Vanguard Set To Move Into Muni Bond ETF Space

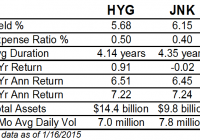

Vanguard Group, known for its low cost offerings, plans to make inroads to the increasingly popular muni bond ETFs space. Vanguard’s entry appears well timed, as the muni bond ETFs space has been on a roll since last year. In fact, the overall muni category managed to secure the third best position in 2014 having added 8.7%, its three-year highest. It’s not that the issuer is entirely new to munis. Presently, there are 12 actively managed Vanguard muni-bond funds worth $140 billion. The issuer expects the fund to be up for sale by the end of June. The fund will trade under the name of Vanguard Tax-Exempt Bond Index Fund . The Proposed Fund in Focus As per the SEC filing , the fund looks to track the performance of the investment-grade U.S. municipal bond market. The goal will be achieved by tracking the S&P’s National AMT-Free Municipal Bond Index. The index includes bonds having a minimum term to maturity greater than or equal to one calendar month. The “investor” share class will have to spend 0.2% in annual fees to own the fund. How Does it Fit in a Portfolio? Municipal bonds are great picks for investors seeking a steady stream of tax free income. Usually the interest income from munis is exempt from federal tax and sometimes even state taxes, making it especially attractive to investors in the high tax bracket looking to reduce their tax liability. The proposed fund too looks to follow munis that have their interests excused by U.S. federal income taxes and the federal alternative minimum tax (AMT). However, investors should note that tax-free bonds yield lower than taxable bonds. With the increase in the U.S. taxes, demand for municipal bonds has grown by leaps and bounds among high earners. Can it Succeed? There are quite a number of choices in the municipal bond space with iShares National AMT Free-Muni Bond Fund (NYSEARCA: MUB ) being the highest grossing ETF with about $4.2 billion. MUB tracks the S&P National AMT-Free Municipal Bond Index to provide exposure to a basket of 2,458 investment grade securities. The average maturity for the fund stands at 5.51 years, while duration is 6.33 years. The fund has a 30-day SEC yield of 1.58% and charges 25 basis points as expenses per year. Interestingly, the newly filed fund also follows the same index that MUB tracks. So it goes without saying that the proposed fund will face tough competition from the largest ETF in the space, i.e. iShares’ MUB. While the lack of first-movers advantage will be a negative for Vanguard, its ability to roll out a product on an ultra low price should give it an edge over many others presently on offer. Going by fundamentals, intermediate term munis offer great opportunities right now especially with the improving fiscal health of the U.S. states and a plunge in intermediate-to-long term yields. The only bump in the road ahead for Vanguard is its late entry to this space. It’s hard to predict how Vanguard’s new product would perform, but a low expense ratio should be the key to a sizable asset base or greater market share than iShares’ ultra-popular product.