¡Viva España!

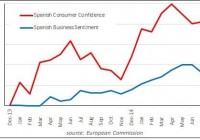

After getting off to a roaring start at the beginning of the year, Spanish equities hit a wall in May. A variety of factors affected them: a spike in interest rates, political upheaval and concern about “contagion” from Greece, as well as some renewed concern about some unchanging issues. Spanish stocks will have to climb a wall of worry, but conditions suggest that they could. Spain ought to outperform the rest of the Eurozone on a twelve-month view. The Spanish economy has grown steadily since Q2 2011, at an accelerating pace, and is on track to grow 3.2% this year, helped by an increase in tourism ─ the strong Pound, a wet summer and travelers’ difficulties with Greece’s cash-only economy boosted Spanish H1 tourist receipts by 7.4%. But tourism is not the only driver of Spain’s recovery, which is broadly-based, and is even beginning to be felt (tentatively) in construction. As this chart implies, growth has been driven by consumption rather than investment or exports, although both of the latter have been healthy. Spanish economic reforms have made the economy considerably more resilient than it was in the darkest days of the Euro Crisis, but there is still much more to be done, so Spaniards could not witness Greek developments with equanimity. The Spanish 10-year bond yield, which had fallen pretty steadily since July 2012, climbed from 1.15% in mid-March to 2.41% in mid-June on fears of “contagion.” It is currently 2.07%. Like consumer confidence, Spanish equities, which had been performing very strongly since the beginning of the year, reacted badly as well: While equities have recovered from the depth of the market’s fears on July 7 (the Tuesday before the crucial Greek parliamentary vote), they do not seem to have recovered their former brio . Several things that are worrying Spanish investors are not new ─ in fact they are perennials. However, Spain’s recent history has brought them once more very much to the fore. One is the structural defects of its labor market. It is indicative that something is very wrong that the Q2 report of 22.4% unemployment, years since the economic crisis, represents improvement. You have to go back to the 1970s to see a reading of less than 5%: even during the boom years it failed to breech 8%. The job creation that has brought it down from 26.9% in Q1 2013 has mostly involved temporary or rolling contract positions. The job protections created by early post-Franco governments are dying, but far too slowly to be helpful to the unemployed. In the meantime, unionized employers that cannot circumvent them simply do not hire, and their workforce just ages. Youth unemployment, while down from its peak, is a still-staggering 49.2%. Persistent unemployment has led to disaffection, amply illustrated by the defeat of traditional parties of government in May’s municipal elections. A significant victor was the Podemos (“We Can”) party, which advocates repudiating the national debt, etc ., but numerous new groups and special interests (civil servants, people who want mortgage forgiveness) won seats. Those who were happy to use their municipal votes for protest might hesitate to elect such groups to parliament; further, the treatment of Greece may cause Spaniards to reconsider support for them. But a national election must be held by December 20th, and it is doubtful whether the economic benefits that current government policy will continue to generate in the meantime will be so dramatic as to change many minds. Thoughtful citizens cannot help but be alarmed. Another perennial worry is separatism. Catalan independence is traditionally a leftist cause, but unlike the Scots, its advocates do not aspire to build Socialism on someone else’s dime. Catalonia is comparatively wealthy, with industrial traditions that are still intact rather than sentimental memories: it could probably be a viable state. Discontent that finds expression elsewhere as “Occupy”-type anarcho-populism, channels easily into separatism in Catalonia. Last November’s referendum saw 80.8% support for independence. Although there were reservations about the value of this exercise ─ some estimated turnout as low as a third, despite minors’ and non-citizens’ participation ─ it certainly does not suggest that support for Catalan independence has dimmed. There are also concerns about deflation. These have hovered over the entire Eurozone, but Spanish prices have contracted by a rather disturbing 6.2% over the last year: It is not surprising that business sentiment, as shown in the first chart, is lagging so noticeably behind consumer confidence. All of which amounts to quite a wall of worry for Spanish equities to surmount. However, if construction is in fact recovering, that will do much to cut into unemployment, as will continued strength in tourism. Both would help youth employment. Greece’s failure to persuade other Europeans to continue to prop up its grotesque economic policies must surely have discredited the more wild-eyed notions of how to escape austerity. Catalan independence will probably overshadow Spain indefinitely: last year’s poll indicates that the flame still burns, but it was too flawed to suggest that concerted efforts toward secession will materialize soon. While the refusal of Spanish prices to increase remains a concern, there is little evidence that they are still contracting (since January, almost all the reported price decline is due to energy). So the Spanish glass is half full as well as half empty: classic conditions under which equity prices can climb a wall of worry. Will they do so? The chances are pretty good. Interest rates can be expected to return to levels closer to those of March. The European Union’s fudge on Greece is sufficient to push those concerns to the back of many minds. Continued economic gains may not help the current government’s electoral chances much, but they cannot hurt. Friday’s report of June industrial production saw it drop 1.4% drop in Germany, 1.1% in Italy, and 0.1% in France, while gaining 0.4% in Spain, suggesting that the Spanish economy will continue to grow more strongly than those the Eurozone generally. Yet other Eurozone equity markets have not been as lackluster as Spain’s in the last week, improving Spain’s relative value in a context where its economy is clearly outperforming theirs. The fundamental attractions that drove the IBEX Index up 22% from trough to peak during its January to May rally are still in place, and in many cases have improved further. There are three Spain ETFs available in the U.S., but the iShares MSCI Spain Capped ETF (NYSEARCA: EWP ) is the only very usable one. The others, SPDR MSCI Spain Quality Mix ETF (NYSEARCA: QESP ) and iShares Currency Hedged MSCI Spain ETF (NYSEARCA: HEWP ), have AUM of only $2.5 million and $3.8 million respectively, making them essentially illiquid. EWP has AUM of $1.7 billion. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.