As Oil Prices Plummet, Investors Flee Natural Resources Funds

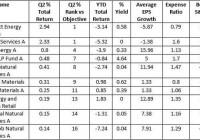

By Patrick Keon Over the past two months, we witnessed a repeat of last summer’s oil price activity. As in 2014, prices of the U.S. and global oil benchmarks (West Texas Intermediate Crude [WTI] and Brent Crude) peaked near the end of June and then headed into decline. Last year, this resulted in seven consecutive months of negative price performance for both WTI and Brent, during which time they lost 54.9% and 57.2%, respectively. As the end of August approaches, the descent for both benchmarks has been more volatile than that in 2014; both WTI and Brent have recently traded at six-year lows, and are down roughly 36% and 30% from their highs at the end of June 2015. This slump in oil prices has impacted the performance and fund flows activity as well as the buy/sell decisions for funds in Lipper’s Global Natural Resources (GNR) Funds and Natural Resources (NR) Funds classifications. Mutual funds in the GNR and NR categories invest primarily in the equity securities of domestic and foreign companies engaged in the exploration, development, production, or distribution of natural resources (including oil, natural gas, and base minerals) and/or alternative energy sources (including solar, wind, hydro, tidal, and geothermal). For the purposes of the current discussion, we look only at those funds that invest the majority of their assets in oil companies; these types of funds account for the lion’s share of the funds in the GNR and NR classifications. Since July 2014, the returns on funds in the GNR and NR categories showed a positive correlation to the movement in oil prices. As illustrated in the table below, the average performance for GNR funds and NR funds followed the direction of WTI and Brent prices during the vast majority of the period. The only times all four groups did not move in the same direction occurred during August 2014 and May 2015. In August 2014, both NR (+3.2%) and GNR (+1.8%) experienced slight bumps when WTI (-0.4%) and Brent (-3.6%) trended downward, while in May 2015, WTI prices appreciated slightly (+1.1%) as the other groups fell off a bit. During the latest slide for WTI and Brent prices (late June through August), funds in the GNR (-24.2%) and NR (-24.5%) categories also experienced a similar sharp downward trend. There was also consistency within the universe: every fund in the two categories suffered at least a double-digit loss during this time frame. Lipper’s data indicates that a positive correlation also existed between the direction of oil prices and fund flows for the GNR and NR categories. During the most recent period in which WTI (-36%) and Brent (-30%) were both down significantly, we saw net outflows from both the fund classifications. GNR funds saw over $480 million leave their coffers, while NR funds had net negative flows of approximately $330 million. Within GNR, three funds were responsible for most of the money leaving the group. Leading the way was the T. Rowe Price New Era Fund No Load (MUTF: PRNEX ) with outflows of over $165 million, followed closely by the Prudential Jennison Natural Resources Fund B (MUTF: PRGNX ) and the Vanguard Energy Fund Inv (MUTF: VGENX ), down $146 million and $126 million, respectively. Within the NR grouping, one fund family accounted for the bulk of the net outflows: Fidelity Management & Research. Fidelity, which has six NR funds, had roughly $240 million leave during this time, with the Fidelity Select Energy Service Portfolio No Load (MUTF: FSESX ) and the Fidelity Select Natural Gas Portfolio No Load (MUTF: FSNGX ) (with net outflows of $71 million and $63 million) taking the two biggest hits. (click to enlarge) When oil prices rose this year (from the late first quarter to the late second quarter), the GNR and NR classifications both responded with overall net inflows. The NR group took in over $840 million, once again paced by the Fidelity family of funds. Fidelity accounted for $340 million in net new money total, with the Fidelity Select Energy Portfolio No Load (MUTF: FSENX ) taking in the largest chunk (+$183 million). Also contributing significantly to NR’s positive showing during this time frame was the Invesco Energy Fund Inv (MUTF: FSTEX ), which registered $118 million of positive net flows. The net flows into GNR (+$423 million) were roughly half of the NR net intake. The largest positive net flows were recorded by VGENX and the RS Global Natural Resources Fund A (MUTF: RSNRX ), at $353 million and $167 million. Of note, going against this trend was PRNEX, which posted net outflows (-$153 million) during the time of oil price appreciation to go along with its $165 million of negative flows during the current oil price decline. Focusing our scope on the changes in holdings in oil company stocks for GNR and NR funds during the current oil price slump, we see the selling was fairly concentrated within NR, but spread out among more stocks within GNR. Within the NR classification, four companies saw their net overall shares reduced by over one million shares, while this number grew to sixteen for the GNR category. The four companies within NR that experienced the most selling were Vantage Drilling (NYSEMKT: VTG ) (-27.6 million shares), BG Group Plc ( OTCQX:BRGXF ) (-3.1 million shares), Halliburton (NYSE: HAL ) (-2.7 million shares), and Weatherford International Plc (NYSE: WFT ) (-2.1 million shares). The number of shares of Vantage Drilling sold represented 8.8% of the company’s shares outstanding (SHOUT). Four funds completely sold out of Vantage, led by FSENX, which closed out an 18.1-million-share position. For the remainder of the group, the shares sold of each accounted for less than 1% of the company’s SHOUT. Weatherford’s activity was the result of four funds liquidating their positions, while BG Group had three funds close out their entire positions. We observe that for the selling within GNR, nine companies went from having a total aggregate position of over one million shares of their stock being held to being completely liquidated. The companies that had the largest positions closed out were Pacific Exploration and Production Corporation ( OTCPK:PEGFF ) (-3.9 million shares) and Brightoil Petroleum Holdings Ltd. ( OTC:BRTPF ) (-2.2 million shares). In each case for these nine stocks, one fund accounted for the entire initial position. The most widely held stocks within NR were essentially static during this period. Schlumberger (NYSE: SLB ) (11 funds) and Baker Hughes (NYSE: BHI ) (10 funds) were the most widely held within NR, and their totals did not change. The GNR classification showed a little more movement in its most widely held stocks. GNR started with five stocks being held by a double-digit number of funds: EOG Resources (NYSE: EOG ) (held by 15 funds), Cabot Oil & Gas (NYSE: COG ) (12 funds), Anadarko Petroleum (NYSE: APC ) (11 funds), Concho Resources (NYSE: CXO ) (11 funds), and Antero Resources (NYSE: AR ) (10 funds). Within this group, EOG Resources was unchanged, while Cabot Oil & Gas, Anadarko Petroleum, and Concho Resources all added one fund each to their totals. Antero Resources had three funds liquidate their positions, to reduce the funds holding Antero to seven. For Antero Resources, the Putnam Global Natural Resources Trust A (MUTF: EBERX ), the AllianzGI Global Natural Resources Fund Inst (MUTF: RGLIX ), and the Putnam Global Energy Fund A (MUTF: PGEAX ) liquidated positions of 4.9 million shares, 550,400 shares, and 353,200 shares, respectively. Oil prices as well as their impact on the performance and fund flows activity of natural resources funds warrant continued observation going forward. The glut in the oil supply does not show signs of abating anytime soon, since the U.S. and OPEC have not indicated any plans to reduce production. If this summer’s downturn in oil prices stretches out as long as last year’s (seven months), we can expect to see additional significant net outflows from funds in Lipper’s natural resources classifications, as well as negative returns for the groups.