‘Betterer’ Investing For A Tired Bull Market

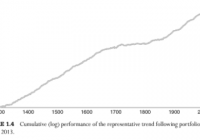

Robo-advisors may not be a “betterer” idea than traditional advisors if all you get is a diversified buy-and-hold approach. If you are a long-term buy-and-hold investor, you should be prepared to weather an occasional four- to seven-year period of diminished portfolio value. If that troubles you, perhaps you should rethink your strategy. At age 33, tennis great Roger Federer trains hard to get “betterer” to keep up with the challenges of staying at the top of the ATP World Tour. While watching a match I saw an ad for robo-advisor Betterment, which suggested that their method of diversified, passive investing is better than more costly traditional advisor services. That got me thinking about what is truly better. Mutual funds were created as a better way to invest in a diversified portfolio of assets aimed at a selected market or market segment. ETFs were created as a lower cost way to do what mutual funds do. Robo-advisors were created as a lower cost way to do what human advisors do, largely with mutual funds and ETFs. All of this has been done to drive the cost out of a “buy and hold” diversified investing approach promulgated by Modern Portfolio Theory (MPT). If a relatively higher-priced wealth advisor implementing MPT on your behalf is like smoking an excellent Cuban cigar, then using a robo-advisor is like smoking a generic cigarette. It’s cheaper, but smoking is still bad for you. I’m not going to go into the cascading unrealistic characterizations, false assumptions and inappropriately applied elegant math that underlies MPT. Nor am I going to explain why it has been so feverishly adopted by the financial products and services industry. There is plenty of that around to read, and you can decide for yourself if the king has no clothes. In the end, you should decide if your investing priority is to beat the market (relative performance) or to make steady positive gains (absolute return). It seems to me that most wealth is created by savings and/or by well-timed concentrated investment positions. Every wealthy person I know got that way either because they inherited wealth, or they spent less than they made (saved), or they had a concentrated investment in a corporation where they worked or in their own business. As Warren Buffett once said, ” Diversification is protection against ignorance. It makes little sense for those who know what they are doing.” While there are likely many exceptions to this generalization, there are some important factors working against wealth creation via long term holding of diversified financial assets? They include: The timing of contributions to investment portfolios; Unforeseen periodic major market corrections that put investment portfolios underwater (or in “drawdown”): Repeated reactions to market advances and declines, wherein many investors enter selected markets only after they have risen and exit only after they gave fallen; and The precept of MPT that the trends of market pricing cannot be known, and are therefore not addressed. The inability of most individual investors and their advisors to protect against market downside variation (drawdown) is obfuscated with the marketing of long-term average market return statistics and assertions about the risk-reduction value of diversification. The market cycles and the investor behavior they illicit contribute heavily to low average investor returns . US equities have risen each year since 2009. Since 1871 US equities have never risen for seven consecutive years. Are you betting that 2015 will break the record? Even though there are secular bull and bear markets that can last 20-30 years, there are dramatic cyclical market downturns that occur about twice a decade which can have severe negative impacts on one’s cumulative investment return. It took 30 months for the S&P 500 to fall 49% between March 2000 and October 2002, and about seven years to recover (total return). It took 17 months for the S&P 500 to fall 57% in the 2007-2008 financial crisis and 5.4 years to recover (total return). More significantly, this last recovery has been fueled by central banks flooding markets with liquidity and forcing money out of savings and into risk assets to find a return. How long could your exposure to equities be in drawdown after the next crisis, if “the Fed” (that’s Federal Reserve, not Roger Federer) is not there to bail you out? So, if you are wealthy and trying to protect what you have, or if you are trying to build wealth over time, you should be wary of applying the generic diversified long-only MPT approach, no matter if you are implementing it with a big bank wealth advisor or with a robo-advisor. How much of a drawdown are you comfortable with? How long do you have before you may have to use some of those invested funds? Liquidation of investments in drawdown is permanent wealth impairment. Absolute return may be a better investment goal for many, especially today. Unfortunately, it is not available from an online robo-advisor for 20 basis points a year. The skills and proprietary analysis required for well-timed concentrated investment positions usually comes with higher fees. If it can help you to consolidate the gains you have made since 2009, maybe it is worth a higher fee. After all, it’s not only what you make, but what you keep that matters. And if your forward investment time horizon is likely to include another major market correction, you will keep more (after paying higher fees) by side-stepping most of the drawdown (assuming the advisor times the market well). By putting your faith in a selected absolute return strategy, you may protect yourself against natural inclinations for unprofitable reactions to changing market trends. It is said that markets climb up the stairs, but come down the elevator. Absorbing the full impact of the next major market correction will be a lot more painful than paying a higher advisory fee. Just as the great Federer has to train hard and switch to a new racquet to stay near the top, maybe your forward results will be “betterer” with an absolute return investment approach in this tired bull market. (click to enlarge) Absolute Return, a publication of Hedge Fund Intelligence, maintains a database of equal weighted hedge fund performance separated into 16 strategies. The Composite Index is an equally weighted index which represents the median performance of all funds in the Absolute Return Database. Returns are net of fees. Trendhaven makes no claims regarding the accuracy of the data reported by hedge funds or compiled and reported by Absolute Return or Hedge Fund Intelligence. Additional disclosure: The author is an investment advisor representative applying an absolute return strategy in separately managed accounts.