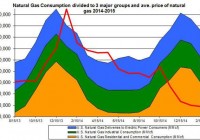

The young UNG bull continues to look like a longer-term rager. The longer-term UNG bull thesis remains intact and has seen some nice upside surprises as of late. Continue to buy UNG as the trend greatly favors bulls. Consensus is way against me on this one guys, way against me. Yes, still. Yes, even after we called the bottom for natural gas pricing two weeks ago when we said “The Turn ” had happened (as we said would happen on the ” Bloodbath “) for The United States Natural Gas ETF, LP (NYSEARCA: UNG ). Yes, even after we doubled down with UNG on the “Bloodbath” lows and watched it rip higher from there in the following 5 trading days. UNG has since held its gains and is sitting pretty on significantly colder weather than consensus was expecting. The market is still betting against us Seeking Alpha UNG trend buyers. (click to enlarge) Still, despite not being consensus our long-term bullish trend remains intact based on our original thesis points of: Falling rig counts hurt overall production – that’s good for the supply side of the equation as production is slowed overall. (Stated originally FEB 3, 2015) This one is pretty cut and dry and should continue to be in our favor for at least the medium duration, regardless of natural gas pricing, as long as oil pricing remains below breakeven levels for respective plays domestically. First, a look at falling rig count overall – take a look at this incredible drop-off in: 1) total rig count, 2) primarily natural gas rigs, and 3) horizontal rigs. (click to enlarge) Those horizontal rigs are more efficient, so seeing those drop hurts even worse than the number implies. Again, this isn’t going to change the trend until oil gets above estimated break-even levels for respective plays. What are those? This is a graphic that was provided to me by John Seitz, the former CEO of Anadarko (NYSE: APC ), in a slide deck presentation for another company that I’m invested in. It’s pretty busy, but you can still take away the major play break-evens that we need: (click to enlarge) Yeah, I don’t want to say we’re a great distance away from some of the break-even levels on the bottom end of this, but we sure as heck aren’t deep into the money on them. This part of the thesis remains well intact and safe on at least the medium duration. Less oil E&P to come on lower CAPEX across the board for oil and natural gas E&Ps – that’s also good for the supply side of the equation. (Source: Bloomberg.com) (Stated originally FEB 3, 2015.) Clearly, looking at the Baker Hughes rig count above I think we can see that this is intact longer term. Again, the only difference here from long-term thesis bullet point one is that, this is more pointed to overall rig count rather than strictly the gas rig count (if they can even be separated anymore). Also, this bullet point has to do with CAPEX cuts which we’ve seen in size starting with announcements as early as mid-December 2014: This graphic is in no way inclusive of all the cuts announced and in effect currently, but I wanted to keep the article at less than 100 pages long, so, I’ll call it day right there. Just know that you can add Chesapeake Energy Corporation (NYSE: CHK ), SandRidge Energy, Inc. (NYSE: SD ), Magnum Hunter Resources Corporation (NYSE: MHR ), etc., to that list as well. We’re talking these cuts are taking place or have taken place across the board and have created a mid/longer term bottle neck for supply. I’m betting on the fact that spring will start early and summer will be, well, it’ll be hot – that’s good for the demand side of the equation – for clarity these projections are based on longer-term weather models from Weather.com which may be unreliable. (Stated originally FEB 3, 2015.) This is the most subjective portion of the thesis, but I’m still betting it remains intact. It’s a large part of the overall longer-term picture here, so I need this to be right but with weather we’re always hoping for the best. What I know is that right now the back-end of this winter is playing out beautifully and at times in the last few weeks in the South Central parts of the U.S., we’ve seen cooling demand during the day and heating demand at night. Southern folks like their temps to stay right in the middle of comfortable, at least this Southern Gentleman does. Give me some wiggle room on this one, but I’ll keep SA readers updated on any material changes. Still, just know the general market is betting heavily that I’m wrong: I believe at poor hedging or at lower than ideal aggregate hedging that natural gas E&P names won’t “pump baby pump” as hard into what has been excellent hedging in size the last few years – that’s also good for the supply side. Examples of companies I’ve reviewed that have 1) less than ideal pricing hedging or 2) less than ideal aggregate hedging coverage are Chesapeake Energy Corporation, Antero Resources Corporation (NYSE: AR ), Ultra Petroleum Corp. (NYSE: UPL ), Halcon Resources Corporation (NYSE: HK ), SandRidge Energy, Inc., Quicksilver Resources Inc. (NYSE: KWK ), etc. This list could have been 50 names deep. (Stated originally FEB 3, 2015.) Again this is a partially subjective, company by company exercise but from my research on Antero Resources Corporation, Ultra Petroleum Corp., SD, CHK, AR, MHR, etc., I’ve found that these E&P’s are significantly less hedged Y/Y and have very little of total 2015 production hedged at all. This has contributed to the first few bullets of the thesis in why the E&P’s have had to cut back on production. It’s all just one big cycle feeding each other and further helping create the supply bottleneck. The good news is, none of these thesis points are short-term and that’s why we UNG longs get to own the trend until further notice. Yes, there’s going to be some lulls in the trend as UNG doesn’t move in straight lines, but the longer-term trend is going to remain higher until some of those bullet points can be invalidated. Right now, the supply bottle neck thesis is irrefutable. Now, how about demand. The following is an excerpt taken from my INSTABLOG page that was written the day of inventory after an ill-advised attempt at selling UNG off: So, again I come into this fresh week bullish on all durations but MUCH more bullish on the shorter-term durations than I was one week ago. One week ago, I was more bullish short-term technicals than I was fundamentals. Today, that’s the opposite. Immediate Term (next 7 days): bullish, STRONG BUY. With UNG tanking intra-day you go ahead and you add some shares here for the next 7 days as this should be about the lows. Weather in Austin gets frigid with worse with slow progression heading into next Tuesday when LOD’s (low of days) hit 27 degrees. In between there LOD’s hover in the low-50’s and you know how our bull thesis loves that mark. Looking a bit further out into Wednesday and Thursday HOD’s (high of days) and LOD’S are as follows: 48/28, 56/38. This is after three straight weeks of essentially mid-70 HOD’s and low-60 LOD’s. Folks in the South will be cold and they’ll be using heat. Nationally, the weather picture has been much cooler the last few weeks and it looks like no help is on the way. A BIGTIME bull run should be ahead for UNG the next 7 days. Mid Term (next 30 days): Mixed to BULLISH as of right now, BUY in the immediate term and wait on further buys. I’m going to holdover last week’s mid-term reco as the story hasn’t really changed on the 30 day. While the shorter term forecasts definitely bulled-up with colder than expected weather being forecasted the forward looking 30 days remains a bit mixed. Let’s wait to get too bullish here. Long Term (longer than 30 days): bullish, BUY on dips. As long as our long-term bull thesis remains intact I don’t see any reason to sell UNG at any time at a loss. What I mean by that is that if you buy today and let’s say I’m wrong for the next month – inclusive of fees just hold the position because we know the longer term bull thesis is intact (assuming it is). Knowing that provides comfort if/when down on a position because of the speed that UNG can move to the upside. As long as we have the trend, and we certainly have the trend, we have safety. Finally, one quick note that could develop into another long-term thesis bullet point is that, powerburn could increase as the estimated monthly average price for electricity generation between CAPP coal and natural gas pricing has converged greatly. This is definitely something that would need several variables to come into play to remain a longer-term bullet point if it indeed does become one (that’s why it wasn’t listed originally), but this could further increase demand in the near-term: To wrap this week’s update up, I’m bullish trade and trend and I continue to reiterate the long-term thesis being in-play. Continue to follow the weekly updates here on inventory day and make sure to subscribe to the UNG ticker for PUSH-email alerts from other authors. Have a good inventory day guys. Disclosure: The author is long UGAZ. (More…) The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it (other than from Seeking Alpha). The author has no business relationship with any company whose stock is mentioned in this article. Additional disclosure: The author has a UGAZ cost basis of $2.69