EELV Makes The Cut For Consideration, May Be A Good Option For Emerging Market Exposure

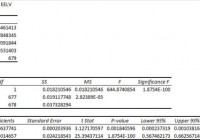

Summary I’m taking a look at EELV as a candidate for inclusion in my ETF portfolio. The expense ratio is a little high relative to my cheap tastes, but certainly within reason. The correlation to SPY is low and based on reasonable trade volumes. Returns since inception have been fairly weak, but the measuring period is less than 3 years. The ETF might fit for my portfolio. I’m not assessing any tax impacts. Investors should check their own situation for tax exposure. Investors should be seeking to improve their risk adjusted returns. I’m a big fan of using ETFs to achieve the risk adjusted returns relative to the portfolios that a normal investor can generate for themselves after trading costs. I’m working on building a new portfolio and I’m going to be analyzing several of the ETFs that I am considering for my personal portfolio. One of the funds that I’m considering is the PowerShares S&P Emerging Markets Low Volatility Portfolio (NYSEARCA: EELV ). I’ll be performing a substantial portion of my analysis along the lines of modern portfolio theory, so my goal is to find ways to minimize costs while achieving diversification to reduce my risk level. What does EELV do? EELV attempts to track the total return (before fees and expenses) of the S&P BMI Emerging Markets Low Volatility Index. At least 90% of the assets are invested in funds included in this index. EELV falls under the category of “Diversified Emerging Markets”. Does EELV provide diversification benefits to a portfolio? Each investor may hold a different portfolio, but I use SPY as the basis for my analysis. I believe SPY, or another large cap U.S. fund with similar properties, represents the reasonable first step for many investors designing an ETF portfolio. Therefore, I start my diversification analysis by seeing how it works with SPY. I start with an ANOVA table: (click to enlarge) The correlation is excellent at 70%. I want to see low correlations on my international investments. Extremely low levels of correlation are wonderful for establishing a more stable portfolio. I consider anything under 50% to be extremely low. However, for equity securities an extremely low correlation is frequently only found when there are substantial issues with trading volumes that may distort the statistics. Standard deviation of daily returns (dividend adjusted, measured since April 2012) The standard deviation is a bit high. For EELV it is .8427%. For SPY, it is 0.7420% for the same period. SPY usually beats other ETFs in this regard, so I’m not too concerned about this. Because the ETF has fairly low correlation for equity investments and an acceptable standard deviation of returns, it should do fairly well under modern portfolio theory. Liquidity looks fine Average trading volume isn’t very high, just shy of 60,000, but that isn’t low enough to be a major concern for me. Mixing it with SPY I also run comparisons on the standard deviation of daily returns for the portfolio assuming that the portfolio is combined with the S&P 500. For research, I assume daily rebalancing because it dramatically simplifies the math. With a 50/50 weighting in a portfolio holding only SPY and EELV, the standard deviation of daily returns across the entire portfolio is 0.7304%. With 80% in SPY and 20% in EELV, the standard deviation of the portfolio would have been .7215%. If an investor wanted to use EELV as a supplement to their portfolio, the standard deviation across the portfolio with 95% in SPY and 5% in EELV would have been .7349%. I know it may seem weird that the standard deviation is lowest at the middle level of including EELV, but that is normal for an asset with low correlation but higher standard deviation. Why I use standard deviation of daily returns I don’t believe historical returns have predictive power for future returns, but I do believe historical values for standard deviations of returns relative to other ETFs have some predictive power on future risks and correlations. Yield & Taxes The distribution yield is 2.68%. That appears to be a respectable yield. This ETF could be worth considering for retiring investors. I like to see strong yields for retiring portfolios because I don’t want to touch the principal. By investing in ETFs I’m removing some of the human emotions, such as panic. Higher yields imply lower growth rates (without reinvestment) over the long term, but that is an acceptable trade off in my opinion. I’m not a CPA or CFP, so I’m not assessing any tax impacts. Expense Ratio The ETF is posting .45% for a gross expense ratio, and .29% for a net expense ratio. I want diversification, I want stability, and I don’t want to pay for them. The expense ratio on this fund is higher than I want to pay for equity securities, but not high enough to make me eliminate it from consideration. I view expense ratios as a very important part of the long-term return picture because I want to hold the ETF for a time period measured in decades. Market to NAV The ETF is at a -.47% discount to NAV currently. Premiums or discounts to NAV can change very quickly so investors should check prior to putting in an order. The ETF is large enough and liquid enough that I would expect the ETF to stay fairly close to NAV. Generally, I don’t trust deviations from NAV. If I can buy an ETF at a discount to NAV, I consider that to be a favorable entry price. Largest Holdings The diversification is very good in this ETF. If I’m going to be stuck with that expense ratio, I expect it to buy a fairly strong level of diversification. This ETF is providing a good level of diversification to give some justification to the expense ratio. (click to enlarge) Conclusion I’m currently screening a large volume of ETFs for my own portfolio. The portfolio I’m building is through Schwab, so I’m able to trade EELV with no commissions. I have a strong preference for researching ETFs that are free to trade in my account, so most of my research will be on ETFs that fall under the “ETF OneSource” program. The correlation and diversification are great. The discount to NAV is also very appealing, but those discounts can disappear quickly. The net expense ratio isn’t too bad, though the gross expense ratio is less attractive. I might dig into the difference if I was considering a large position to determine how sustainable it would be. Since the ETF is covering emerging markets, I wouldn’t want to go more than 10% into the ETF because of the risks that I believe are present there. On the other hand, we saw that the portfolio had a lower standard deviation when this ETF was 20% of the portfolio rather than 5% because of the low correlation. I’ll need to test EELV in hypothetical portfolios that are more diversified to see how it does there. I think this one is worth considering for the 5% to 10% exposure to emerging markets. Additional disclosure: Information in this article represents the opinion of the analyst. All statements are represented as opinions, rather than facts, and should not be construed as advice to buy or sell a security. Ratings of “outperform” and “underperform” reflect the analyst’s estimation of a divergence between the market value for a security and the price that would be appropriate given the potential for risks and returns relative to other securities. The analyst does not know your particular objectives for returns or constraints upon investing. All investors are encouraged to do their own research before making any investment decision. Information is regularly obtained from Yahoo Finance, Google Finance, and SEC Database. If Yahoo, Google, or the SEC database contained faulty or old information it could be incorporated into my analysis. The analyst holds a diversified portfolio including mutual funds or index funds which may include a small long exposure to the stock.