Tag Archives: government

A Word Of Caution About New Purchases In The Utility Sector

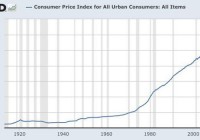

My first purchase of an electric utility stock was 400 shares of Duke Energy (NYSE: DUK ) around 1978. Somewhere along the way, I sold those shares for reasons that I no longer recall. I am not expressing a word of caution about the long term benefits that have flowed through buying and holding quality utility stocks and reinvesting the dividends. The ten year annualized total return numbers for a number of electric utility stocks are superior to the 7.83% annualized total return of the S&P 500 ETF (NYSEARCA: SPY ) through 2/13/15. Some examples include the ten year annualized performance numbers of American Electric Power (NYSE: AEP ), Dominion Resources (NYSE: D ), Edison International (NYSE: EIX ), NextEra Energy (NYSE: NEE ) and Wisconsin Energy (NYSE: WEC ) Ten Year Annualized Total Returns Through 2/13/15 Computed by Morningstar: AEP +8.09% D + 9.93% EIX + 8.72% NEE +12.15% WEC +13.03% Several other well known “utility” stocks have come close to matching the S & P 500 ten year annualized total return without the same decree of drama. AT&T +7.69% SCANA +6.86% Southern Co +6.75% Verizon Communications +7.54% The question that I am addressing now is whether new buys can be justified based on current yields and valuations. I started to look at this question a few days ago when making a comment here at SA about the impact of rising rates on REIT and utility stocks. Both of those industry sectors have attracted a large number of investors searching for yield. For many investors, REITs and utility stocks are viewed as “bond substitutes”. I started an analysis simply be looking at the current yield of the Utilities Select Sector SPDR ETF (NYSEARCA: XLU ), a low cost sector fund that owns primarily electric utility stocks. Yield: As of 2/12/15, the sponsor calculated the dividend yield at 3.28%. The attractiveness of that yield will depend on an investor’s view about the direction of interest rates. Notwithstanding the abundance of contradictory evidence, the Bond Ghouls have been predicting that a Japan Scenario will envelope the U.S. until the end of days, a slight exaggeration, based on the pricing of a thirty year treasury bond at a record low 2.25% yield recently. If an investor believes that deflation will alternate with periods of abnormally low inflation for the next 30 years, then the pricing of several long term sovereign bonds may at least appear to be rational rather than delusional. The current yields of a U.S. electric utility stock, with modest earnings and dividend growth, may even look good compared to those yields and the dire future predicted by those sovereign bond yields (U.S., Germany, Switzerland, Netherlands, Japan, etc.) The 30 year German government bond closed last Friday at a .92% yield. German Government Bonds – Bloomberg The average annual inflation rate in Germany between 1950-2015 was 2.46%. Just assume for a moment that the future will be similar to the past, with some hot and low inflation numbers and possibly a brief period of slight deflation. The .92% 30 year German government bond would produce a 1.54% negative annualized real rate of return before taxes. The average annual U.S. inflation rate between 1914-2015 was 3.32%. When the 30 year treasury hit a 2.25% earlier this year, and assuming the historical average annual rate of inflation, the total annualized return before taxes would be -1.07%. The first item for investors to consider is why are so many predicting the Japan Scenario given the recent U.S. economic numbers and the non-existence of a single annual deflation number since 1955 other than the understandable -.4% reported for 2009. Consumer Price Index, 1913- | Federal Reserve Bank of Minneapolis When looking a long term charts, it is hard to see the underlying support for what the Bond Ghouls are saying about the future. (click to enlarge) (click to enlarge) (click to enlarge) The DSR ratio highlights that U.S. households have more disposable income after debt service payments to pay down debt, to spend, or to save. I view this chart as bullish long term for stocks but not far bonds. I have been making the same point here at SA for over three years now without convincing a single bear of my point. An example of banging my head against the wall was a series of comments to this SA article published in February 2013: Sorry Bulls, But This Is Still A Secular Bear Market-Seeking Alpha It is interesting to go back and read some of those comments from other investors. Yes, I am referring to the bears here who were predicting a bear market starting in 2012 just before the S & P 500 took off on a 700 points move up, not down by the way. (click to enlarge) (click to enlarge) (click to enlarge) (click to enlarge) (click to enlarge) Links to some other relevant charts: Financial Stress-St. Louis Fed Household Financial Obligations as a percent of Disposable Personal Income-St. Louis Fed Mortgage Debt Service Payments as a Percent of Disposable Personal Income-St. Louis Fed Charge-Off Rate On All Loans, All Commercial Banks-St. Louis Fed Retail Sales: Total (Excluding Food Services)-St. Louis Fed E-Commerce Retail Sales-St. Louis Fed Light Weight Vehicle Sales: Autos & Light Trucks- St. Louis Fed Corporate Net Cash Flow with IVA -St. Louis Fed ISM Non-manufacturing-St. Louis Fed And what are the current economic statistics (not the ones generated through reality creations) that support the long term Japan Scenario prediction that underlies current intermediate and long term bond prices? I will just drag and drop here my recent discussions of this data. Is that dire long term U.S. inflation and growth forecasts embedded in those historically abnormal yields justified by the 5% real Gross Domestic Product growth in the 3rd quarter perhaps slowing to 3% in the 2014 4th quarter with personal consumption expenditures accelerating; the lowest readings on record in the debt service payments to disposable income ratio (DSR) ; the decline in the unemployment rate to 5.7% with 257,000 jobs added in January with a 12 cent rise in average hourly earnings and a 147,000 upward revision for the prior two months; a decline in the 4-week moving of initial unemployment claims to the historical lows over the past four decades; the long term forecasts of benign inflation; a temporary decline in inflation caused by a precipitous drop in a commodity’s price, the consistent and long term movement in the ISM PMI indexes in expansion territory; capacity utilization returning to its long term average where business investment has traditionally increased by 8% , or perhaps some other “negative” data set. That kind of data has to be negative rather than positive, right? Even the government’s annual inflation numbers for 2014 showed a + 3.4% increase in food prices; a 2.4% increase in medical service costs, a 2.9% increase in shelter expenses, and a 4.8% increase in medical commodities. The BLS called the rise in food prices “a substantial increase” over the 1.1% rate for 2013. While I am not predicting here a return to $80+ crude, the price may have already bottomed and the disinflationary impact created by the 50%+ decline is consequently a temporary abnormality that will self correct with supply and demand moving back into balance. Consumer Price Index Summary While it is too early to know whether intermediate and long term rates have started to turn back up, the recent movement is certainly cautionary and resembles the lift off in interest rates that started in May 2013, when the ten year was at a 1.68% yield, and culminated in a rate spike to 3.04% for that note by year end. 7 to 30 Year Treasury Yields 2/2/15 to 2/13/15 Daily Treasury Yield Curve Rates When looking at that table, it is important to keep in mind that a ten year treasury yield of 2.00% is abnormally low by historical standards since 1962: (click to enlarge) 10-Year Treasury Constant Maturity Rate – FRED – St. Louis Fed And this brings me to my word of caution about utility stocks. A 3% dividend yield is not too hot using history as a guideline. To be justified, the investor will have to buy into most of the Bond Ghouls Japan Scenario unfolding in the U.S. rather than a gradual return to something close to normal inflation and GDP growth. Valuation: For me, valuation is the kicker. What S & P sector currently has the highest P.E.G. ratio? Back in the late 1990s, I would have said technology stocks without looking to verify the answer. I said utility stocks now and I took the time to verify that response. An investor can download the current E.P.S. estimates for the S & P 500 and the various sectors from S & P in the XLS format. I can not link the document here, but anyone interested can find it using the exact google search phrase “XLS S & P Dow Jones Indices”. It should be the first result. As of 2/12/15, the estimated forward 5 year estimated P.E.G. for the utility sector is a stunningly high 3.65, and this sector has traditionally been one of the slowest growing sectors. Technology is at a 1.27 P.E.G. The P/E based on estimated 2015 earnings is 17.12. The data given by the sponsor of XLU immediately set off alarm bells when I looked at it recently. In addition to the vulnerability of stock prices due to a rising interest rate environment, the sponsor calculated the forward P/E at 17.14, which is normally a non-GAAP ex-items number, a 7.23 multiple to cash flow, and a projected 3 to 5 year estimated E.P.S. growth rate of only 4.86%, or a similar P.E.G. to one calculated by S & P and mentioned above. The Vanguard Utilities ETF (NYSEARCA: VPU ) has another set of data that is even more concerning than the XLU valuation information: As of 1/31/15, this fund owned 78 stocks, with a P/E of 20.8 times and a 2% growth rate. Portfolio & Management Taking into consideration the possible or even probable rise in rates, the low starting yields for utility stock purchases now, the high P/E and abnormally high P.E.G. ratio, I am just saying be careful out there. I will be discussing in my next blog a reduction in my position in the Duff & Phelps Global Utility Income Fund Inc. (NYSE: DPG ), a closed end fund that has performed well for me since my purchases. I may not start writing that blog until Monday after taking the time to write this one in my usual stream of consciousness writing mode. CEFConnect Page for DPG According to Morningstar, the Utilities Select Sector ETF ( XLU ) had a 2014 total return based on price of 28.73%, much better than SPY, and was up YTD 2.33% through 1/31/15. The tide has turned with the recent rise in rates since the end of last month. The total return for XLU is now at -4.34% YTD through 2/12/15. Just as a reminder, I only have cash accounts and consequently do not short stocks. I do not borrow money to buy anything. I have never bought an option or a futures contract. I am not paid anything to write these SA Instablogs or SA articles or any of my almost 2000 blogs written since early October 2008, mostly very long ones, published at Stocks, Bonds & Politics . I do not own any of those short ETFs. I am currently substantially underweighted in the Utility sector.

Korea Electric Power Corporation (KEP) Q4 2014 Results – Earnings Call Transcript

Korea Electric Power Corporation (ADR) (NYSE: KEP ) Q4 2014 Earnings Conference Call February 11, 2015 02:30 AM ET Executives Bon-Woo Koo – VP and Treasurer Changyoung Ji – Senior IR Manager Analysts Pierre Lau – Citibank Yun Hee-do – Korea Investment Securities Joseph Jacobelli – Bloomberg Intelligence Sujin Bum – Samsung Securities Bon-Woo Koo Good afternoon. This is Bon-Woo Koo, Vice President and Treasurer of KEPCO. On behalf of KEPCO, I would like to thank you all for participating in today’s conference call to announce earnings results for the fourth quarter of 2014. We will begin with a brief presentation on the earnings results, which will be followed by a Q&A session. Today’s call will be presented in both Korean and English. Please note that the financial information to be disclosed today is on a preliminary, unaudited, and consolidated basis in accordance with KIFRS. Any comparison will be on a year-on-year basis between 2013 and 2014. Business, strategies, plans, financial estimates, and other forward-looking statements included in today’s call will be made based on our current expectations and plans. Please be noted that such statements may involve certain risks and uncertainties. Now Senior IR Manager, Mr. Changyoung Ji will begin with an overview of earnings results of the fourth quarter of 2014, first in Korean and repeated in English. Changyoung Ji Now we will provide the overview in English, starting with operating income. In the fourth quarter of 2014, KEPCO recorded a net operating income of KRW5.78 trillion. Taking a closer look, operating revenues increased 6.4% to KRW57.47 trillion. This was attributable mainly to 4.9% increase in power sales revenue, totaling in KRW52.62 trillion and 34.7% increase in revenue from the overseas business amounting to KRW3.22 trillion. Moving on to main operating costs, cost of goods sold, SG&A expenses decreased 1.6% to KRW61.68 trillion. Fuel cost decreased 14.9% to KRW20.59 trillion. Power generation affected by the lower power demand decreased 1.4% and unit cost of fuel declined by 13.7%. Meanwhile, purchased power cost increased 11.2% to KRW12.60 trillion. Unit cost of purchase power decreased 5.6% because of the decrease of S&P caused by the increase of new highly efficient top line and purchase volume increased KRW16.1 trillion. Depreciation cost rose 5.3% to KRW6.09 trillion, mainly due to the newly constructed power substations and new facility additions by power plants. Now let me explain KEPCO’s non-operating segment. Net financial loss was KRW2.25 trillion in the fourth quarter of 2014, which was improved by KRW47 billion. As a result of the foregoing, we recorded a consolidated net income of KRW2.79 trillion in the fourth quarter of 2014. This concludes the overview of KEPCO earnings results for the fourth quarter of 2014. Now let me move on to the Q&A session. Q&A session will be hosted by Mr. Bon-Woo Koo. Question-and-Answer Session A – Bon-Woo Koo This is Bon-Woo Koo, I’m joined with our IR committee members in charge of major business areas at KEPCO. We are prepared to take any questions. Since we will proceed in both Korean and English all Q&As will be interpreted. Please make sure your questions and answers are brief and clear. Operator Now Q&A session will begin. (Operator Instructions). The first question will be given by Mr. Pierre Lau from Citibank. Please go ahead, sir. Pierre Lau I have three regarding your 2014 results. The first one is regarding your unit LNG cost, in the fourth quarter it is up 7.3% year-on-year. So I would like to know why your unit LNG cost increased in the fourth quarter year-on-year despite of the lower oil prices. And also what is your guidance for your unit LNG cost in 2015? That’s question number one. Question number two is what is your guidance for your unit coal cost in 2015? And question number three is what is your expected generation mix for coal and nuclear in 2015? These two kinds of fuel generate 35% and 46% of your total generation in 2014 respectively. And also will you buy net IPP next year — this year in 2015 given that you have more capacity now. Bon-Woo Koo To answer your first question first we have witnessed the drop in the oil price starting in September and October last year and there is inevitably time lag between oil and LNG price decrease and we expect the time lag to be about four to six months’ time. Having said that, we saw the oil price drop in the fourth quarter or starting in October last year and we expected to see that impact on LNG unit price in early 2015. On our guidance for the fuel unit cost for 2015 is as following. For coal, we anticipate the coal price should be KRW120,000 per ton and for LNG, we expect the LNG price to be KRW820,000 per ton. And on the fuel mix to answer your third question, on the fuel mix we believe the LNG to be 10% of overall fuel mix and quarter reporting 9% and nuclear to be 38%. Pierre Lau Okay if LNG 10%, nuclear 48% and coal how many percent? Bon-Woo Koo Coal 49%, nuclear 38% and LNG 10%. Pierre Lau And lastly we will finance output from IPP in 2015. Bon-Woo Koo To answer your question on the energy mix if you look at the IPP proportion, the current number for IPP from 2014 was 14% of overall volume. But in 2015 we expect the number to go up to 19%. And the reason for that is that we are going to increase the co-generation for the high efficient power generation in 2015. Did that answer your question. Pierre Lau Yes thank you. Operator Currently four participants are waiting with your question. The following question is by Mr. Hee-do Yun from Korea Investment Securities. Please go ahead sir. Hee-do Yun Thank you for giving me the opportunity to ask the question. I have two questions first it seems that your operating profit performance is slightly less than we have expected. We believe the reason for that is because executed about KRW350 billion to 3 billion [ph] nuclear waste of Korea Hydro and Nuclear Power Generation Corp. Could you elaborate on what that is really and the back ground of it? Is it going to be a one-time expense for KEPCO? We understand that we launched a project to have a treatment facility for the nuclear waste in [indiscernible], we spent KRW300 billion as a one-time investment. Is this investment by KHNP a similar type of investment or a different one? That’s question number one. The second question is on the dividend payout ratio. Coal gas has just announced that their dividend payout would be about 25%, which is lower than what market has expected. How is KEPCO doing in terms of your discussion with the government in determining your dividend payout ratio? Bon-Woo Koo So clearly our operating profit is lower by about KRW300 billion than market expectation and that is because we have allocated additional cost for trading the waste of nuclear power plant which was ordered by the government. All of that expense was executed in fourth quarter alone and we didn’t have an expense allocated for the first quarter to third quarter of this year. So hence the accumulated expense that we have set aside for this quarter was KRW320 billion and which has resulted in KRW300 billion GAAP in our expected operating profit. This is one-time expense that we have accumulated and moving forward we’ll be accumulating about KRW50 billion per year moving forward under this same expense category. This is however different from the liability for commissioning the nuclear power plant cost, which is a separate line item on our accounting book. To answer your second question, we’re currently in discussion with the government in terms of determining our dividend payout ratio. Current estimation is that our dividend payout ratio will be higher than previous year and we’re discussing with the government to have this impaired ratio higher than 25%. Follow up question for the first question is that will the KRW320 billion for this fourth quarter this year will no longer take place in the subsequent year and going forward there will be only KRW50 billion expense allocated for this category? Is that correct? And what was the reason behind accumulating KRW350 billion this year? And the answer is because we are adding incremental cost to that waste treatment cost because we want to support the region that is going to set up this facility for shipping nuclear waste. And as part of that we have increased the budget in the fourth quarter of this year to support those regions. Operator The following question is by Mr. Shin Ji Yoon from KTB Investment Securities. Please go ahead sir. Shin Ji Yoon I have two questions. First is on the dividend payout ratio. You have stated that you are going to discuss with the government to maintain about 25% dividend payout ratio. Is that going to consider the consolidated balance sheet fees? That’s question number one. Second question is on your generation mix. You said that KEPCO will have a percent LNG and its lower than previous year and IPP ratio will be 19%, which is higher than year-on-year. Is those numbers correct? I would like to verify those numbers. Having said that in 2015, it seems that the base load will be also coming from the new nuclear power plant as well as in the core power plant. What are the neutralization assumptions you’re taking into for 2015 in terms of overall coal generated power and nuclear generated power? Bon-Woo Koo To answer your first question on dividend payout ratio it will be based on the individual Company, not consolidated leases. And because of that the dividend payout will be slightly lower or decreased than previous payout ratio which is before we were introducing the KIFRS in our accounting system. That’s why we’re discussing with the government to maintain 25% or above at the minimum. However the details haven’t been determined and we will let the market know as soon as something has been decided. To answer your second question on the generation mix where the LNG proportion will slightly go down and IPP will go up to 19%, we will verify those numbers for you and get back to you with the accurate number later on and communicate back to you on that. On the utilization rate for different energy mix is that for nuclear it will be about the similar level with 2014 at 84.4%. For coal however there will be slight decrease from 2014 to 93.2%. Shin Ji Yoon On the question on the coal and the nuclear energy mix, so there won’t be any additional increase for coal power plant but for nuclear power plant are we going to consider both Shin Wolsong and Shin Kori or just one of them? Bon-Woo Koo To answer that question in 2015 we said the utilization rate will be 84.4% and that number considers both Shin Wolsong No. 2 and Shin Kori No. 3 facility. Operator The following question is by Joseph Jacobelli from Bloomberg Intelligence. Please go ahead sir. Joseph Jacobelli I wanted some clarity with regards to power plants commissioning schedule in 2015 and 2016, including nuclear and another other coal or gas plants that you maybe commissioning during the period. And the second question is with regards to the debt management. How are the other assets sales going and the overall debt management going? Bon-Woo Koo To answer your first question, for nuclear power plant we are going to add two nuclear power plant in the second half of 2015 which is Shin Wolsong No. 2 and Shin Kori No. 3 power plant. As for coal power plant in 2015 we expect to have 2 power plant within 1000 megawatt capacity by end of the year and in 2016 we expect to add six more on coal powered power plant which will be providing capacity of 8000 megawatts in total. On our equity sales plan, we plan to sell the equity of our KEPCO KPS equity, which we own about 3% and for KEPCO EMC company we plan to sell our 50.4% of the equity that we own and for KEPCO industry development that we own, we planned to sell our 29% of our equity that we own, which is all the equity that we own for that subsidiary. Joseph Jacobelli If I may just a supplement question with regards to the first answer. What about outside Korea? Any commissioning of invested power plants outside Korea please? Thank you. Bon-Woo Koo The new power plant for the overseas office, we’re currently pursuing the project at the moment, but nothing has been determined looking here at the moment. Operator The following question is by Mr. [indiscernible] Private Investor. Please go ahead sir. Unidentified Analyst Your overseas revenue has gone up by 6% – 7%. What has driven this increase in revenue coming from overseas margin? Could you share with us your revenue trend in overseas market in the last five years and what is your expectation for just here? Bon-Woo Koo To answer your question on the overseas business, most of our revenue generated in overseas market is coming from our projects in UAE which has contributed by KRW780 billion this year in revenue. There are other revenues coming in from our outsourcing work from transmission and distribution projects, as well as pipe construction projects. But most of our revenue from overseas market is coming from our UAE project. To elaborate on our overseas business performance, we are seeing our business grow in the Philippines. Also in the second half of last year we have seen the commercial operation of our Mexican power plant in Norte. That has also contributed in our increased revenue. We’re also seeing revenue growth in our China project as well. Also we had a commercial operation for the Amman Asia project in April of 2014. To share with you the profitability level coming from our overseas business is that for our hydraulic and thermal power energy, we’re seeing the profitability compared to our revenue at 15% to 20%. Unidentified Analyst Could share with us the trend for the last five years in terms of your overseas revenue and your expectation for this year? Bon-Woo Koo The numbers that we have shared with you at the moment is our historical revenue for the last three years. We don’t have the numbers for the past years. We will be more than happy to share that with you when we have those numbers. To give you a brief trend on our five year performance for the overseas business is that our revenue in 2011 for the overseas revenue was KRW1.7 trillion whereas this it’s KRW3.2 trillion. In terms of revenue mix overseas business was 3.9% in 2011 but now it’s 5.6% which is based on a consolidated basis. Unidentified Analyst And what is your expectation for this year? Bon-Woo Koo Let us follow up with you on that question. Currently we do not have the numbers for this year’s items. Operator The following question is by Ms. Sujin Bum from Samsung Securities. Please go ahead madam. Sujin Bum First question is on the operating expense for the UAE project. Can you share with us the operating expense? And second question, although it could be difficult for you to share the information regarding this at the moment, but could you if possible share with us your timeline for adjusting tariff this year? Is there any information that you can share with us at this moment? Next question is on the CapEx, it means that there are additional CapEx set aside for the nuclear and coal-fired power plant facility enhancement in 2015 and that’s a significant amount. What is the nature of this CapEx this year? Bon-Woo Koo To answer your first question on the cost of revenue for UAE project, we have seen the cost of revenue go up by — cost of revenue to be KRW2.2617 trillion for this year because we have seen significant progress into the project. To answer your second question on the tariff adjustment discussion with the government, we see that market has had a significant interest in the tax adjustment since the old price of trench [ph] starting in the fourth quarter in 2014. Although the fuel cost decrease is a factor that [indiscernible] have significantly, we’re also seeing some of the factors that drive up tariff such as the Transmission Act as well as the tax rate which is part of the policy cost that is raising tariff. We’re going to submit report on tariff to the government in June of this year and the tariff adjustment will take place afterwards. To answer your question on the CapEx on the power plant is for Thermal power plant, we plan to spend KRW3.3 trillion in construction of thermal power plant and for new renewable energy we have allocated KRW820 billion in CapEx for the new renewable energy. And in refining the power plant facility for thermal power plant the CapEx amounted to KRW1.4 trillion for this year. Just for your information when it comes to our power plant construction if you consider the overall approval process that we have to go through with the government for power plant construction, we assume that about 80% of the CapEx allocated with the project will be executed. Operator The following question is by Mr. [indiscernible] from Shinhan Finance Investment. Please go ahead sir. Unidentified Analyst First I have question on the CapEx following up the previous question. It seems that there is significant purchase set aside for the refinement of nuclear power plant facility and that number increases this year. Do you believe that the nuclear power plant utilization rate of 88% is feasible this year with such a large investment in enhancing these nuclear power plant? Because if you look at previous year, without such a huge CapEx being executed, we only saw 85% of utilization rate for the nuclear power plant. Also last year it seems that you’re setting a sight KRW2 trillion for additional power plant set up. Could you elaborate on those numbers? And third question is on the traffic adjustment. You’re going to be reporting on the total cost of power supply this year and will that include the investment coverage for the subsidiary as well? If not could you be able to share that with us? Bon-Woo Koo To answer your first question, on the nuclear power plant facility enhancement, the number does increase by about two fold this year compared to 2014. But the utilization rate is not 88%. It’s actually 84.8%. On the reason why we’re seeing the increase in CapEx for nuclear power plant is because to give you a high level answer that we are seeing enhanced criteria coming from the government side on the safety of these nuclear power plant which is leading to a higher quality requirement. We would like to share with you the details of that in a separate session. On the 2015 profit guidance, if we exclude the profit coming in from the headquarter sales in last year, we anticipate the number to be at similar level with 2007 at about KRW2 trillion. On our total cost of energy supply calculation, that is actually based off of our regulations set off Ministry of Trade Industry and Energy and KEPCO will be listed as an independent separate entity. Therefore we will not be considering the cost and CapEx on five GENCOs or our subsidiaries. However there our numbers will be reflected in terms of purchased energy cost only. Unidentified Analyst It’s not on a consolidated basis. It will be very difficult for us to anticipate a fair rate of return on your investment. Having said that is there any possibility that you’ll be willing to share with us this separate data for all the GENCOs? Bon-Woo Koo To answer your question the cost and the rate of return for our GENCOs is not directly reflected on the cash calculation of KEPCO. That is done independently by KEPCO. However the adjustment coefficient from the power market will be reflected. Operator The following question is by [indiscernible] from UBS. Please go ahead, sir. Unidentified Analyst First question is on your power demand or cash flow 2015. It seems that your CapEx is less than about KRW800 billion compared to last year. But having seen the enhanced fixed requirement on your facility and new project that is planned in your Company, we see about KRW2 trillion increases in those investment. So could you elaborate on that and is it safe to understand that the investment increase CapEx from KEPCO is offset by decreasing CapEx in the subsidiaries or GENCOs. Second question is on the utilization rate or your coal fired power plant. I would like to clarify the utilization rate. In 2014 you said 88% and in 2015 you anticipate the number to go up to 93.2%. Is that right? Bon-Woo Koo On our 2015 guideline on the power sales is that we see a 2.3% increase year-on-year in terms of power sales and our assumptions for GDP growth is at 3.7%. With the revenue increase at 2.3% we believe the profit to increase by 3.2% year-on-year. On your question on the CapEx, earlier this year yes, we did announce to the media that there will be KRW2 trillion in increase in our CapEx on the facilities. But however the total CapEx so much goes down when we consider the long term transmission and distribution investment cost on a year-on-year basis. When you translate that on our account that will actually decrease the overall CapEx investment and you’re right intense of our subsidiaries’ CapEx decrease offsetting our increase in CapEx by KEPCO. On your question on the coal-fired power plant utilization the rate was 88% in 2014. However we do not have the actual forecast number for 2015. So we use the five year average for the utilization rate for the coal-fired power plant. Our generation mix in 2015 is going to be 49%, which is an increase from 46%. So we also assume that the utilization rate will therefore increase. Unidentified Analyst Another follow up question on the dividend payout ratio. You said it’s going to be over on 25%. It seems up until 2007 your dividend payout was up to 30%. Is it safe for us to assume that level this year? But having had the consolidated basis, is it going to be much higher than the 25% level? Bon-Woo Koo The dividend payout ratio target for the government this year is 25%. However KEPCO is targeting 30% in discussing with the government. So we will do our best to have our dividend payout ratio at 30% level. Just to add to that we are aiming for 30% ex minimum, however currently we haven’t fully discussed this with the government yet. So we will let the market know as soon as something becomes concrete. Because we are approaching the end of our allocated time. We will accommodate just one last question. Operator Currently there are no participants to question. (Operator Instructions). Last question will be given by Pierre Lau from Citigroup. Please go ahead sir. Pierre Lau I have two follow up questions. The first one is your early guidance for coal cost in 2015 will be KRW121,000 per ton. But I find this number even higher than your actual coal cost KRW104,000 per ton. So why the guidance for coal cost unit cost in 2015 higher than the actual number in fourth quarter last year? And the second question is you just mentioned that you will submit your tariff review proposal to the government in June 2015. Why it takes so much time to submit only in June? Bon-Woo Koo To answer your question on the coal unit price, the last year the unit cost price for coal has dropped to a level that is very close to the production cost level. So there is actually no room for the coal price to drop further even if we see the huge drop in the oil price. That is why our guideline for 2015 is slightly above the unit cost of last year. And on your second question on why the submission to the government on the total cost of energy supply is scheduled in June, it is because the cost, although it is based on our budget base, we also have to reflect the previous year’s financial performance into those numbers. So once that financial statement is settled in March and finalized, then we need to do a separate accounting for calculating the tariff calculation, which will be done as a separate effort. Once that is done, we have to go through another auditing process and because of the series of administration process that we have to go through, is it only scheduled to be done in June. Changyoung Ji All right, we will conclude this conference call. Once again, thank you for joining us today. Thank you and good bye.