CEF Portfolio Generates 9% Income With Reasonable Risk

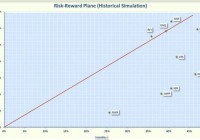

Summary The CEF portfolio had an average distribution of 9.4% coupled with lower risk than the S&P 500. The CEF portfolio is diversified among many types of funds including bonds, preferred stocks, equities, and covered calls. Most of the selected CEFs are selling at historically large discounts. As an income focused investor, I’m a fan of Closed End Funds (CEFs), and have written many articles on Seeking Alpha discussing their risks and rewards. Many CEFs have recently taken it on the chin because of fear that the Fed may begin raising rates. To my mind, this has created CEF bargains among many asset classes. This article constructs a diversified portfolio of CEFs that are selling at large discounts and also have reasonable risk-versus-reward profiles. Below is a summary of the CEFs I have selected. I apologize in advance if I did not include your favorite CEF and I welcome alternative suggestions from readers. The data is based on the 2 October market close. BlackRock Corporate High Yield Fund (NYSE: HYT ). This is one of the largest high yield CEFs with a market cap of $1.3 billion. Over the past 5 years, this CEF has sold for a both discounts and premiums. Premiums were relatively rare and reached a high of 6% in 2012. The fund typically sells at a discount, averaging about 5% over the past 5 years but increasing to a 12% average during the past year. The current discount is 15.2%. The portfolio is a combination of high yield bonds (87%) and equities (7%). The fund utilizes 31% leverage and has an expense ratio of 1.3%. The distribution is 8.7%, funded by income with a small amount of Return of Capital (ROC). The ROC is typically only about 1% of the total distribution. Brookfield Total Return Fund (NYSE: HTR ). This fund focuses on mortgage backed securities (MBS). Over the past 5 years this CEF has sold primarily at a discount. The 5 year average discount was 5% but the discount has grown to a 9% average over the past year. The current discount is 16.5%. The portfolio consists mostly of MBS and asset backed securities with the majority coming from the commercial and residential non-agency sectors. About 40% of the bonds are investment grade. The fund utilizes 28% leverage and has an expense ratio of 1.3%. The distribution is 10.9%, funded by income with no ROC. Nuveen Credit Strategic Income Fund (NYSE: JQC ). JQC has a market cap of about $1.1 billion and is the largest CEF focused on floating rate loans. Over the past 5 years, this CEF has sold mostly at a discount. The only time this fund sold at a premium was a short period in 2013. The five year average discount is 8% and the one year average is 12%. The current discount is 15.2%. The portfolio consists of a combination of floating rate loans (68%) and corporate bonds (19%). Less than 10% of the holdings are investment grade. The fund utilizes 38% leverage and has an expense ratio of 1.8%. The distribution is 7.6%, funded by income with no ROC. AGIC Convertible and Income Fund II (NYSE: NCV ). This fund focuses on convertible securities. Over the past 5 years, this CEF has sold mostly at a premium, sometimes as high as 15%. It was not until the second half of 2015 that the fund, began selling at a discount. The five year average was a premium of 7% and the 1 year average was a premium of 5%. The current discount is 14.4%. The portfolio consists of a combination of convertible bonds (58%) and high yield bonds (41%). Less than 10% of the holdings are investment grade. The fund utilizes 33% leverage and has an expense ratio of 1.2%. The distribution was recently reduced but is still 13.3%. The distribution is funded by income with no ROC. Nuveen Preferred Income Opportunities Fund (NYSE: JPC ). This fund focused on preferred shares. Over the past 5 years this CEF has sold only for a discount. The smallest discount was about 1% in 2012. The 5 year average discount is 9% and the 1 year average discount increased to over 10%. The current discount is 11%. The portfolio consists primarily of preferred stock (88%) with a small amount of equities (6%). The fund utilizes 29% leverage and has an expense ratio of 1.7%. The distribution is 9%, funded by income with no ROC. Cohen Steers Quality Income Realty Fund (NYSE: RQI ). This fund is focused on REITs. Over the past 5 years this CEF has sold only at a discount. The discount has oscillated between less than 1% to over 14%. The 5 year average has been a discount of 8% but the 1 year average has increased to a discount of 12%. The current discount is 12.5%. The portfolio consists of a combination of REITs (80%) and preferred stock (19%). The fund utilizes 25% leverage and has an expense ratio of 1.9%. The distribution is 8.6%, funded by income with no ROC. Eaton Vance Enhanced Equity Income Fund II (NYSE: EOS ). This is a covered call fund. Over the past 5 years this CEF has sold for a both a discount and a premium, but mostly at a discount. The premium was as high as 5% in 2010. The premium turned into a discount in 2011 and has stayed at a discount ever since. The discount sunk to 15% in 2011 but has been improving in recent years. The 5 year average has been a discount of about 8% and the 1 year average is only 5%. The current discount is 8.5%. The portfolio consists equities that are used for call writing on about 50% of the portfolio. The fund managers have a flexible mandate and can invest in all size companies but most are medium to large cap. The fund does not use leverage and has an expense ratio of 1.1%. The distribution is 8.4%. The fund has a small amount of ROC but this is not unusual for covered call funds. Cohen & Steers Infrastructure Fund (NYSE: UTF ). This fund focuses on utilities. Over the past 5 years this CEF has always sold at a discount. The discount has grown larger in 2015. The 5 year average has been a discount of about 11% and the 1 year average is 13%. The current discount is 16.8%. The portfolio consists of investments in utility and infrastructure companies. The portfolio contains 80% equities, 10% bonds, and 5% preferred shares. About 60% of the holdings are domiciled in the US. The fund utilizes 29% leverage and has an expense ratio of 2%. The distribution is 8.5% funded by income and capital gains with no ROC. The characteristics of an equally weighted portfolio of these CEFs are summarized in Figure 1. The portfolio has an average distribution of 9.4%, which definitely achieves the objective of high income. The average discount is also large at 14%. (click to enlarge) Figure 1: Portfolio averages Even more important than the value of the discount is how it relates to the average discounts over the past year. This is measured by a metric called the Z-score, which is a statistic popularized by Morningstar to measure how far a discount (or premium) is from the mean discount (or premium). The Z-score is computed in terms of standard deviations from the mean so it can be used to rank CEFs. A good source for Z-scores is the CEFAnalyzer website. A Z-score more negative than minus 2 is relatively rare, occurring less than 2.25% of the time. With the exception of JPC and RQI, the selected CEFs are selling at historically large discounts as evidenced by the large negative Z-score. Both JPC and RQI have large discounts but the discounts are close to the average discount for the year. Figure 2 shows the allocation among asset classes as: bonds (50%), preferred stocks (16%), and equities (33%). Most of the equity portion is hedged by using covered calls. Thus, overall this is a defensive portfolio, which I believe is prudent given the current uncertainties in the market. (click to enlarge) Figure 2: Allocations among asset classes The portfolio looks promising in terms of income but total return and risk are also important so I plotted the annualized rate of return in excess of the risk free rate (called Excess Mu in the charts) versus the volatility for each of the component funds. The risk free rate was set at 0% so that performance could be easily assessed. I equated volatility with risk and used a 5 year look-back period from October 2, 2010 to October 2, 2015. The plot is shown in Figure 3. (click to enlarge) Figure 3. Risk versus reward for past 5 years. In the figure, the risk-versus-reward for each CEF is represented by a green diamond. The performance of the composite portfolio is shown by the blue dot. I also included the SPDR S&P 500 Trust ETF (NYSEARCA: SPY ) ETF as a comparison with the overall market. As is evident from the figure, the CEFs had a wide range of returns and volatilities. Were the returns commensurate with the increased risk? To answer this question, I calculated the Sharpe Ratio. The Sharpe Ratio is a metric, developed by Nobel laureate William Sharpe that measures risk-adjusted performance. It is calculated as the ratio of the excess return over the volatility. This reward-to-risk ratio is a good way to compare peers to assess if higher returns are due to superior investment performance or from taking additional risk. In Figure 3, I plotted a red line that represents the Sharpe Ratio associated with the composite portfolio. If an asset is above the line, it has a higher Sharpe Ratio than composite portfolio. Conversely, if an asset is below the line, the reward-to-risk is worse than the portfolio. You may be surprised that the volatility of the portfolio is smaller than the volatilities of the components. This is an illustration of an amazing discovery made by an economist named Markowitz in 1950. He found that if you combined certain types of risky assets, you could construct a portfolio that had less risk than the components. His work was so revolutionary that he was awarded the Nobel Prize. The key to constructing such a portfolio was to select components that were not highly correlated with one another. In other words, the more diversified the portfolio, the more potential volatility reduction you can receive. To be “diversified,” you want to choose assets such that when some assets are down, others are up. In mathematical terms, you want to select assets that are uncorrelated (or at least not highly correlated) with each other. I calculated the pair-wise correlations associated with the funds. The data is presented in Figure 4. All the CEFs had relatively low correlations with SPY and each other. The only large correlation is the covered call CEF with the S&P 500. This is not surprising since large and medium cap companies were used for writing covered calls. Overall, these results were consistent with a well-diversified portfolio and hence, the reduction in portfolio volatility. (click to enlarge) Figure 4. Correlations over the past 5 years. Some interesting observations are apparent from Figure 3. SPY generated a higher return than the portfolio but SPY also had a higher volatility. SPY and the portfolio had virtually the same risk-adjusted performance. Thus, I believe that the composite portfolio is a good tradeoff for the risk averse investor looking for income. To get additional views of the how the portfolio performed, I analyzed two other metrics. The first is graphed in Figure 5 and shows the growth of wealth over the 5 years period. The plot assumes that the portfolio is frequently rebalanced to maintain equal weighting. As illustrated by the graph, wealth grew at a steady pace over the 5 year period. (click to enlarge) Figure 5 Growth of wealth for CEF portfolio The value of the portfolio decreased a few times along the way. The second metric is plotted in Figure 6 and provides a measure of the draw downs that an investor would experience. The figure illustrates that you can expect periods of relatively large draw downs, which could reach as high as 14% in a few cases. Thus, the portfolio is best suited for long term investors who can weather moderate draw downs. Note that we are currently in a 10% drawdown period, which is similar to draw downs in the past. (click to enlarge) Figure 6. Draw downs associated with the CEF portfolio Bottom Line Many of the CEFs in this portfolio have recently taken price hits, which have resulted in large discounts. No one knows what the future may hold but if the future is anywhere close to the past, these CEFs will recover and the discounts will revert back to the mean. If this turns out to be true, you can receive high income while you wait. Overall I believe this portfolio provides high income with reasonable risk.