Global Macro: The Role Of A ‘Go Anywhere’ Strategy

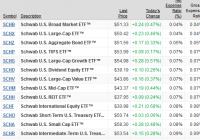

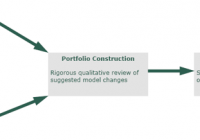

By Andy Hyer Global macro is among the least restricted of all the major investment styles and is often referred to as a ‘go anywhere’ strategy which can potentially create positive investment returns in a wide range of economic environments. As shown in the diagram below, there is a rules-based process that we follow to manage our Global Macro portfolio (available on the Masters and DMA platforms at Wells Fargo Advisors and other SMA platforms , as a mutual fund – Arrow DWA Tactical Fund A (MUTF: DWTFX ) – and as an ETF – Arrow DWA Tactical ETF (NASDAQ: DWAT ). Investment Process We start with a broad investment universe of ETFs from the following asset classes: U.S. Equities, International Equities, Inverse Equities, Currencies, Commodities, Real Estate, and Fixed Income. That broad universe of ETFs is categorized into ETF Baskets, allowing us to rank the baskets by their relative strength. That top-down Basket Ranking part of the model seeks to guide the model to the strongest asset classes and to avoid the weakest asset classes. There is no forecasting in any part of this model-it is purely a trend-following strategy. There is also a bottom-up ranking of all of the ETFs in the investment universe. That ranking allows us to score each ETF to determine exactly what we buy and when a position is sold. 10 ETF are held in the Global Macro portfolio and the positions will stay in the portfolio as long as they retain strong relative strength. We’ve had some positions stay in the portfolio for years at a time and other positions that have been quickly removed. Any position stays in the portfolio only as long as it retains is favorable relative strength. (click to enlarge) Why Global Macro? Asset classes go through bull and bear markets. That goes for all asset classes. It is easy for someone to look at any 30 year period of time in history and use that period to suggest that all that is needed for any investor is a buy and hold approach to asset allocation using a narrow universe of asset classes. In one 30-year period, a 70% allocation to U.S. equities and a 30% allocation to U.S. fixed income would do the trick. However, take a different 30 year stretch and it may make more sense to include a healthy allocation to Real Estate or International Equities or Commodities. The ideal or optimal passive allocation for any 30 year stretch is only evident with the benefit of hindsight. Real investors have no idea what the future will hold. Rather than guess what asset mix might work best as they manage their retirement nest egg, a relative strength-driven Global Macro strategy relies on a strict trend-following approach to adapt to current markets. Investors may like to think that if they guess right and select the right passive asset allocation then their investment experience will be similar to the guy on the bike below (top of the image)…smoothly accumulating and compounding their retirement nest egg as they glide towards their retirement years. However, reality in the financial markets is anything but a smooth ride. Without an adaptive investment strategy as part of their asset allocation many investors will guess wrong and pick the wrong passive asset allocation. Furthermore, investor behavior being what it is, many investors will panic at the wrong times (and unwisely tinker with their asset allocations). Global Macro has the potential to play a soothing role for an investor and has the potential to help investors stay the course with their overall asset allocation. (click to enlarge) Source: @ThinkingIP Current Holdings As of 6/30/15, current holdings in our Global Macro portfolio were as follows: (click to enlarge) Performance We are very proud of the fact that Global Macro has performed well compared to its peer group over time. As shown below, The Arrow DWA Tactical Mutual Fund has outperformed 95% of its peers in the Morningstar Tactical Allocation category over the past 3 and 5 years; outperformed 92% over the past year, and has outperformed 68% of its peers YTD. Fact Sheet Click here for a fact sheet on our Global Macro portfolio. Nothing contained herein should be construed as an offer to sell or the solicitation of an offer to buy any security. This report does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this document. It is for the general information of clients of Dorsey, Wright & Associates, LLC (“Dorsey, Wright & Associates”). This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation in this document, clients should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice. The relative strength strategy is NOT a guarantee. There may be times where all investments and strategies are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon. Each investor should carefully consider the investment objectives, risks and expenses of any Exchange-Traded Fund (“ETF”) prior to investing. Before investing in an ETF investors should obtain and carefully read the relevant prospectus and documents the issuer has filed with the SEC. To obtain more complete information about the product the documents are publicly available for free via EDGAR on the SEC website ( http://www.sec.gov ).