Parkit Enterprise Inc.: Pay Discount On Parking Assets, Get Asset Management With Significant Multi-Bagger Potential For Free

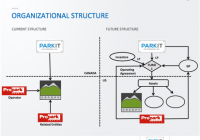

Summary Parkit is a rare opportunity to own a start-up asset manager that is likely to raise significant capital in 2015 to execute on their strategy. Parkit and ProPark combine to create a competitive advantage and have a track record of success which shall help raise capital. Management is extremely bullish and CEO has been buying on the open market extremely consistently at prices higher than today. Shares trade at a significant discount to NAV and investors get the asset management business for free. We see multi bagger potential. (Note: Parkit is also traded on the Canadian TSX Venture Exchange under the ticker PKT.V. Volume on the Canadian exchange is greater than on the OTCQB shares.) We are continuously looking for a business with quality economics run by incentivized managers and where the market is getting the risk/reward ratio very wrong. Strong downside protection is absolutely paramount as the upside will take care of itself with upcoming catalysts. To find such an opportunity in a frothy market such as today one must be willing to search through some obscure places. For 2015, we will be closely following a small parking garage owner based in Canada called Parkit Enterprise Inc. (OTCQX: PKTEF ). The company owns equity in two US off-airport parking garages and has been working on transitioning to becoming a fund manager that aggregates high quality income producing parking assets via a private equity platform. We think the market is serving up a very attractive opportunity as it is extremely rare for the investing public to have the ability to invest in an emerging asset manager. Most often those opportunities are only available to employees or private equity investors. Even rarer is that Parkit already has a track record, has operating assets and is cash flow positive. Currently trading at a discount to NAV on the company’s current owned parking assets, we think the low US$0.40s (mid CAD $0.40s) is a very cheap price to pay for Parkit and does not at all account for the upside potential as a fund manager of quality parking lots. We will be watching Parkit very closely as capital is raised for their first fund over the next few quarters. Management has significantly raised their guidance on funds they will be able to raise and if properly executed, this company is worth many multiples today’s price. History and Fund Manager A Long Time Coming In years past, Parkit was originally called Greenspace and previous management before 2012 did not have a coherent strategy. They helped greenfield the construction of the Canopy parking garage located right outside Denver International airport (completed in 2010), but they ran a bloated cost structure which ultimately almost led to the company going broke even as Canopy performed well. To help transition the company into a leading parking industry company, they brought on Rick Baxter as CEO, some other talented managers and a board of directors with the private equity experience to turn the ship around and execute on an asset manager strategy. Since 2012 when management changes occurred, the company has paid down debt, set the platform for the company’s new fund management strategy and did this while management did not pay themselves for a year and a half. Management decided to take the compensation that accrued to them and roll that over as equity into the company. Unwarranted Recent Price Dive You would expect the market to be reacting positively to Parkit’s turnaround and future prospects, which it did to some degree in April after the announcement of the Expresso acquisition; however, shares have been falling from a high of $0.70 in both the Canadian and US listed shares since October. We think that the market is overreacting to the combination of the oil sell off and the recent resignation of John LaGourgue, VP of Corporate Communications, who was extremely bullish on the company’s long-term prospects. We think that the oil price drop does not change the investment thesis and actually could increase drivers’ interest to travel and park in parking lots. Also, LaGourgue left for personal reasons and as a sign of interest in the company’s long-term prospects he continues to keep 85-90% of the shares and options in Parkit. Keep in mind, many of his shares were purchased on the open market and that he likely sold some shares to diversify his investments. Business Current And Going Forward (click to enlarge) (Source: Parkit Presentation) Parkit has been operating in the past and currently under the model to the left. Parkit owns an equity stake in the Canopy and Expresso garages alongside ProPark America and a few other outside investors. Parkit does not operate these assets, ProPark America provides those services as that is within their circle of competence. Previously Parkit did not bring too much to the relationship other than the capital to invest into Canopy, but that is changing drastically as the new strategy emerges. Parkit’s new strategy is to, to put it simply, set up and run a parking garage private equity fund not too different from an asset manager in structure. As seen in the chart above and to the right, Parkit has already set up a fund with ProPark to act as a platform to raise institutional money to then be used to aggregate parking assets that both Parkit and ProPark manage. Parkit and ProPark both are General Partners (50:50 split) and will receive hedge fund like management fees (0.5-1% of AUM), acquisition fees ( Additional disclosure: This article is meant for instructional purposes and not meant as a recommendation to buy or sell. We are human and can be wrong, especially with our forecasts, so it is extremely important to do your own homework. The only kind of intelligent investing is through your own due diligence. We own both PKTEF and PKT.V.