Tactical Asset Allocation – My Ideas From 30 Years Of Learning

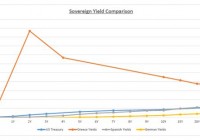

Summary How to create an investment portfolio using Tactical Asset Allocation. Three key measures I use are interest rates, valuation, and growth outlook. When selecting countries or regions, consider demographics, job growth, urbanization, debt levels, geo-political risk and currency effects. Tactical Asset Allocation (TAA) is defined as a dynamic investment strategy that actively adjusts a portfolio’s asset allocation . My goal in this article is to share with you the ideas that I have developed over the past 30 years, and to encourage discussion amongst readers, so as we can all learn from each other’s ideas and experiences. Introduction As a financial adviser, I must first consider a client’s risk profile. Younger clients with less capital invested will typically be prepared to take on more risk, and older clients will usually be comfortable taking on less risk. To keep it simple, I consider the following four asset classes: Cash, Bonds (CDs), Property and Equities. NB: I may also add Infrastructure (when interest rates are low to medium) or other sector funds, on occasion, as a small percentage of the portfolio. In determining my clients’ asset allocation, I consider the following factors: Interest rates Valuation Growth outlook Interest Rates The table below guides me, as does the 10-year Bond rate versus the equities dividend yield. BEST WORST Interest Rates Number 1 Number 2 Number 3 Number 4 Low (0-3%) Property Equities Bonds (CDs) Cash Medium (3-6%) High (6%+) Cash Bonds (CDs) Equities Property NB: The above % interest rates above are based on the reserve bank rate. Typically, the actual lending rates are around 2-3% higher. NB: When interest rates are “Medium” (3-6%), then their effect on the four asset classes is fairly neutral. Interest rates falling is better for bonds (CDs), property and equities. Interest rates rising is better for cash. Valuation My preferred valuation measures for asset allocation are: Price Earnings (P/E) Ratio : I look at a region or country’s P/E, both historical (last year’s earnings) and forward P/E, where available. My rule of thumb is to buy heavily as the P/E heads towards 10 and sell heavily as the P/E heads towards 20. A P/E of 15 is considered neutral. Having said that, I will also factor in interest rates. The Rule of 20 holds that P/E should be 20 minus the current interest rate. E.g., USA’s P/E should currently be 20 – 0.25 = 19.75. This makes allowance for times of extreme interest rates, as does the table below on interest rates. Long-term Charts of a Country’s Equity Index : Here, I simply view a 10- or 20-year chart and see if the index is above or below its trend line. Above being overvalued, below undervalued. Growth Outlook I will assess the following for a region’s or country’s growth outlook; GDP – Current year and forecast for next year. Earnings Per Share (EPS) – Forecast for next year. I will take a look at the following factors: Demographics – Is there a rising middle class, a growing work force or wealth effect? (You can read my article on demographics here , and the one on the rising Asian middle class here .) Job growth (unemployment) – Is the country gaining jobs? Urbanization – Is the country urbanizing? Debt levels – Are household debt levels low? Geopolitical risk and quality of government – Is there low geopolitical risk? Currency valuation – Is the currency undervalued? Trying to factor in all of the above is, of course, no easy task. Nor is it an exact science, but rather, is an art form, in my opinion. Having said that, I will give an example below of how I am currently (as of August 2015) recommending to my Australian clients, based on the above. Moderate-Risk Australian Client – $1m (AUD) Cash – 30% Bonds (Term Deposits, or TDs) – 0% Property – 20% Equities (comprising Asia) – 40% Sector funds – 10% (comprising Global Infrastructure – 5%, Global Resources – 5%) NB: TDs in Australia are the same as CDs in USA. Discussion on the above Tactical Asset Allocation Cash – 30% : Low percentage, as aggressive client and interest rates are very low. The reason to maintain 30% is to have cash available (to protect and invest) in case we see a severe market correction. Cash rates in Australia are still around 2.5% p.a. Bonds – 0% : Zero percentage, as interest rates are falling in Australia. 0% to International bonds, as the rates are already very low in developed markets. Could consider Asian or emerging market bond funds, where the rates are around 5-6% p.a., but there would be currency risk. Property – 10% in Australian-listed property : Low percentage due to earnings growth outlook being weak, with a weak Australian economy and rising unemployment. Low interest rates and fair valuation (P/E 15) suggest some exposure is necessary. Finally, most Australians already have very large $ exposure to an overvalued residential property sector. 10% in Global-listed property : Low interest rates are favourable and valuations fair. Equities – 40% : High percentage due to low interest rates, fair valuations in some regions/countries, strong growth prospects in Asia (demographics mostly good, rising middle class set to triple in size by 2020, according to DBS , with good jobs growth, urbanization, mostly low household and government debt levels, mostly low geo-political risk, and mostly good governments). Global Infrastructure – 5% : Low due to valuations being somewhat elevated. Could go to 10%, based on low global interest rates. Global Resources – 5% : Low, as this sector has been smashed down, and Asian demand for resources will pick up, with 290 million new homes required by 2020 and massive infrastructure projects planned. The valuations may look a bit high, but they are based on very low commodity prices at present. The following P/Es and growth outlook were part of the consideration. Australia: P/E – 15.67, Growth outlook – Poor Asia: P/E – 17.05, Growth outlook – Strong USA: P/E – 19.92, Growth outlook – Average-to-poor Europe: P/E – 19.11, Growth outlook – Average-to-poor Japan: P/E – 16.91, Growth outlook – Average-to-poor The above allocations will certainly lead to many debates, and this is healthy. US investors will naturally have more exposure to their local assets, which will avoid currency risk. They may choose to hold a percentage in US shares, given that the long-term outlook for US companies is strong. I do not disagree with that. My concerns are for non-US investors buying into the US late in the bull run, with a high valuation and a high USD. The main point of this article is to give investors some ideas on how they can go about building their portfolios, with consideration to both risk and return. For me, as discussed, I like to start with interest rates, then consider valuations and growth outlook. I always keep one eye on risk control and the other on optimizing returns, based on the client’s risk tolerance. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Additional disclosure: The information in this article should not be relied upon as personal advice.