GTAA Is For Real (Part 3): Why VBINX Is The Wrong Benchmark

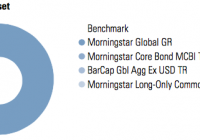

To judge a strategy, it is critically important to identify an appropriate benchmark. For several reasons, comparing tactical strategies to “balanced portfolios” like VBINX is inappropriate. The Global Market Portfolio meets all the criteria for a proper benchmark, making it is the most appropriate baseline for assessing GTAA strategies. At our research blog, we recently posted an article discussing how many noteworthy investment commentators either misunderstand or misconstrue the salient qualities of Tactical Asset Allocation strategies. We encourage you to read the entire piece, but today’s post will be limited to the topic of benchmarking. One of the most common failings of the investment industry is the prevalence of poorly specified benchmarks. This is of critical importance because it’s easy for a knowledgeable but disingenuous professional to manipulate the facts in order to make any point they want. Want a simple way to boost results? Choose an easy benchmark for comparison. Want to dismiss performance? Choose a challenging benchmark. Recall that at root, a well specified benchmark should meet the following criteria: It is passive; It is investible, and; It reflects the investing opportunity set of the manager. While all of these criteria are individually valid, they are unified by a simple and profound benchmarking philosophy: The best benchmark for a tactical manager is the one they would own if everyone were forced to invest all their assets in a single, passive portfolio. Axiomatically, this portfolio would represent the average positions of all market participants, and would hold each asset in a percentage equal to its proportion of total market capitalization. This is not a new concept; U.S. large cap equity managers are typically benchmarked against a market cap weighted index of large-cap U.S. stocks. U.S. Investment Grade bond managers are benchmarked against a market cap weighted index of U.S. listed investment grade bonds. Cap weighted indexes are common and intuitive when they are constructed within a major asset class. But it is not immediately intuitive how to extend the concept to multi-asset universes like those employed by GTAA managers. As a result, GTAA strategy benchmarks often seriously misrepresent the risks and opportunities of the underlying strategies. Investment commentators who dismiss TAA often compare the results of GTAA strategies to a U.S. 60/40 balanced fund like the Vanguard Balanced Index Fund (MUTF: VBINX ). And this benchmark does have one thing going for it, especially if a commentator’s goal is to malign GTAA strategies: it is a very tough benchmark to beat over the past one, three and five years – perhaps the toughest in the world in USD terms. Unfortunately, it’s hard to see how this portfolio represents an appropriate bogey for GTAA strategies over the long-term. For one, this portfolio is insulated from global currency effects, which have been especially pronounced in the past few years with global QE programs in effect. Second, it ignores non-U.S. equity beta; while a focus on U.S. equities at the expense of international stocks has been a lucky bet for the past few years, it ignores the broader scope of GTAA strategies. Also, since the goal of GTAA strategies is to harvest premia from as many liquid global sources as possible, the strategies often incorporate alternative investments, like REIT and commodity ETFs, into their investible universe. These are not represented in a U.S. balanced fund benchmark. Fortunately, some analysts take a more enlightened view. In their quarterly ” ETF Managed Portfolios Landscape Summary ” report, Morningstar proposes a much more globally diversified benchmark. The report’s Global All Asset benchmark, copied below, is composed of 55% global stocks, presumably distributed geographically by market cap; 35% global bonds, split evenly between U.S. and international; and 10% commodities. Source: Morningstar Clearly the folks at Morningstar are trying to be more representative of the GTAA space, and their mix is certainly in the right ballpark. But it is also still rather arbitrary – how did they arrive at their weights? Have they weighted toward historical GTAA holdings? If so, is there any guarantee that historical holdings will be representative of future holdings? These are dynamic strategies after all. Do commodities deserve a 10% strategic weighting or is this informed by recency bias? In addition, the Morningstar benchmark is over 80% weighted to U.S. dollars. Does this represent a neutral currency policy? We stated above that it isn’t immediately obvious how to extend the market cap weighted benchmarks applied to traditional single-asset portfolios, such as equity or bond funds, to a multi-asset context. This isn’t strictly true. In a multi-asset situation, we would expect a passive portfolio to hold all asset classes in proportion to their respective market capitalizations. Consider a simple example where the aggregate global market has a value of $100 trillion, where $50 trillion is stocks and $50 trillion is bonds. In this case, a passive investor would hold 50% of their portfolio in bonds and 50% in stocks. Every participant in the markets could hold this exact portfolio without changing the overall composition of the market, so it is the only passive, neutral portfolio. As discussed in prior posts (see here and here ) Doeswijk et. al. determined the actual market value of every global financial asset (as of year-end 2012) and published their relative market capitalization weights in a 2014 paper. These weights describe the most passive global portfolio possible: the global market cap weighted portfolio (GMP). This portfolio reflects the average portfolio positions of all investors globally. Fortunately, an investible version of this portfolio can be very closely replicated with low-cost, U.S. listed ETFs (see Figure 5.) This portfolio uniquely meets all the criteria for an appropriate benchmark: it is definitionally the only passive portfolio; it is definitionally investible; and it covers the investible opportunity set for GTAA mandates because it includes all global investible assets. Figure 5. Investible Global Market Portfolio. (click to enlarge) Source: Interpreted from Doeswijk et. al. We would note that the global market cap weighted portfolio definitionally holds all assets in their native currency, and therefore reflects currency fluctuations in non-domestic asset classes. Over 50% of both global equity and bond sleeves in our proposed global market portfolio is impacted by non-U.S. currency exposure (the foreign equity exposure is hidden inside our global equity ETF). We believe this is the most appropriate benchmark for GTAA strategies. In the next and final chapter of our series on GTAA, we will examine the performance of a robust cross-section of live strategies, and show how GTAA strategies have delivered measurable alpha against well specified benchmarks, even over this most difficult phase of the market cycle. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.