. Both initially (opening a position) and ultimately (closing the position) require an other side of the trade. It’s a great game, because we can’t be sure what that guy (or guys, and gals) are going to do next. Lots of game strategies can work, and are continually in play. Plenty of action in a trillion-dollar-a day market. But which way is the emphasis heading, enthusiasm or caution, greed or fear? Who knows what evil lurks in the hearts of men? Heh-heh-heh. The VIX knows! And because its calculation is rigidly defined and regularly measured, it is constantly watched. It is an objective appraisal of the most subjective element in the game. Starting 7/23/2015 additional coloration will enrich the speculative confusion. The VIX index is calculated from premiums paid for options on near expiration contracts on the S&P 500 index. Caution! Objects in this mirror are closer than they may appear! Those contracts have expirations with monthly granulations. But on 7/23 futures and options start trading in the VIX with weekly expirations. Why? Market professionals are consummate hedgers, hate risk, unless they get paid (extravagantly?) for bearing it. In the process, time has profound value. Hedging markets for equity securities have all-along had an inverted “yield curve.” Back in the old days of economically honest (non-governmental interference) markets for “risk-free” U.S. Government Treasury Debt securities, short duration obligations – bills – would carry small interest costs. Obligations with longer periods of time before the investor has his principal returned, paid larger yields. Logically, the more time before you got your bait back, the more likely something might go wrong. You need to be paid for that risk. It still works that way, but now the curve between 30 days and 30 years is a lot flatter. Not so in street equity financing. Market capital typically has huge return potentials in the immediate time frame. Every last scrap of capital that can be declared and committed earns something at the measurement hour. Street capital is required by means of “haircuts” to be reserved, unproductive, against potential disaster. The crisis of 2008 made the dangers clear. The cost of raising capital to meet regulatory requirements makes immediate capital availability dear, while long-term (days, weeks) capital is far less demanding, cheaper. If a hedger can arb a position with a one-week security instead of a one-month one, it is like found money. So the game rules are being eased, and weekly VIX expirations are coming. All very rational. But it may also be very informative. Or not; we really can’t be sure. Here is the CBOE’s official statement : VIX Weeklys futures began trading at CBOE Futures Exchange (CFE®) on July 23. VIX Weeklys options are expected to begin trading at Chicago Board Options Exchange, Incorporated (CBOE®) shortly thereafter. What do we know now? The VIX index tells the amount of uncertainty present in the prices of options on the S&P 500 Index (SPX). But it cannot distinguish any directional balance between upside and downside in that uncertainty. In fact, changes in the size of the VIX calculation are a resultant of the behavior of investors, not in themselves a forecaster of behavior. Observers have learned that fearful investor actions cause the VIX to rise, and reflections of comfort and reassurance cause it to diminish. When the VIX is high, it is because investor concerns are already high, usually because stock prices have already dropped some. How much worse it might get is hard to tell, since that bound has been erratic. The comfort side of the proposition is much more clearly defined and more frequently visited at 10 to 12. The introduction of options trading in the VIX Index in February of 2006 gave us the ability to apply to the VIX the insight we have in appraising the investor expectations we have for individual stocks and ETFs. The balance of expectations between upside and downside prospects measured by the Range Index became available to the VIX in 2006. We achieved the ability to forecast the directional inclination of what many observers took to be a forecasting device itself. A forecast of the forecast. But it hasn’t been the magic many have hoped for. Here are recent measures of the price range implications for the VIX, daily for 6 months in Figure 1, and once a week samples of that weekly for the past 2 years in Figure 2. Figure 1 (used with permission) Figure 2 (used with permission) It should be apparent that market professionals have a good sense of when investor confidence is high, because then the VIX is low in its expectations range, seen as green in these pictures. Prior experience since 2006 has been similar to these at the low extreme, and only more aggravated, but still irregular, on the high side. The small thumbnail picture at the bottom of Figure 2 shows what the distribution of VIX RIs has been daily over the past 5 years. The shape of its distribution is heavily skewed to the low end of a normal stock’s typical, fairly symmetrical, bell-shaped curve experience. The scarcity of VIX pricings at or above a mid-RI level (where prospects for market decline are as great as for price increase) should be a reassurance that markets still remember having grabbed the hot end of the match in 2008. But the RI distribution before the past 5 years is just as healthy, because there had been bad market experiences previously, and they too were remembered. In all, the evidences of U.S. equity market functionality over the past few decades are quite reassuring, largely because of its demonstrated recovery capacity. At the heart of that capacity is the market-making community’s self-protective instincts and its arbitrage skills in making risk-reward tradeoffs. Risks usually can not be eliminated, but can be transferred to those with the capacity to bear them, if appropriate price tags are attached. This is the heart of the insurance concept. This only breaks down when widespread fraud permeates the system, as was the case with mortgage-backed securities in 2007-2008. That was on a scale large enough to threaten the entire financial system and damaged important parts of it badly. Forecasting the “forecaster” We have the ability to infer when the VIX is at comfortable levels and to know when it has jumped to altitudes unlikely to be sustained. Can we make money with that knowledge? Let’s take a closer look at the VIX’s own price behavior following the presence of various levels of Range Indexes. Figure 3 shows what that has been over the past 4-5 years: Figure 3 (click to enlarge) The VIX Range Indexes currently indicated in Figures 1 and 2 are right at the bottom of a normal expectations range, with all upside “reward” and no downside “risk.” In Figure 3 that is indicated by the magenta color of the count of past RIs with similar RWD:RSK balances of 100:1. The blue 1 : 1 row is an average of all 1130 observations from 1/19/11 to 7/22/2015, cumulated from progressive rows above and below. But keep in mind that with the VIX, price direction of the market is inverted. Vix goes up whem markets go down. Given that, in terms of market outlook, there may be room for some concern. And that concern is what causes technical analysts to claim “bull markets climb a wall of worry.” We’re not ever in the technician camp, but let’s take a look at what is being implied by the numbers. If the VIX is to behave (exactly) as it has in the average of 208 prior experiences, that index might rise by +4% during the next week. A quick reference back to Figure 1, tells that the behavioral analysis implies that the Index could rise in the foreseeable future (weeks to months) from its present $12.12 to 16.74 or some 38+%. So maybe 1/10th of that +4.62 rise or $0.46 might happen right away. After 7-8 weeks it might be double that, +8%. Are we scared yet? Seems like sort of noise-level variations. Odds of it happening in the past have been little better than a coin-flip, about 5 out of 8. If the VIX went from $12.12 to $13 and its expectations stood still, then the Range Index would be 20-25 with not much change in prospect from where we are now. And maybe 7-8 weeks have passed. For a MM, 7-8 weeks are an eternity. They don’t husband their time, they pimp it. Conclusion No, to make what we know more valuable, we need a much more aggressive and productive strategy than simple asset-class allocation guesses. From what several commenters and some SA contributors have suggested there are effective strategies in place and being acted upon. Discussions to date have been light on the use of the ProShares Short VIX Short-term Futures ETF (NYSEARCA: SVXY ). It has a significant place in this ongoing discussion but has a tale of its own to tell and should be the subject of a separate article, to follow shortly. The enrichment of weekly data availability may make the discussion even more interesting. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.