Scalper1 News

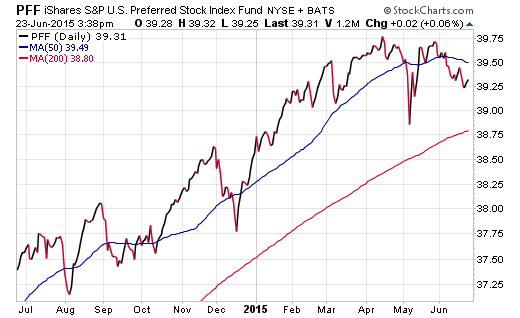

Summary The income investing landscape has certainly shifted in 2015, with many dividend fixtures trading well below their starting point for the year. The backup in interest rates this year has been the primary culprit responsible for rebalancing the scale away from these equity income assets. PFF has managed to remain on a relatively steady course so far this year when compared to other areas of the income-generating universe. The income investing landscape has certainly shifted in 2015, with many dividend fixtures trading well below their starting point for the year. Stalwart asset classes such as REITs, utilities, MLPs, and even dividend paying common stocks have struggled to make positive headway and in some cases are more than 10% off their recent highs. The backup in interest rates this year has been the primary culprit responsible for rebalancing the scale away from these equity income assets. The 10-Year Treasury Note Yield has moved over 40% higher since hitting a low in January and is now firmly situated near 2.40%. Income investors are likely feeling a level of frustration with the lack of progress year-to-date and oversensitivity to interest rates may fuel additional anxiety as they contemplate the looming threat of a Fed rate hike. Nevertheless, one alternative asset class has continued to persevere despite the overarching malaise. The iShares U.S. Preferred Stock ETF (NYSEARCA: PFF ) is a fund I have owned for some time now for my income-seeking clients . PFF has over $13 billion dedicated to over 300 preferred stock holdings and charges an expense ratio of 0.47%. One of the most attractive features of this fund is its current 30-day SEC yield of 5.40%. Income is paid on a monthly basis to shareholders and has historically been very consistent. In addition, PFF has managed to remain on a relatively steady course so far this year when compared to other areas of the income-generating universe. Preferred stocks carry characteristics of both equity and debt, which allow for very low correlations with either asset class. Typically these securities are issued by banks, financial institutions, and real estate companies with long maturity dates. While PFF has been able to escape the wrath of interest rate volatility this year, that doesn’t mean it will hold up under every appreciable change in credit or Treasury-linked securities. This fund experienced a 10% drop in 2013 as changes to quantitative easing programs by the Fed sent shockwaves through the financial markets. The portfolio manager for PFF did an excellent review of its potential weaknesses with respect to interest rates that is worth a read as well. Another ETF in this space that promises a unique dynamic is the PowerShares Variable Rate Preferred Portfolio ETF (NYSEARCA: VRP ). This fund primarily invests in preferred stocks with floating rate or variable coupon components. VRP has an effective duration of 3.86 years and a 30-day SEC yield of 4.92%. In theory, floating rate securities are deemed to be more effecting during periods of rising interest rates because their income component adjusts higher along the way and they typically have shorter durations. Nevertheless, with the relatively short trading history, this strategy has yet to be tested under the rigors of an outsized move in rates. The Bottom Line Preferred stock ETFs can be used for yield enhancement and diversification in the context of a well-balanced income portfolio. However, investors should be aware that as a non-traditional asset class, they may be susceptible to unique risks and price drivers. Keep in mind that the higher yields of preferred stocks should correlate with smaller overall position sizes to avoid becoming overly focused on just one component of these securities. Disclosure: I am/we are long PFF. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. Additional disclosure: David Fabian, FMD Capital Management, and/or clients may hold positions in the ETFs and mutual funds mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell, or hold securities. Scalper1 News

Summary The income investing landscape has certainly shifted in 2015, with many dividend fixtures trading well below their starting point for the year. The backup in interest rates this year has been the primary culprit responsible for rebalancing the scale away from these equity income assets. PFF has managed to remain on a relatively steady course so far this year when compared to other areas of the income-generating universe. The income investing landscape has certainly shifted in 2015, with many dividend fixtures trading well below their starting point for the year. Stalwart asset classes such as REITs, utilities, MLPs, and even dividend paying common stocks have struggled to make positive headway and in some cases are more than 10% off their recent highs. The backup in interest rates this year has been the primary culprit responsible for rebalancing the scale away from these equity income assets. The 10-Year Treasury Note Yield has moved over 40% higher since hitting a low in January and is now firmly situated near 2.40%. Income investors are likely feeling a level of frustration with the lack of progress year-to-date and oversensitivity to interest rates may fuel additional anxiety as they contemplate the looming threat of a Fed rate hike. Nevertheless, one alternative asset class has continued to persevere despite the overarching malaise. The iShares U.S. Preferred Stock ETF (NYSEARCA: PFF ) is a fund I have owned for some time now for my income-seeking clients . PFF has over $13 billion dedicated to over 300 preferred stock holdings and charges an expense ratio of 0.47%. One of the most attractive features of this fund is its current 30-day SEC yield of 5.40%. Income is paid on a monthly basis to shareholders and has historically been very consistent. In addition, PFF has managed to remain on a relatively steady course so far this year when compared to other areas of the income-generating universe. Preferred stocks carry characteristics of both equity and debt, which allow for very low correlations with either asset class. Typically these securities are issued by banks, financial institutions, and real estate companies with long maturity dates. While PFF has been able to escape the wrath of interest rate volatility this year, that doesn’t mean it will hold up under every appreciable change in credit or Treasury-linked securities. This fund experienced a 10% drop in 2013 as changes to quantitative easing programs by the Fed sent shockwaves through the financial markets. The portfolio manager for PFF did an excellent review of its potential weaknesses with respect to interest rates that is worth a read as well. Another ETF in this space that promises a unique dynamic is the PowerShares Variable Rate Preferred Portfolio ETF (NYSEARCA: VRP ). This fund primarily invests in preferred stocks with floating rate or variable coupon components. VRP has an effective duration of 3.86 years and a 30-day SEC yield of 4.92%. In theory, floating rate securities are deemed to be more effecting during periods of rising interest rates because their income component adjusts higher along the way and they typically have shorter durations. Nevertheless, with the relatively short trading history, this strategy has yet to be tested under the rigors of an outsized move in rates. The Bottom Line Preferred stock ETFs can be used for yield enhancement and diversification in the context of a well-balanced income portfolio. However, investors should be aware that as a non-traditional asset class, they may be susceptible to unique risks and price drivers. Keep in mind that the higher yields of preferred stocks should correlate with smaller overall position sizes to avoid becoming overly focused on just one component of these securities. Disclosure: I am/we are long PFF. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. Additional disclosure: David Fabian, FMD Capital Management, and/or clients may hold positions in the ETFs and mutual funds mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell, or hold securities. Scalper1 News

Scalper1 News