Leveraged Long ETFs: Active Investment Now Best Long-Term Strategy

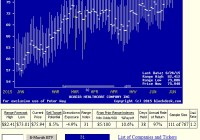

Summary Price sensitivity of these ETFs provide profitability guidance in portfolio asset allocation guidance, using prior experiences of current-level Market-Maker forecasts. Current overall market apprehensions offer heightened near-term price gain opportunities, using imbalances in ETF upside-to-downside price potentials. These are tactical opportunities for investors pursuing active investing strategies, not for passive buy&hold long-term index investors. Active investment strategy permits subsequent retreat to defensive posture when that is indicated by behavioral analysis of market-maker hedging activity. The current price outlook environment Market-makers [MMs] unintentionally signal their upside and downside price expectations by the hedging deals they accept in protecting firm capital put at risk while filling volume “block” orders from big-$ fund-management clients. We collect their expectation proportions and convert them into Range Index [RI] measures, where the value of each RI tells what percentage of the overall price range forecast lies below the current market quote. Here is today’s distribution of RIs for some 2500+ widely-held and actively-traded stocks and ETFs. Figure 1 (click to enlarge) (used with permission) Range Index values appear from time to time in a span from negative numbers (current price below bottom of forecast range) to sometimes (but not often) above 100 where the price is above the forecast range. The span is from excessively cheap at left (bounded) to grossly overpriced at right on the scale at bottom of Figure 1. The vertical scale is a count of subject investment alternatives at that level of RI. It might seem at first thought that a “normal” array of values would be centered around a RI value of 50, with equal-sized prospects of upside price change opportunity and downside price exposure. But since these are perceptions of risk-avoiding humans, the “normal” distribution is shifted toward the left, with an average of the whole population much closer to 40 than 50. Further, the continuing existence of Range Indexes measuring above 50, usually is found in securities having trend-following enthusiasts. So the current distribution indicates a diminished presence now of this mind-set in the investing public. At the other extreme, active bargain hunters usually minimize the presence of negative RIs. When collections of securities are stacked up at the lower bound of the Figure 1 scale, it confirms that market price decline concerns are being overdone, at least as MMs see the situation from their role. Here’s how we differentiate their perspective from that of the investing public. The influence of MMs is strongest in those big-cap issues where massive amounts of capital are most easily employed, and in “special situation” outliers where skilled research indicates special upcoming price gain opportunity. But there are hundreds of stocks and some ETFs in our forecastable population that are not in that set. Since equity RIs are creatures of their participating audiences, some stocks have much more widely ranging RI travels, and many are more stable. The Market Profile of Figure 1 does not indicate which is which, but in periods like now, the less stable ones sort themselves out swinging from one side of the distribution to the other. This day’s Profile has an average RI of 24, suggesting three times as much upside price change prospect as downside. (100-24=76, 76 / 24 = 3) Yet The largest, most liquid security being traded, the SPDR S&P 500 Trust ETF (NYSEARCA: SPY ), has a Range Index of 34. That implies only twice as much upside as downside (100-34=66, 66 /34 ~ = 2). To the extent that individual investors influence the overall market, we now seem to be where their influence is intent of fearfully selling items of value to professional, more opportunistic, investors. After the market has remained more irrational than individual investors’ fear or holdings can last, we will forget about what the media speculates that the Fed can do to us all, and the equity markets will return to their usual uptrending character. But in the opportunity interim… There are a lot of price-gain prospects yelling for attention. They are most evident among the leveraged long ETFs, where their capital structures are designed to magnify the price movements of the indexes or stock holdings that they track. The market character of the 20 such ETFs with the greatest likely appeal for active wealth-building investors is shown in Figure 2. These dry details are important, because they easily (and often) get overlooked in the race to capture profit opportunities. Sometimes that may cripple the intent. Ice cream in your lap is never as satisfying as ice cream in the lap’s interior, so napkins (perspective) have a protective purpose. Figure 2 (click to enlarge) source: Yahoo Finance The biggest bets among leveraged long ETFs currently are in US priced WTI crude oil, via ProShares Ultra Bloomberg Crude Oil ETF (NYSEARCA: UCO ), where 7 million shares with a market value of over $1 billion is involved. Close behind are three broad market index tracking ETFs, the ProShares UltraPro S&P 500 ETF (NYSEARCA: UPRO ), the Direxion Russell 2000 Bullish 3X ETF (NYSEARCA: TNA ), and the P roShares UltraPro QQQ ETF (NASDAQ: TQQQ ). In the same just-under-a-billion league is the Proshares Ultra Nasdaq Biotechnology ETF (NASDAQ: BIB ). Combined they make up a tiny fraction of the largest (unleveraged) ETF, the SPDR S&P 500 ETF Trust, where $167 billion is committed. The average daily trading volume in each of those just named is sufficient to completely turn over their capital investments made in them in 1 to 2 weeks. These are very liquid securities most of which tend to be held rather briefly. Their cost of entry and exit, the bid-ask spread, is totally trivial, 1/10th of 1%, or less than -0.2% per round-trip. The way to make them productive is to know when to own them, and when not to. They have been constructed and contain holdings designed to accentuate the price movements in the indexes that they track. That can be seen in their price movements over the past 52 weeks. For example, SPY has had a price range of 18%, going from $181.92 to 213.78, as the S&P 500 Index that it tracks moved from 1820.66 to 2134.72 (prices ten times as large, but the same percentage change). In contrast, UPRO and the Direxion Daily S&P 500 Bull 3X Shares ETF ( SPXL) are constructed to move 3 times as much. Over the same time period that the S&P 500 moved 18%, they moved 71% and 61%, as expected. All of these ETFs are set up with operating leverage (not financial leverage by borrowing) to move either double or triple the change in their underlier indexes. The owner of the security is never subject to a margin call, which is important, because a -20% decline in what is being tracked becomes a -60% decline in the ETF. Leverage cuts both ways. The decision to exit from one of these securities is always a choice by the owner, it is never forced him/her by a broker or lender, as long as they are not part of securities pledged for some separate loan. When measured from the ETF’s low 52-week price to its high, the average price change for their best-possible trips in the period is 147%. But direction is important. Those ranges are a mix of crude oil’s UCO declining from $162 to $17, and biotech stocks’ BIB rising from $42 to $106. Which critter to ride, American Pharaoh or that rodeo Brahma bucking bull? Most of these ETFs in a year will see their prices have both increases and decreases within their extremes, sometimes repeatedly. With such wide ranges, it pays to know what is likely to be coming. A start on that perspective can be had by anyone from the past price range data made public information by the exchanges and clearing houses. A past Range Index [RI] calculation can be done by comparing that part of the range between the low and the current market quote with the whole range from low to high. The Range Index lets the investor compare where each ETF now is in its range from zero to 100. If past-year ranges were to be repeated, a low RI would indicate a lot of upside, while a high RI signals much downside exposure. But are past price ranges to be repeated? We don’t know. That is why we turn to the market-making community, who make an extremely nice living out of having better guesses about that than almost everyone else. Part of that community takes on the job of insurance underwriter, for prices they deem necessary, of providing risk protection for the other part of the MM community that has to put part of its capital at risk making it possible for fund-management clients to adjust their holdings. That happens because the fund clients have to make securities transactions larger than the markets are normally prepared to find participants for the other side of the trade. Both the block trade desks of the MM firms (buyers of risk protection) and the proprietary trading desks of MM firms (sellers of protection) keep themselves extremely well informed via world-wide information gathering systems on a 24×7 basis so that they can’t get raped by their clients. So the price paid for the protection seen as needed is a fair fight, viewed from both sides, and is agreed to by all three parties involved, since the fund client winds up paying for it as part of the cost of the desired trade. This is significant, since its cost, and the way the deal is structured, tells just how far they all believe the security’s price might possibly go while the insurance is in force. The insurance is provided by a hedging transaction that uses derivative securities (futures, options, and swaps) that are based on contracts that have expirations in coming weeks and months. Unwinding the hedge may not be as quick and easy as coming market changes removing the need for it. So the price ranges implied by the hedge deal’s contracts are not simply matters of the moment, but involve considerations of things to come. Our decades-long experience shows that what they imply has profitable forecasting content. Figure 3 shows the current price range forecasts for these leveraged-long ETFs, and averages of forecasts for a population of over 2500 widely-held and actively traded stocks and ETFs. Figure 3 (click to enlarge) source: Peter Way Associates, blockdesk.com. Columns (2) and (3) are MM forecasts of (4). The remaining columns are the result of using prior forecasts with upside-to-downside proportions (7) like those of today. Column (12) tells, out of the past 5 years of daily forecasts how many of those there have been. A simple portfolio risk-management discipline has been applied to each hypothetical buy position, assuming a next-day market close price cost. That discipline uses (2) as a first-occurrence (at or above) sell target within the next 3 months (63 market days). If not yet achieved, position closeout is forced then regardless of loss or gain, and the liberated capital is immediately redeployed. Column (9) tells the net gain or loss from the (12) sample thus managed, (10) the average period held (in market days) and (11) the CAGR of those results. (6) indicates the average worst-case price drawdown on the way to (9), and (8) the proportion of the sample recovering from (6) to produce a profit. The quality of forecasts is tested in (13) by pitting (9) against (5) and in (14) by comparing (6) against (5). (5) is a calculation of (2) and (4). A figure of merit [FOM] is produced in (15) by weighting (9) by (8) and (6) by the complement of (8), weighted by the frequency of (12). The items in Figures 2 and 3 are ranked by (15). Please note that all forecasts are made live, before the fact, and only judged in Figure 3 afterwards. What is involved here is not a “back-test” of some current-day hypothesis, but an accounting of the results of applying an investment strategy evolved in years previous, to forecast data made as time subsequently progressed. These all are live-tests. Comparing leveraged-long ETF prospects now The blue summary rows provide perspective of how well the MM community appraises these ETFs in comparison to how well they see other equity investments. Over 2500 equities have an average f orecast Range Index of 25, like what is indicated in Figure 1, with three times as much upside prospect (+15%) as downside. Their actual downside exposures during the past 5 years have averaged ~ -9%, and only 60% of them have recovered sufficiently to produce profitable closeouts. That resulted in an achieved net gain of only +3%, not today’s prospect of +15%. A terrible credible ratio of 0.2. These best-20 ranked ETFs bettered the upside expectations a bit, and overcame comparable drawdown experiences in 7 out of 8 cases to generate gains approaching +13%. A much more credible ratio of 0.8. And it took only 32 market days (6+ weeks) instead of the population’s 46 days (9 weeks). The CAGR of the ETFs is 8 times as large as the population’s, and 9 times the size of the SPY market proxy’s. SPY has had a much less stressful drawdown risk exposure (-3.6%) but at an enormous reward cost. Comparing the ETF group’s 20 top-ranked items to the best of the population sees about the same net payoffs +12.7 to +12.5% with the best-odds equities winning in 9 out of 10 cases. Their slightly longer holding period (by about a week) cut their CAGR back to a +126% rate, compared to the ETFs’ +156%. On a reward-to-risk tradeoff basis, Figure 4 makes an interesting comparison of these ETFs vs. SPY and the unleveraged Dow-Jones ETF, DIA. Figure 4 (used with permission) This tradeoff map sometimes is helpful in encouraging investors to sort out their own emotional preferences between investment candidates, absent of detailed numerics. Conclusions From Figure 1: Market professionals and major-scale investment fund organizations do not view the near future of coming market prices with anything like the calamity being often expressed by many market observers. From Figure 2: Leveraged-long ETFs are practical and effective near-term investment devices providing ease of entry and exit market liquidity at trivial cost. From Figure 3: As a group, Leveraged Long ETFs currently are competitive with top individual corporate stocks on both a reward~risk tradeoff and on a prospective return basis. Crude Oil and Energy are the currently most attractive ETFs. From Figure 4: Passive investing in broad market-tracking indexes at this point in time in order to avoid downside price change exposure pays an enormous price in terms of denied prospective price gains from active investment in the best Leveraged Long ETFs. Overall: Passive investing perpetually self-inflicts the wounds of time passage in vehicles as they retreat from periods of above average price gains. The current publicly proclaimed fears of overall equity market retrenchment is not being supported by the actions of big investment organizations or the best-informed market professionals that serve them. The continuing fear of continuing price drawdowns in the face of contrary profit-making actions by market-movers denies prospective price change gains during the time that real warnings are not forthcoming. This is the continuing penalty that has been paid by passive investors since the turn of the Y2K century. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.