SPDR S&P 500 ETF (SPY) Analysis: Using CapFlow And FROIC

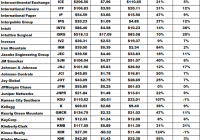

Summary Analysis of the components of the SPDR S&P 500 ETF (SPY) using my CapFlow and FROIC ratios. Specifically written to assist those Seeking Alpha readers who are using my free cash flow system. Part II will concentrate on “Main Street” while Part I in the series concentrated on “Wall Street”. Back in late December I introduced my free cash flow system here on Seeking Alpha, through a series of articles that you can view by going to my SA profile . My purpose in doing so was to try and teach as many investors as I could on how to do this simple analysis on their own as I believe in the following: “Give a person a fish and you feed them for a day, Teach a person to fish and you feed them for life” I have been very pleased with the positive feedback that I have received so far, but included in that feedback were many requests by those using my system, to see if they did their analysis correctly or not. Since the rate of these requests have been increasing with every new article I write, I have decided to start a new series of articles here on Seeking Alpha analyzing the SPDR S&P 500 ETF (NYSEARCA: SPY ), where I will analyze each of its components individually. That way those of you using my system will have something like a “teacher’s edition” that will give you all the correct calculations for each component. Obviously I can’t include the results for all my ratios in one article, so I will thus be doing a series of articles, where each ratio’s results for the SPDR S&P 500 ETF will have its own article devoted to it. Hopefully these articles can be used as reference guides that everyone can use over and over again, whenever the need arises. Having said that, I would suggest that everyone first read Part I by going HERE . There you will find the data on my “Free Cash Flow Yield” ratio which is one of three parts that I use it tabulating my final “Scorecard”. While free cash flow yield is a Wall Street ratio (Valuation Ratio), this article with concentrate on my “CapFlow” and “FROIC” Ratios, which are Main Street ratios. The final Scorecard results will be available in Part III of this series and basically combines all three ratio results to generate one final result. Once completed, my scorecard should give everyone a clearer understanding on how accurate the valuation is that Wall Street has assigned each company relative to its actual Main Street performance. Before we show you the final results of our two Main Street ratios, here is brief introduction to what each of the two ratios, which make up my system as well as what the final “Scorecard” score mean. CapFlow CapFlow is the name I have given to the ratio (Capital Expenditures/Cash Flow). CapFlow allows us to see how much capital spending (or capital expenditures, CAPEX) a company must employ in relation to its cash flow to maintain itself and more importantly grow the company. This ratio is extremely useful as it is both a qualitative and quantitative ratio in that it acts as a laser beam into the inner workings of a company. Quite simply if a company is increasing its profits and doing so by spending less money relative to its growth in cash flow, it should, in theory, outperform on Main Street. When you can have such an occurrence for more than a few years in a row, it clearly shows you have wonderful management in place that knows what it is doing. The ideal again is to consistently have a CapFlow of less than 33% and avoid any company, like the plague, that has a CapFlow of over 100%, as in such a case management is spending more in capital expenditures than it is bringing in from cash flow from operations. That is a recipe for disaster in my opinion. Just using this ratio alone will narrow your list of potential candidates for investment substantially and will give you an easy-to-use tool for judging management effectiveness. FROIC FROIC = Free Cash Flow Return on Invested Capital FROIC= Free cash flow/ (long-term debt + shareholders equity) FROIC basically tells us how much return in free cash flow a company generates for every one dollar of “Total Capital” it employs. I consider FROIC the primary determining factor in identifying growth companies as one can compare every company on an equal basis using this ratio. The question I ask every company I analyze is: “How much return (in percent) in free cash flow are you going to give us for every dollar of total capital you invest?” A FROIC of 20% or more is considered excellent and the higher the result the better. Since long-term debt is included in the invested capital part of the equation, one can see quite clearly by using this ratio, on just how well or how poorly management is managing its debt. So without further ado here are my results for the CapFlow and FROIC ratios for the components that make up the SPDR S&P 500 ETF : Always remember that the results shown above are just for two ratios and that this is not investment advice, but just the results of the ratios. The system outlined in this article and all that will follow, as part of this series, are just meant to be used as reference material to be included as just “one” part of everyone’s own due diligence. So in other words, don’t make investment decisions based on just these two results, but incorporate them as part of your own due diligence.