Scalper1 News

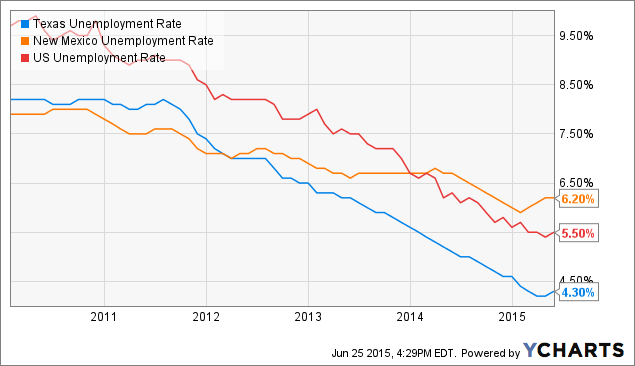

Summary Electric utility holding company PNM Resources has underperformed the S&P 500 in 2015 YTD due to regulatory and economic headwinds. While regulatory uncertainty is negatively impacting the company’s FY 2016 earnings estimates, its history of earnings and dividend growth provide some optimism. At the same time, however, its earning growth could be adversely affected by a slowing Texas economy and reduced energy demand in New Mexico. Potential investors should not consider initiating a long position until the company’s shares hit a 3-year forward P/E ratio low, or $21.40 based on the consensus FY 2016 EPS estimate. PNM Resources (NYSE: PNM ) is an investor-owned holding company that provides electricity to customers in New Mexico and Texas through two subsidiary utilities, PNM (in New Mexico) and TNMP (in Texas). The company’s share price grew strongly in the second half of 2014 as energy prices fell across the board but has subsequently lost almost of that ground in 2015, having fallen by almost 21% YTD (see figure). While the company’s trailing earnings have increased even as its share price has retreated, the presence of regulatory uncertainty and underwhelming electricity demand in New Mexico have weighed on investors’ minds. This article evaluates PNM Resources as a potential long investment in light of the current operating conditions. PNM data by YCharts PNM Resources at a glance The two utility subsidiaries of PNM Resources operate in different areas of the electric utilities sector. PNM (the subsidiary rather than the holding company) is a vertically integrated regulated electric utility that generates, transmits, and distributes electricity to 513,000 residential and commercial customers across New Mexico, including Greater Albuquerque. It owns and operates 2,707 MW of generating capacity and 14,800 miles of transmission lines. PNM also owned a gas utility until 2009, at which point it was sold to a competitor in New Mexico to allow the subsidiary to focus entirely on electricity generation and distribution. PNM has undergone the beginning of a transition toward lower-carbon energy sources in recent years in an effort to reduce its overall carbon footprint. This transition will involve the closure of two of PNM’s existing coal-fired generating units by 2017, a move that will reduce its total capacity by 847 MW while also bringing its greenhouse gas emissions 17% below their 2005 levels. PNM is also investing in the generation and purchase of renewable electricity, including the construction of 107 MW of utility solar capacity by 2016 for $269 million, the purchase of 102 MW of wind energy from the Red Mesa Wind Energy Center, and 10 MW of geothermal energy. One of the most notable investments is the PNM Prosperity Energy Storage Project , which is the first solar electricity storage facility to be fully integrated into the utility power grid. The project provides 500 kW of solar energy capacity and 1 MWh of electricity storage capacity. While the announcement of the Tesla Powerwall has sparked a debate into the current value of electricity storage, the placement of PNM’s project ensures that it will have the greatest feasibility available in terms of solar availability. PNM has not completely abandoned coal, however, having recently signed a coal supply agreement through 2022 with miner Westmoreland Coal (NASDAQ: WLB ) that will generate cost savings for the utility of up to 20%. TNMP is a regulated electricity transmission and distribution utility that provides electric service to customers in Texas. The electric utility in Texas is different from those in many other states in that it is unregulated at the point of generation but regulated for purposes of transmission and distribution. TNMP is regulated, therefore, but under the Texas Electric Rate program it distributes electricity to customers from competing retail electricity generators. TNMP serves 240,000 customers, including coastal petroleum facilities, via approximately 9,000 miles of transmission and distribution lines. PNM Resources has maintained relatively heavy exposure to New Mexico over the past several years, with PNM generating a greater share of the holding company’s earnings than TNMP. This has hurt its revenue of late due to weak electricity demand, the result of a combination of a weak economy and unfavorable weather conditions. The company’s revenue in FY 2014 was 16% lower than in FY 2010. Thanks to the combination of low energy prices following the widespread advent of shale gas extraction, which caused natural gas and coal prices to move sharply lower, and cost-control measures, the company has been able to maintain its gross income and operating income (see table). PNM Resources Financials (non-adjusted) Q1 2015 Q4 2014 Q3 2014 Q2 2014 Q1 2014 Revenue ($MM) 332.9 346.9 414.0 346.2 328.9 Gross income ($MM) 174.6 163.9 221.3 174.8 169.0 Net income ($MM) 14.3 19.0 55.7 29.1 12.5 Diluted EPS ($) 0.18 0.24 0.69 0.36 0.16 EBITDA ($MM) 111.7 120.7 174.9 130.5 104.0 Source: Morningstar (2015). PNM Resources has also been able to maintain a solid, if not exceptionally strong, balance sheet over the last several quarters (see table). Its current ratio has remained stable even as it has returned $50-60 million in cash dividends, which have in turn grown by approximately 12% annually per share, to shareholders. The most recent such increase came last December, bringing the quarterly dividend up to $0.20 per share. While the company’s cash reserves have generally been low, this is not uncommon for regulated utilities due to their access to large lines of credit at relatively low interest rates. PNM Resources Balance Sheet (restated) Q1 2015 Q4 2014 Q3 2014 Q2 2014 Q1 2014 Total cash ($MM) 122.4 28.3 28.4 12.1 27.2 Total assets ($MM) 5,939.3 5,829.3 5,709.2 5,604.2 5,507.0 Current liabilities ($MM) 693.0 704.3 700.3 486.9 312.1 Total liabilities ($MM) 4,224.9 4,107.8 3,986.5 3,907.7 3,841.2 Source: Morningstar (2015). Q1 earnings report PNM Resources reported Q1 earnings last month that were largely in-line with expectations. The company reported revenue of $332.9 million, up 1.2% from $328.9 million in Q1 2014 and just missing the consensus estimate by $2.1 million. The company’s loads were down in New Mexico overall (residential loads were higher YoY but commercial and industrial loads were lower), marking at least the ninth consecutive quarter in which such a drop was reported in the state. This was partially offset by higher loads in all categories in Texas, however; the company also reported better-than-expected customer growth in both states as well. The presence of low energy prices and other sources of income in Q1 allowed PNM Resources to report slight operating income growth YoY from $48.8 million to $49.6 million. Net income also increased, from $12.5 million in Q1 2014 to $14.3 million in the most recent quarter, or diluted EPS results of $0.16 and $0.18, respectively. Adjusted net income, which included positive adjustments from mark-to-market impacts of economic hedges and state tax credits, rose from $14.2 million to $16.5 million YoY. Adjusted diluted EPS came in at $0.21 compared to $0.18 the previous year, beating the consensus estimate by $0.03. PNM reported the strongest improvement over the previous year, with its EPS rising from $0.11 to $0.14 as refined coal income, reimbursement for spent nuclear fuel, and half-priced leases more than offset the negative impact of reduce New Mexico loads. TNMP reported a slight EPS increase from $0.09 to $0.10 YoY, with the increase being attributed to slightly higher Texas loads and rate relief. While Q1 is historically a weak quarter for utilities operating in the Southwest U.S., it was strong enough for PNM Resources to maintain its previous guidance for adjusted diluted EPS of $1.50-$1.62 in FY 2015. Outlook PNM Resources faces a mixed operating outlook over the next several quarters. The economies of Texas and New Mexico have undergone very different recoveries in the wake of the Great Recession despite their close proximity. While New Mexico was not especially hard-hit by the recession, with its unemployment rate staying below that of both Texas and the U.S. average initially (see figure), it quickly fell behind after 2012. Texas, on the other hand, saw its unemployment rate plummet beginning the same year as it became a major producer of natural gas and petroleum, and its unemployment rate remains well below those of New Mexico and the U.S. average despite a recent uptick following last year’s energy price collapse. This has allowed PNM Resources to essentially split the difference, although its heavier focus on New Mexico via electricity generation as well as distribution has prevented strength in Texas from completely offsetting New Mexico’s relative weakness in recent quarters. Management stated during the Q1 earnings call that it is seeing early signs of “stabilization” in New Mexico’s economy, with employment rolls increasing and YoY customer growth of 0.7%. This improved outlook is partially offset by weakness in Texas, however, as energy production in that state has fallen in recent months (although customer growth there did increase by 1.4% in Q1 YoY). Potential investors in PNM Resources will want to keep an eye on economic conditions in both states. While energy prices have rebounded of late, sustained low prices for natural gas and petroleum could limit load growth in Texas in particular, hampering the company’s outlook. Texas Unemployment Rate data by YCharts Regulatory uncertainty has increased recently following adverse initial decisions at both the federal and state levels. PNM Resources recently received notice that the compliance plans it had submitted to regulators were determined to be insufficient, raising questions as to the amount and timing of expenses anticipated under them. The first initial decision relates to the company’s BART determination under the Clean Air Act. Whereas the company has proposed to retire two of its coal-fired units and upgrade two more to comply, the BART hearing examiner recommended that the negotiated proposal be rejected. While the recommendation is not final, Moody’s has indicated that an adverse final BART decision would cause it to remove its positive outlook on the company’s debt, potentially resulting in the imposition of higher interest rates. PNM Resources has also encountered difficulties with its future rate case proposal, which a hearing examiner determined was incomplete. As a regulated utility the company’s rates are determined by regulators rather than the market, making the final decision an important one for the company’s earnings. While the hearing examiner’s decision is not final, its finalization by the state regulatory commission would delay the implementation of new rates by several months, negatively impacting the company’s earnings for one or more quarters. The company has already receive approval for transmission rates equaling a 10% ROE so an adverse decision would not negatively impact all of its operations, but it would still cause the company’s FY 2016 estimated earnings to be revised lower. Valuation Analysts have revised their estimates for the company’s earnings FY 2016 earnings lower over the last 90 days in response to slowing economic growth in Texas and the possible delay in the implementation of new rates for the year. While the consensus estimated EPS for FY 2015 has remained flat at $1.56, the consensus for FY 2016 has fallen from $1.85 to $1.65. Both results would reflect a positive trend on an adjusted basis that has been in place since at least FY 2010. That said, based on the company’s share price at the time of writing of $24.74, this earnings growth has not outpaced the company’s share price. The current share price results in a trailing P/E ratio of 16.3x, which is roughly in the middle of the company’s 3-year range (see figure). The forward P/E ratios for FY 2015 and FY 2016 of 15.9x and 15.0x, respectively, are near the bottom of their respective 3-year ranges, although ratios of 13.5x and 13.0x for FY 2015 and FY 2016 would represent true bottoms (as well as a share price of $21.40, or a discount of 14% to the current share price). PNM PE Ratio (NYSE: TTM ) data by YCharts Conclusion PNM Resources has seen its share price fall substantially since the beginning of the year in response to slowing economic growth in its service areas, regulatory uncertainty at both the state and federal levels, and broad bearish sentiment with regard to dividend stocks in light of anticipated interest rate increases by the Federal Reserve. While the company appears to be undervalued on the basis of earnings estimates for FY 2015 and FY 2016, I believe that potential investors in the firm should require an additional discount to the current share price to compensate for the risks of a slowing Texas economy resulting from low energy prices and the prospect of adverse regulatory actions later in the year. I recommend that potential investors wait to initiate a long position until the company’s shares set a new 3-year low on the basis of forward valuations, or a share price of $21.40 based on current EPS estimates. While the company’s reliable earnings and dividend growth and current 3.1% dividend yield are attractive, the prospect of regulatory and economic headwinds should give potential investors pause. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Scalper1 News

Summary Electric utility holding company PNM Resources has underperformed the S&P 500 in 2015 YTD due to regulatory and economic headwinds. While regulatory uncertainty is negatively impacting the company’s FY 2016 earnings estimates, its history of earnings and dividend growth provide some optimism. At the same time, however, its earning growth could be adversely affected by a slowing Texas economy and reduced energy demand in New Mexico. Potential investors should not consider initiating a long position until the company’s shares hit a 3-year forward P/E ratio low, or $21.40 based on the consensus FY 2016 EPS estimate. PNM Resources (NYSE: PNM ) is an investor-owned holding company that provides electricity to customers in New Mexico and Texas through two subsidiary utilities, PNM (in New Mexico) and TNMP (in Texas). The company’s share price grew strongly in the second half of 2014 as energy prices fell across the board but has subsequently lost almost of that ground in 2015, having fallen by almost 21% YTD (see figure). While the company’s trailing earnings have increased even as its share price has retreated, the presence of regulatory uncertainty and underwhelming electricity demand in New Mexico have weighed on investors’ minds. This article evaluates PNM Resources as a potential long investment in light of the current operating conditions. PNM data by YCharts PNM Resources at a glance The two utility subsidiaries of PNM Resources operate in different areas of the electric utilities sector. PNM (the subsidiary rather than the holding company) is a vertically integrated regulated electric utility that generates, transmits, and distributes electricity to 513,000 residential and commercial customers across New Mexico, including Greater Albuquerque. It owns and operates 2,707 MW of generating capacity and 14,800 miles of transmission lines. PNM also owned a gas utility until 2009, at which point it was sold to a competitor in New Mexico to allow the subsidiary to focus entirely on electricity generation and distribution. PNM has undergone the beginning of a transition toward lower-carbon energy sources in recent years in an effort to reduce its overall carbon footprint. This transition will involve the closure of two of PNM’s existing coal-fired generating units by 2017, a move that will reduce its total capacity by 847 MW while also bringing its greenhouse gas emissions 17% below their 2005 levels. PNM is also investing in the generation and purchase of renewable electricity, including the construction of 107 MW of utility solar capacity by 2016 for $269 million, the purchase of 102 MW of wind energy from the Red Mesa Wind Energy Center, and 10 MW of geothermal energy. One of the most notable investments is the PNM Prosperity Energy Storage Project , which is the first solar electricity storage facility to be fully integrated into the utility power grid. The project provides 500 kW of solar energy capacity and 1 MWh of electricity storage capacity. While the announcement of the Tesla Powerwall has sparked a debate into the current value of electricity storage, the placement of PNM’s project ensures that it will have the greatest feasibility available in terms of solar availability. PNM has not completely abandoned coal, however, having recently signed a coal supply agreement through 2022 with miner Westmoreland Coal (NASDAQ: WLB ) that will generate cost savings for the utility of up to 20%. TNMP is a regulated electricity transmission and distribution utility that provides electric service to customers in Texas. The electric utility in Texas is different from those in many other states in that it is unregulated at the point of generation but regulated for purposes of transmission and distribution. TNMP is regulated, therefore, but under the Texas Electric Rate program it distributes electricity to customers from competing retail electricity generators. TNMP serves 240,000 customers, including coastal petroleum facilities, via approximately 9,000 miles of transmission and distribution lines. PNM Resources has maintained relatively heavy exposure to New Mexico over the past several years, with PNM generating a greater share of the holding company’s earnings than TNMP. This has hurt its revenue of late due to weak electricity demand, the result of a combination of a weak economy and unfavorable weather conditions. The company’s revenue in FY 2014 was 16% lower than in FY 2010. Thanks to the combination of low energy prices following the widespread advent of shale gas extraction, which caused natural gas and coal prices to move sharply lower, and cost-control measures, the company has been able to maintain its gross income and operating income (see table). PNM Resources Financials (non-adjusted) Q1 2015 Q4 2014 Q3 2014 Q2 2014 Q1 2014 Revenue ($MM) 332.9 346.9 414.0 346.2 328.9 Gross income ($MM) 174.6 163.9 221.3 174.8 169.0 Net income ($MM) 14.3 19.0 55.7 29.1 12.5 Diluted EPS ($) 0.18 0.24 0.69 0.36 0.16 EBITDA ($MM) 111.7 120.7 174.9 130.5 104.0 Source: Morningstar (2015). PNM Resources has also been able to maintain a solid, if not exceptionally strong, balance sheet over the last several quarters (see table). Its current ratio has remained stable even as it has returned $50-60 million in cash dividends, which have in turn grown by approximately 12% annually per share, to shareholders. The most recent such increase came last December, bringing the quarterly dividend up to $0.20 per share. While the company’s cash reserves have generally been low, this is not uncommon for regulated utilities due to their access to large lines of credit at relatively low interest rates. PNM Resources Balance Sheet (restated) Q1 2015 Q4 2014 Q3 2014 Q2 2014 Q1 2014 Total cash ($MM) 122.4 28.3 28.4 12.1 27.2 Total assets ($MM) 5,939.3 5,829.3 5,709.2 5,604.2 5,507.0 Current liabilities ($MM) 693.0 704.3 700.3 486.9 312.1 Total liabilities ($MM) 4,224.9 4,107.8 3,986.5 3,907.7 3,841.2 Source: Morningstar (2015). Q1 earnings report PNM Resources reported Q1 earnings last month that were largely in-line with expectations. The company reported revenue of $332.9 million, up 1.2% from $328.9 million in Q1 2014 and just missing the consensus estimate by $2.1 million. The company’s loads were down in New Mexico overall (residential loads were higher YoY but commercial and industrial loads were lower), marking at least the ninth consecutive quarter in which such a drop was reported in the state. This was partially offset by higher loads in all categories in Texas, however; the company also reported better-than-expected customer growth in both states as well. The presence of low energy prices and other sources of income in Q1 allowed PNM Resources to report slight operating income growth YoY from $48.8 million to $49.6 million. Net income also increased, from $12.5 million in Q1 2014 to $14.3 million in the most recent quarter, or diluted EPS results of $0.16 and $0.18, respectively. Adjusted net income, which included positive adjustments from mark-to-market impacts of economic hedges and state tax credits, rose from $14.2 million to $16.5 million YoY. Adjusted diluted EPS came in at $0.21 compared to $0.18 the previous year, beating the consensus estimate by $0.03. PNM reported the strongest improvement over the previous year, with its EPS rising from $0.11 to $0.14 as refined coal income, reimbursement for spent nuclear fuel, and half-priced leases more than offset the negative impact of reduce New Mexico loads. TNMP reported a slight EPS increase from $0.09 to $0.10 YoY, with the increase being attributed to slightly higher Texas loads and rate relief. While Q1 is historically a weak quarter for utilities operating in the Southwest U.S., it was strong enough for PNM Resources to maintain its previous guidance for adjusted diluted EPS of $1.50-$1.62 in FY 2015. Outlook PNM Resources faces a mixed operating outlook over the next several quarters. The economies of Texas and New Mexico have undergone very different recoveries in the wake of the Great Recession despite their close proximity. While New Mexico was not especially hard-hit by the recession, with its unemployment rate staying below that of both Texas and the U.S. average initially (see figure), it quickly fell behind after 2012. Texas, on the other hand, saw its unemployment rate plummet beginning the same year as it became a major producer of natural gas and petroleum, and its unemployment rate remains well below those of New Mexico and the U.S. average despite a recent uptick following last year’s energy price collapse. This has allowed PNM Resources to essentially split the difference, although its heavier focus on New Mexico via electricity generation as well as distribution has prevented strength in Texas from completely offsetting New Mexico’s relative weakness in recent quarters. Management stated during the Q1 earnings call that it is seeing early signs of “stabilization” in New Mexico’s economy, with employment rolls increasing and YoY customer growth of 0.7%. This improved outlook is partially offset by weakness in Texas, however, as energy production in that state has fallen in recent months (although customer growth there did increase by 1.4% in Q1 YoY). Potential investors in PNM Resources will want to keep an eye on economic conditions in both states. While energy prices have rebounded of late, sustained low prices for natural gas and petroleum could limit load growth in Texas in particular, hampering the company’s outlook. Texas Unemployment Rate data by YCharts Regulatory uncertainty has increased recently following adverse initial decisions at both the federal and state levels. PNM Resources recently received notice that the compliance plans it had submitted to regulators were determined to be insufficient, raising questions as to the amount and timing of expenses anticipated under them. The first initial decision relates to the company’s BART determination under the Clean Air Act. Whereas the company has proposed to retire two of its coal-fired units and upgrade two more to comply, the BART hearing examiner recommended that the negotiated proposal be rejected. While the recommendation is not final, Moody’s has indicated that an adverse final BART decision would cause it to remove its positive outlook on the company’s debt, potentially resulting in the imposition of higher interest rates. PNM Resources has also encountered difficulties with its future rate case proposal, which a hearing examiner determined was incomplete. As a regulated utility the company’s rates are determined by regulators rather than the market, making the final decision an important one for the company’s earnings. While the hearing examiner’s decision is not final, its finalization by the state regulatory commission would delay the implementation of new rates by several months, negatively impacting the company’s earnings for one or more quarters. The company has already receive approval for transmission rates equaling a 10% ROE so an adverse decision would not negatively impact all of its operations, but it would still cause the company’s FY 2016 estimated earnings to be revised lower. Valuation Analysts have revised their estimates for the company’s earnings FY 2016 earnings lower over the last 90 days in response to slowing economic growth in Texas and the possible delay in the implementation of new rates for the year. While the consensus estimated EPS for FY 2015 has remained flat at $1.56, the consensus for FY 2016 has fallen from $1.85 to $1.65. Both results would reflect a positive trend on an adjusted basis that has been in place since at least FY 2010. That said, based on the company’s share price at the time of writing of $24.74, this earnings growth has not outpaced the company’s share price. The current share price results in a trailing P/E ratio of 16.3x, which is roughly in the middle of the company’s 3-year range (see figure). The forward P/E ratios for FY 2015 and FY 2016 of 15.9x and 15.0x, respectively, are near the bottom of their respective 3-year ranges, although ratios of 13.5x and 13.0x for FY 2015 and FY 2016 would represent true bottoms (as well as a share price of $21.40, or a discount of 14% to the current share price). PNM PE Ratio (NYSE: TTM ) data by YCharts Conclusion PNM Resources has seen its share price fall substantially since the beginning of the year in response to slowing economic growth in its service areas, regulatory uncertainty at both the state and federal levels, and broad bearish sentiment with regard to dividend stocks in light of anticipated interest rate increases by the Federal Reserve. While the company appears to be undervalued on the basis of earnings estimates for FY 2015 and FY 2016, I believe that potential investors in the firm should require an additional discount to the current share price to compensate for the risks of a slowing Texas economy resulting from low energy prices and the prospect of adverse regulatory actions later in the year. I recommend that potential investors wait to initiate a long position until the company’s shares set a new 3-year low on the basis of forward valuations, or a share price of $21.40 based on current EPS estimates. While the company’s reliable earnings and dividend growth and current 3.1% dividend yield are attractive, the prospect of regulatory and economic headwinds should give potential investors pause. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Scalper1 News

Scalper1 News