Cost-Efficient Exposure To Momentum

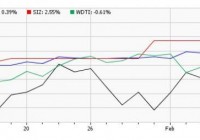

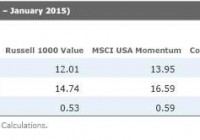

By Alex Bryan In many cases, extrapolating past performance into the future is a bad idea. In fact, securities that have outperformed for several years tend to become more expensive and priced to offer lower returns going forward. But in the short run, recent performance trends tend to persist. Winners over the past six to 12 months tend to continue to outperform for the next several months, while those that have underperformed often continue to lag. This phenomenon is known as momentum. It has been observed in nearly every market studied and across different asset classes over long periods. Investors can get efficient exposure to stocks with positive momentum through iShares MSCI USA Momentum Factor (NYSEARCA: MTUM ) for a low 0.15% expense ratio. This fund tracks an MSCI index that targets large- and mid-cap stocks with strong risk-adjusted price momentum, which differentiates it from traditional momentum strategies studied in the academic literature. This focus on risk-adjusted performance may help moderate the fund’s risk profile and reduce turnover. Volatility in a stock influences price movements, but this component of returns may not last. Risk-adjusted momentum gives a better signal of directional price movements, which may be more likely to persist. MSCI built the fund’s index with capacity in mind, at the expense of style purity. It usually only reconstitutes twice a year and applies a wide buffer to reduce turnover. On paper, momentum strategies appear to work better with reconstitution every month, as momentum is strongest over shorter windows. But in practice, monthly reconstitution can create high turnover and transaction costs. The index’s more tempered approach may improve its cost-efficiency, though it can still experience high turnover. In fiscal 2014, its turnover was as high as 123%. However, it has not yet distributed a capital gain, thanks to the exchange-traded fund structure, which allows managers to transfer holdings out of the portfolio through a nontaxable in-kind transaction with its authorized participants. Momentum is less likely to persist when volatility spikes. In order to address this potential problem, the fund’s benchmark applies conditional rebalancing in between the schedule reconstitution dates when market volatility significantly increases. When this rebalancing is triggered, the index focuses on more recent momentum to construct the portfolio. Investment Thesis In theory, investors should arbitrage any predictable price pattern away. Yet simple momentum strategies have historically worked (on paper) in nearly every market studied. Behavioral finance offers the best explanation for the momentum effect. Those in this camp assert that investors tend to anchor their beliefs and are slow to update their views in response to new information. For instance, event studies have demonstrated that stocks that beat earnings expectations have historically tended to offer excess returns for many weeks after the announcement. Similarly, stocks that miss expectations have tended to continue to underperform. Investors may also be reluctant to sell losers in the hope of breaking even and quick to sell winners in order to lock in gains. This irrational behavior may prevent stocks from quickly adjusting to new information. Once a trend is established, investors may pile on a trade or over-extrapolate recent results, pushing prices away from their fair values, which may contribute to the long-term reversals underlying the value effect (the tendency for stocks trading at low valuations to outperform). While momentum strategies have a good long-term record, they may struggle during periods of high volatility or market reversals. As a result, the fund can underperform when it is most painful. For instance, its benchmark lagged the MSCI USA Index by 3.8% during 2008. Heading into a bear market, momentum strategies tend to overweight riskier stocks, which may underperform during a correction. After a market downturn they tend to load up on defensive stocks, and they may miss out on some of the upside during a sharp recovery. There is also a risk that momentum may become less profitable as more investors attempt to take advantage of it. That said, the momentum effect hasn’t gone away even though it was first published in academic literature in 1993. Like any strategy, momentum can underperform for years. This risk may limit arbitrage and allow momentum to persist. MTUM’s moderate style tilt takes some juice out of the strategy. However, it still captures the essence of the style and at a lower cost than if it pursued a more aggressive rebalancing approach. It has a good chance of beating the market if momentum continues to pay off. But even if momentum doesn’t pan out, the fund’s low expense ratio doesn’t hurt performance much. This is a compelling holding on its own, but it can also offer good diversification benefits to value-oriented investors. That’s because momentum tends to work well when value doesn’t, and vice versa. Therefore, putting them together may reduce the risk of significantly underperforming, as the chart below illustrates. It shows the aggregate wealth accumulated in the MSCI USA Momentum Index, the Russell 1000 Value Index, and a portfolio split evenly between the two, divided by the wealth accumulated in the broad MSCI USA Index. When the line is sloping up, the strategy is beating the market, when it is sloping down, the strategy it is underperforming. Keep in mind that the MSCI USA Momentum Index’s live performance record only started in 2013. Sources: Morningstar Direct, Analyst Calculations. Portfolio Construction MTUM tracks the MSCI USA Momentum Index, which draws stocks from the market-cap-weighted MSCI USA Index, which includes large- and mid-cap stocks. In May and November, MSCI calculates the ratio of each stock’s price returns of the past 13 and seven months (excluding the most recent month to take into account the tendency for performance to reverse during that horizon) to its volatility during the past three years. There isn’t a great theoretical reason to use price returns rather than total returns, but it shouldn’t make a big difference. The index averages these two scores and selects the highest-scoring stocks until it reaches a fixed target number of stocks (currently 122). In order to reduce turnover, new constituents must rank in the top half of the index’s target number of securities to get priority over stocks that were previously in the index. Stocks already in the index only have to rank within 1.5 times the target number of securities to remain in the index. Holdings are weighted according to both the strength of their risk-adjusted momentum and their market capitalization, subject to a 5% cap. In addition to the scheduled semiannual reconstitution, MSCI may rebalance the index when the month-over-month change in the trailing three-month volatility of the market is larger than the 95th percentile of such monthly changes historically. When this occurs, the index only uses each stock’s seven-month risk-adjusted momentum score. Alternatives AQR offers some of the purest momentum funds on the market. However, these funds are only available in a mutual fund format, which can make them less tax-efficient. AQR Large Cap Momentum (MUTF: AMOMX ) (0.49%) ranks the largest 1,000 U.S. stocks by total return over the prior 12 months, excluding the most recent month, and targets the third with the strongest momentum. It weights its holdings according to both the strength of their momentum and market capitalization and rebalances monthly with an adjustment to reduce turnover. While AQR Large Cap Momentum’s $5 million minimum investment may seem a little steep, there is no minimum investment for investors who gain access to the fund through a financial advisor. AQR International Momentum (MUTF: AIMOX ) (0.65% expense ratio) and AQR Small Cap Momentum (MUTF: ASMOX ) (0.65% expense ratio) might also be worth considering. PowerShares DWA Momentum ETF (NYSEARCA: PDP ) is another option, but it is difficult to justify its 0.65% expense ratio. It targets stocks with the best relative strength and rebalances its portfolio quarterly. Historically, PDP has been less sensitive to the standard momentum factor documented in the academic literature than MTUM. Disclosure: Morningstar, Inc. licenses its indexes to institutions for a variety of reasons, including the creation of investment products and the benchmarking of existing products. When licensing indexes for the creation or benchmarking of investment products, Morningstar receives fees that are mainly based on fund assets under management. As of Sept. 30, 2012, AlphaPro Management, BlackRock Asset Management, First Asset, First Trust, Invesco, Merrill Lynch, Northern Trust, Nuveen, and Van Eck license one or more Morningstar indexes for this purpose. These investment products are not sponsored, issued, marketed, or sold by Morningstar. Morningstar does not make any representation regarding the advisability of investing in any investment product based on or benchmarked against a Morningstar index.