Frontier Markets Index Issues: How Flawed Index Construction Is Distorting Perceptions Of The Asset Class

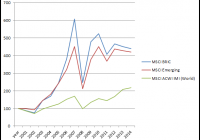

Summary A common complaint heard from Frontier Markets investment managers is the poor quality of the major indices that are designed to track Frontier Markets equities. The primary underlying cause of the problem has been, and continues to be, the use of market capitalization as the construction weighting methodology. This can contribute to lopsided geographic and sector weightings, which distort the risk and return characteristics of the equity market segment being considered. This article explores the nuances and flaws of two of the most prominent Frontier Markets indices, the MSCI Frontier Markets Index and the S&P Frontier Broad Market Index. It details the uneven geographic and sector concentrations found in these indices, root causes of these imbalances, as well as the implications such index construction has on return and risk. Frontier Markets Index Issues (click to enlarge) How Flawed Index Construction is Distorting Perceptions of the Asset Class Sean Wilson, CFA Brent Clayton, CFA Ha Ta A common complaint heard from Frontier Markets investment managers is the poor quality of the major indices that are designed to track Frontier Markets equities. Poor index construction is not a new issue for the global investment community. The primary underlying cause of the problem has been, and continues to be, the use of market capitalization as the construction weighting methodology (some indices use free-float adjusted market capitalization weighting methodologies, which suffer from the same issues). This can contribute to lopsided geographic and sector weightings, which distort the risk and return characteristics of the equity market segment being considered. Frontier Market indices suffer from additional weaknesses due to varying degrees of capital market development in constituent countries, which can magnify the distortions caused by market capitalization-based weighting methodologies. As Frontier Markets indices are used to formulate asset allocators’ return and risk expectations for the asset class and as benchmarks to measure and evaluate Frontier Markets investment managers, it is important that the nuances and flaws of these indices are identified and understood. D é j à Vu All Over Again … Over the past century, indices have risen in importance from rough barometers of equity market performance to structural components of passive investment strategies with allocations worth hundreds of billions of dollars. However, some of the most prominent indices have been distorted by the common practice of employing market capitalization to determine the weight of their respective constituents. With this approach, the larger a company’s market capitalization, the larger its weighting in the index will be. This approach is particularly sensitive to distortions from market bubbles because it exaggerates the weightings of those areas in the index which have been inflated. One of the most extreme examples of this occurred in the late 1980s and early 1990s in the MSCI EAFE Index, then the most popular benchmark for international equities. Japan grew from approximately 10% of the index in 1970 to over 60% of the index by the late 1980s. Investors in the US market saw a similar phenomenon appear in the S&P 500 when the technology sector grew six-fold to over a 30% weighting during the tech bubble at the turn of the century. Both events created indices that were less diversified and more precarious with concentrations in areas of the market that were most overvalued. Investment managers benchmarked to these indices faced a binary decision with respect to their weighting in these extreme concentrations, putting commonsense portfolio diversification at odds with the business risk of deviating substantially from the primary measuring stick of their performance. An investment manager’s singular call on Japan or the technology sector often, for better or worse, became the primary determinant of fund performance. With the retreat of the Japanese stock market and the bursting of the technology bubble, the distortions dissipated, but the underlying methodology issues remained. Today, Frontier Markets indices suffer from a lack of diversification with historically high concentrations in a few countries and an abnormally large weighting in the financials sector. This can be seen in the following charts of the historical concentrations of the two most prominent Frontier Markets indices, the MSCI Frontier Markets Index (“MSCI FM Index”) and the S&P Frontier Broad Market Index (“S&P Frontier BMI”): Chart 1: (click to enlarge) Source: MSCI Barra, S&P Dow Jones Indices On August 31st, 2008, the eve of the collapse of Lehman Brothers and the ensuing Global Financial Crisis, the MSCI FM Index and the S&P Frontier BMI held a whopping 65% and 58%, respectively, in the financials sector. Likewise, two countries, Kuwait and the United Arab Emirates, together accounted for 51% and 53% of the MSCI FM Index and the S&P Frontier BMI, respectively. One single country, Kuwait, with a population and land mass that are approximately one third and three fifths that of Belgium respectively, accounted for 35% of the MSCI FM Index and 39% of the S&P Frontier BMI. These concentrations are slightly less disproportional today, but there remains a roughly 50% concentration in the financials sector in both indices and 38% and 32% weightings in the top two countries of each, respectively. As discussed further below, the ramifications of such uneven weightings are significant. The root causes of such lopsided concentrations are twofold. First, a market capitalization-based weighting methodology makes these indices susceptible to market bubbles, which reward stocks and markets that go up with greater and greater index weights. Second, differences in development stages among countries can skew index sector weightings. Financial institutions are generally first to list on nascent stock exchanges. Banks are the foundation of any economy and are relatively more established than other industries in Frontier economies. They have business models that rely on shareholder funding due to international regulatory requirements, so it is not surprising that Frontier Markets indices have an overly large weighting to the financials sector. In addition, more developed Frontier Markets with large index weightings such as Kuwait that are held back from being upgraded to “Emerging Markets” status for technical reasons (foreign ownership restrictions, liquidity and size requirements) can skew overall index exposures due to the idiosyncratic nature of their underlying stock markets (e.g. a disproportionately large publicly-listed banking industry, a lack of energy and materials sector listings due to state ownership, a small consumer sector due to a smaller population). These two issues together serve to magnify the distortions in sector and country weightings. Implications for Return Expectations in Frontier Markets Analyzing historical returns of indices is a logical starting point for investors wishing to understand an asset class. Typically, historical returns are used as guideposts for setting investor expectations about potential future returns. With Frontier Markets, however, the lopsided concentrations in certain countries and the financials sector have dominated the historical performance of these indices and continue to mask the true underlying diversity of opportunities available in the over 50 countries with liquid Frontier Markets stocks. An argument sometimes voiced against allocating to Frontier Markets is the lower relative performance of Frontier Markets compared to traditional Emerging Markets following the Global Financial Crisis. Looking at the MSCI indices in Chart 2, while Emerging Markets appear to have quickly snapped back, Frontier Markets appear to have languished for several years and only recently have begun to experience a modest recovery. As of May 31st, 2015, the MSCI FM Index was still more than 18% below its August 31st, 2008 pre-Lehman value while the MSCI Emerging Markets Index was up 23%. Chart 2: (click to enlarge) Source: Bloomberg Looking at the three largest country weightings in the MSCI FM Index on August 31st, 2008 (collectively representing 66% of the index), however, reveals how greatly these index concentrations can influence index performance. Chart 3: (click to enlarge) Source: Bloomberg The MSCI Kuwait Index (Kuwait was 35% of the MSCI FM Index in August 2008) has, in fact, languished since the Global Financial Crisis. Plagued by low growth, high valuations, regional instability with the Arab Spring, and political gridlock domestically, Kuwait has not been a hallmark of the investment case for Frontier Markets in recent years. It remains 45% below its pre-crisis value. The United Arab Emirates market (16% of the index in August 2008) also languished for several years. However, the economy and market began a recovery in 2012, which shot the MSCI UAE Index up 276% from the end of 2011 to the country’s exit from the MSCI FM Index at the end of May 2014. Viewing the broader index’s performance from this perspective suggests that the tail may be wagging the dog much more than a superficial view would suggest. Trying to estimate an expected return for the entire asset class based on the historical returns of such a lopsided index is largely an analysis of its largest three country components – one of which is no longer even classified as a Frontier Market! While the demographic-led growth potential of these early-stage markets is one of the primary allures of Frontier Markets investing, these concentrations mask that case. The underlying drivers of Frontier Market index returns have not necessarily been the consumption growth stories that compel investors into the asset class. Take, for example, the case of Kuwait and Bangladesh as shown in Table 1: Table 1: Country Kuwait Bangladesh Difference MSCI FM Index Weighting 22.2% 2.4% 19.7% S&P Frontier BMI Weighting 17.4% 3.7% 13.7% Market Cap of Local Exchange (USD bn) 94 34 60 3M Average Traded Value (USD mm) 55 57 -1 Market Cap to GDP % 52.5% 18.0% 34.5% Number of Liquid Listed Companies 76 92 -16 GDP (USD bn) 179 187 -7 GDP Per Capita 44,844 1,179 43,665 Population (NYSE: MM ) 4 158 -154 Source: IMF World Economic Outlook, Bloomberg. Economic data from the IMF is for calendar year 2014. Market data is as of May 31st, 2015. “Liquid listed companies” is defined as locally-listed stocks with a 3-month average dauly traded value over $100,000 and median daily traded value over $25,000. Kuwait enjoys a 14-20% higher weighting in the MSCI FM Index and the S&P Frontier BMI than Bangladesh. Both markets have similar total GDP, a similar number of liquid listed stocks and similar market liquidity. Which of these two markets, however, appears to have more room for future growth and development? Bangladesh stands out with its massive population, low per capita GDP, and a lower market capitalization to GDP ratio. While these metrics simplify the nuanced growth stories for both countries, it is our view that Bangladesh has far more desirable “Frontier Markets” characteristics than does Kuwait. Nonetheless, the returns of the MSCI FM Index have been far more influenced by underlying drivers of the Kuwaiti market than those of the Bangladeshi market due to the index’s market capitalization-based weighting methodology. The returns of Frontier Markets equity indices are also affected by the annual reclassification of countries by market development status. As countries develop, they are reclassified as Emerging Markets, and as new Frontier stock markets open, they can attain “Frontier Markets” status. Countries can also be “demoted” from Emerging to Frontier Markets status, as was the case in MSCI FM Index with Morocco (2013), Argentina (2009), and Jordan (2008). (Argentina is also in the S&P Frontier BMI and currently accounts for 15% of the index. Astonishingly, unlike the MSCI FM Index, the S&P Frontier BMI includes local Argentinian shares that are impractical for foreigners to own due to capital controls.) Since its launch on December 18th, 2007, the MSCI FM Index has seen eight new countries join and three exit the index. The effects of country reclassifications on Frontier Markets index returns are most pronounced when countries are upgraded to “Emerging Markets” status. This can most recently be seen during the time period between MSCI’s June 10th, 2013 announcement that the UAE and Qatar would be promoted to its Emerging Market index effective June 1, 2014 and their exit, one year later, from its Frontier Markets index. At the time of MSCI’s announcement, both countries collectively accounted for almost one third of the entire MSCI FM Index. During this 12-month time period, the MSCI UAE Index and the MSCI Qatar Index rose 97% and 55%, respectively, before declining 24% and 22%, respectively, during the month of June 2014. As a result, the MSCI FM Index was up 20% during the first six months of 2014 with the UAE and Qatar accounting for a staggering 72% of that total return according to a recent report by FIS Group. An analysis of the historical returns of an index that has changed its composition so drastically and is constructed without diversification considerations masks the underlying opportunities in Frontier Markets and is a dangerous starting point for extrapolating future returns. Pick an Index any Index … To demonstrate how returns can vary depending upon the index and the weighting methodology it employs, we have constructed four custom indices using the same constituents as the S&P Frontier BMI (see Table 2). We also show the MSCI FM Index, which uses a different country universe than the S&P Frontier BMI. However, because it is less diversified with only 127 stock constituents versus 579 in the S&P Frontier BMI, the S&P Frontier BMI constituents were chosen to construct the custom indices. The equal-weighted index shown is derived by assigning each constituent of the S&P Frontier BMI an equal weight in the index. We also weighted the countries by population and by total GDP. For these two indices, we weighted the companies within each country by market capitalization. Lastly, we weighted each company by its size using annual sales instead of market capitalization. The point of this exercise is not to promote one Frontier Markets index over another since most have large concentrations, as Table 3 shows, but rather to demonstrate the variability of returns from reasonable indices constructed from the same constituents (excluding, of course, the MSCI FM Index, which has its own constituent universe). Table 2: Source: MSCI Barra, S&P Dow Jones, Business Monitor International, Bloomberg, LR Global Table 3: Source: MSCI Barra, S&P Dow Jones, Business Monitor International, Bloomberg, LR Global As Table 2 shows, yearly comparisons between the indices vary greatly with the biggest difference between the highest and lowest annual return of 24% occurring in 2009, where a sales-weighted index outperformed the MSCI FM Index by the largest amount. Likewise, the boost the MSCI index received from the removal of UAE and Qatar in 2014 can be seen in its outperformance in 2014 (The S&P Frontier BMI also removed these two countries in 2014, but not until September after both markets had fallen from their peaks at the end of May. Other weighting differences also influenced the variant returns). As the table shows, while there is a broad range of historical returns from which an investor can choose to help formulate future return expectations, each index comes with different biases and shortcomings. In addition, given the limited amount of historical data (under a decade of “live” index results), it is hard to argue that any of these indices can be used to anchor future return expectations (S&P Frontier BMI inception is 10/31/2008 and the MSCI Frontier Markets Index inception was on 12/18/2007). Implications for Manager Evaluation Flawed indices also obfuscate manager evaluation when used as benchmarks. For example, it is common for investors to separate an investment manager’s return attribution between stock selection and allocation versus the benchmark. This attribution analysis is an attempt to better understand the source of the manager’s returns and validate the consistency of the manager’s professed style. If returns are mostly coming from geographic and/or sector allocation, then a top-down style of investing is assumed. If returns are being generated from individual stock selection, a bottom-up style is inferred. In the case of Frontier Markets indices where there is a huge weight to financials, however, it is highly likely that Frontier Markets managers will never be overweight this sector and will most likely underweight financials in the interest of common sense diversification. Any underweight in one sector by definition implies an overweight in another sector or sectors. Does this mean the Frontier Markets manager is making top down strategic decisions to sector allocation or simply employing common sense diversification? An all too familiar binary decision is forced upon managers with regard to how closely to match the concentrated index exposures. Implications for Risk Expectations in Frontier Markets Just as return expectations in Frontier Markets are clouded by the flawed Frontier Markets indices, so too are the risk expectations for the asset class. With the birth of Modern Portfolio Theory in 1952 (Markowitz), investment risk became defined as the standard deviation, or volatility, of returns. If the historical returns are sampled from a flawed index such as one of the major Frontier Markets indices, this risk measure is also distorted. In a previous LR Global white paper (“Risk in Frontier Markets: Overcoming the Misperceptions.” May 2014) we examined the riskiness of Frontier Markets. Using the Modern Portfolio Theory definition of volatility, we analyzed Frontier Markets risk by calculating the standard deviation of individual Frontier Market country returns. Using ten years of rolling three-year weekly US dollar returns, we found that the median standard deviation of the Frontier Market country returns were consistently less volatile than Emerging Markets country returns and surprisingly less volatile than Developed Markets in six out of ten years (see Chart 4). Chart 4: Source: Sean Wilson, Brent Clayton, & Ha Ta (2014). “Risk in Frontier Markets: Overcoming the Misperceptions.” LR Global White Paper. However, it is also worth considering a different mindset of risk that does not assume investors are perfectly rational and that markets are efficient, as Modern Portfolio Theory requires. The booms and busts of individual Frontier Markets, the relative lack of institutional investors and research coverage as well as the opaque nature of these immature markets suggest that Frontier Markets are inefficient. Thus, a different notion of risk may be needed. Warren Buffet, a disciple of Benjamin Graham, explained why volatility is a poor measure of investment risk in a 1994 Berkshire Hathaway Annual Meeting : “For owners of a business – and that’s the way we think of shareholders – the academics’ definition of risk is far off the mark, so much so that it produces absurdities. For example, under beta-based theory, a stock that has dropped very sharply compared to the market – as had Washington Post when we bought it in 1973 – becomes ‘riskier’ at the lower price than it was at the higher price. Would that description have then made any sense to someone who was offered the entire company at a vastly-reduced price?” 15 In Frontier Markets, we also see volatility in individual markets and sectors as a potential source of opportunity and not risk. Fortunately, there are over 50 countries that comprise the broader Frontier Markets universe, and some of the biggest opportunities we have identified and exploited have been the result of extreme volatility in one or more countries. Would the Real ” Benchmark Risk ” Please Stand Up Thanks again to Modern Portfolio Theory, a new sub-category of risk was born. “Benchmark risk,” or, as it is more commonly known, “active risk” measures the amount of “risk” an investment manager takes by constructing a portfolio that is different than the benchmark it seeks to outperform. Studies conducted by academics and consultants over the past five years show that active managers who deviate significantly from their benchmarks have outperformed their more benchmark-like peers. According to researchers at Yale University, managers with an Active Share, one measure of active risk, of greater than 80% beat their benchmarks by 2.0% to 2.7% before fees. If, however, the benchmark is not diversified properly and constructed sub-optimally as current Frontier Markets indices are, then benchmark risk should really be literally thought of as just that, benchmark risk . In an asset class often assumed to be highly risky and not for the faint of heart, one might assume that managers should seek to minimize active risk. In light of these studies and the aforementioned flaws of Frontier Markets benchmarks, however, Frontier Markets managers should really be encouraged to seek out active risk. Conclusion Since Farida Khambata of the International Finance Corporation coined the term “Frontier Markets” in 1992, Frontier Markets have grown into a market segment distinct from traditional Emerging Markets with growing interest from investors and asset allocators. Much of this interest has occurred only over the past decade, which has accounted for the lion’s share of asset growth. It is important that investors interested in Frontier Markets understand the shortcomings of the major indices when considering an allocation or monitoring an existing allocation. In a subsequent paper, an alternative solution to existing Frontier Markets indices that will provide a better tool for monitoring and understanding the asset class will be discussed. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.