Scalper1 News

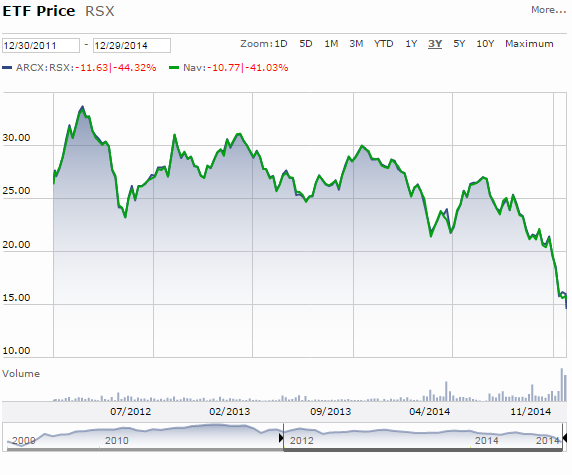

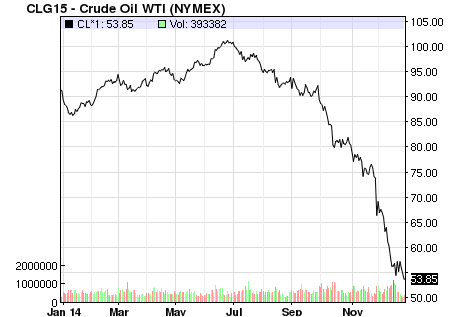

Russian companies may offer the best values in the world currently. Buying assets for pennies on the dollar. An excellent contrarian play is developing. “After an extremely strong performance by U.S. markets this year, it is our belief that emerging markets will be more in focus next year as investors rotate into underperforming areas. Of these markets, Russia, has the lowest fundamental valuation. With new positive light shining on President Vladimir Putin, after having negotiated a peaceful solution to Syria’s chemical weapons program, and the world watching the 2014 Winter Olympics in Sochi, Russia; we expect the government controls to loosen providing an economic boost on top of a general recovery in equity prices.” That was an excerpt taken from a letter I wrote to clients in November of last year, 2013. My timing was nearly perfect in choosing the precise opposite moment to go long Russian equities. The comments occurred at what would prove to be the high-water mark for the Russian equity markets to date. What seemed like unrelated developments in neighboring Ukraine would prove to be a harbinger for things to come. In December 2013 more than 800,000 protesters occupied Ukraine’s Kiev city hall and Independence Square in Ukraine. And by February 22nd, after months of violence and the resignation of Ukrainian Prime Minister Mykola Azarov, the government collapsed as protesters took control of presidential administrative buildings and President Yanukovych fled the country. Less than a week later “pro-Russian” gunmen responded to the collapse of the regime by seizing key buildings in the Crimean capital, Simferopol. On March 16th, Crimea seceded from Ukraine and two days later Russian President Vladimir Putin signed a bill absorbing Crimea into Russia. Since Crimea’s annexation, violent clashes between the new Ukrainian government and pro-Russian militants have continued along the Russian-Ukrainian border. Tensions between the European Union, along with the U.S., and Russia continued to mount as violence escalated. On July 30, 2014 the EU and U.S., along with other NATO nations, announced sanctions against Russia. Little progress toward a peaceful outcome has been made in the months since. The sanctions imposed in July were directed at Russia’s economy. Specifically against the financial sector and the majority government-owned Russian banks. Additional trade restrictions were aimed at the energy and defense industries along with individuals and entities whose overseas assets were frozen. Sanctions have continued to strengthen and have been adopted by additional countries around the world putting a severe strain on the Russian economy. Even before the sanctions, Russia’s perceived involvement in the fighting had already taken a toll on Russian equities as their markets fell by 25% by the spring of 2014, as seen here by the Market Vectors Russia ETF (NYSEARCA: RSX ): By autumn, the Russian real economy was showing the strains from the bite of sanctions. As if things could not have been getting any worse for Russian markets the price of oil had also begun a precipitous fall in June of this year and has not yet stopped even with the price of crude having been cut in half. While prices seem to have stabilized in the past couple of weeks it is still unclear as to whether or not that massive fall is now over or if we might still see more downside pressure. Just over half of Russia’s stock market capitalization is made up of oil and gas producers. As is always the case, oil producers have fallen in tandem with Brent Crude prices helping to push the overall Russian markets down an impressive 47% this year, making it the worst performer anywhere in 2014. As a result of oil’s depreciated price and the sanctions against their financial industry, the Russian Ruble has collapsed 70% against the U.S dollar putting even further pressure on the economy as the price of necessary imports become unaffordable. All of the above factors have pushed Russia into what is expected to be a deep recession next year. Data released by the Economy Ministry of Russia on December 29th showed the country’s GDP shrinking 0.5% in November. This was the first contraction since September 2009 during the global financial crisis and follows forecasts for GDP to fall as much as 4.7% in 2015 if oil prices remain at current levels. So the question now is whether or not all of this bad news has been priced into an already fundamentally ‘cheap’ market? Over the past 10 years Russian shares have traded at a discount to other emerging markets with an average Price-to-Earnings (P/E) ratio of 7.1. This discount reflects the country’s political risks as well as its dependence on the cyclical energy industry. While a discount is deserved, current valuations are reaching levels of absurdity. The U.S. based ETF RSX, whose stated goal is to “replicate as closely as possible, before fees and expenses, the price and yield performance of the Market Vectors Russia Index”, is the simplest way for U.S. investors to gain exposure to the overall Russian market. Currently the companies owned in the ETF portfolio have an average P/E of 6.55 and a Price-to-Book (P/B) ratio of 1.08. While certainly a discount to the country’s long term average it doesn’t exactly scream “bargain” at those valuations. A closer look at individual companies however yields a much different picture. Gazprom ( OTCQX:GZPFY ), the country’s largest company by market cap, currently trades at a P/E of 1.66 with a (P/B) ratio at 0.18. Sberbank ( OTCPK:SBRCY ), the country’s largest bank, trades at a P/E of 1.91 with a P/B at 0.35. OAO Tatneft ( OTCPK:OAOFY ), an oil and gas exploration company, trades at a P/E of 3.21 and P/B at 0.53 All of these companies are directly impacted by current and potential future sanctions, low oil prices, and the overall economic decline. They deserve to be trading at discounts to their foreign peers and historical averages. However, current valuations for these companies are absurdly low considering that they do have real value in their owned assets and their potential future earnings. When you can purchase $1.00 worth of assets for $0.18, as is the case with Gazprom based on their P/B ratio, or $0.35 and $0.53 on the dollar with Sberbenk and Tatneft respectively; I believe it to be a worthwhile endeavor to take a closer look at the potential opportunity. It is unlikely that all-out war will break out between NATO and Russia, as it would benefit no one. I also find it more likely that sanctions will begin to ease rather than tighten as the European Union is suffering economically from the imposed sanctions as well. It looks more and more likely that the EU will also fall into recession next year and I would expect them to start pushing back against any further sanctions suggested by the U.S. in an attempt to restore their own economies. It’s also important to remember that Europe is highly dependent on Russian energy exports for their own well-being and while finding replacement sources is not impossible it is substantially more expensive. While market participants’ sentiments may not have reached the point of maximum pessimism, and additional problems can certainly arise; at some point this market will bottom. Russia will continue to not only exist in the future but grow economically. An excellent contrarian play is developing. I wouldn’t attempt to call a bottom at current levels but when the situation does begin to improve, either through conciliatory actions by the Russian government leading to easing of sanctions or a price recovery in oil, or both, the market upside could be substantial for the brave few who take advantage at the right time. Scalper1 News

Russian companies may offer the best values in the world currently. Buying assets for pennies on the dollar. An excellent contrarian play is developing. “After an extremely strong performance by U.S. markets this year, it is our belief that emerging markets will be more in focus next year as investors rotate into underperforming areas. Of these markets, Russia, has the lowest fundamental valuation. With new positive light shining on President Vladimir Putin, after having negotiated a peaceful solution to Syria’s chemical weapons program, and the world watching the 2014 Winter Olympics in Sochi, Russia; we expect the government controls to loosen providing an economic boost on top of a general recovery in equity prices.” That was an excerpt taken from a letter I wrote to clients in November of last year, 2013. My timing was nearly perfect in choosing the precise opposite moment to go long Russian equities. The comments occurred at what would prove to be the high-water mark for the Russian equity markets to date. What seemed like unrelated developments in neighboring Ukraine would prove to be a harbinger for things to come. In December 2013 more than 800,000 protesters occupied Ukraine’s Kiev city hall and Independence Square in Ukraine. And by February 22nd, after months of violence and the resignation of Ukrainian Prime Minister Mykola Azarov, the government collapsed as protesters took control of presidential administrative buildings and President Yanukovych fled the country. Less than a week later “pro-Russian” gunmen responded to the collapse of the regime by seizing key buildings in the Crimean capital, Simferopol. On March 16th, Crimea seceded from Ukraine and two days later Russian President Vladimir Putin signed a bill absorbing Crimea into Russia. Since Crimea’s annexation, violent clashes between the new Ukrainian government and pro-Russian militants have continued along the Russian-Ukrainian border. Tensions between the European Union, along with the U.S., and Russia continued to mount as violence escalated. On July 30, 2014 the EU and U.S., along with other NATO nations, announced sanctions against Russia. Little progress toward a peaceful outcome has been made in the months since. The sanctions imposed in July were directed at Russia’s economy. Specifically against the financial sector and the majority government-owned Russian banks. Additional trade restrictions were aimed at the energy and defense industries along with individuals and entities whose overseas assets were frozen. Sanctions have continued to strengthen and have been adopted by additional countries around the world putting a severe strain on the Russian economy. Even before the sanctions, Russia’s perceived involvement in the fighting had already taken a toll on Russian equities as their markets fell by 25% by the spring of 2014, as seen here by the Market Vectors Russia ETF (NYSEARCA: RSX ): By autumn, the Russian real economy was showing the strains from the bite of sanctions. As if things could not have been getting any worse for Russian markets the price of oil had also begun a precipitous fall in June of this year and has not yet stopped even with the price of crude having been cut in half. While prices seem to have stabilized in the past couple of weeks it is still unclear as to whether or not that massive fall is now over or if we might still see more downside pressure. Just over half of Russia’s stock market capitalization is made up of oil and gas producers. As is always the case, oil producers have fallen in tandem with Brent Crude prices helping to push the overall Russian markets down an impressive 47% this year, making it the worst performer anywhere in 2014. As a result of oil’s depreciated price and the sanctions against their financial industry, the Russian Ruble has collapsed 70% against the U.S dollar putting even further pressure on the economy as the price of necessary imports become unaffordable. All of the above factors have pushed Russia into what is expected to be a deep recession next year. Data released by the Economy Ministry of Russia on December 29th showed the country’s GDP shrinking 0.5% in November. This was the first contraction since September 2009 during the global financial crisis and follows forecasts for GDP to fall as much as 4.7% in 2015 if oil prices remain at current levels. So the question now is whether or not all of this bad news has been priced into an already fundamentally ‘cheap’ market? Over the past 10 years Russian shares have traded at a discount to other emerging markets with an average Price-to-Earnings (P/E) ratio of 7.1. This discount reflects the country’s political risks as well as its dependence on the cyclical energy industry. While a discount is deserved, current valuations are reaching levels of absurdity. The U.S. based ETF RSX, whose stated goal is to “replicate as closely as possible, before fees and expenses, the price and yield performance of the Market Vectors Russia Index”, is the simplest way for U.S. investors to gain exposure to the overall Russian market. Currently the companies owned in the ETF portfolio have an average P/E of 6.55 and a Price-to-Book (P/B) ratio of 1.08. While certainly a discount to the country’s long term average it doesn’t exactly scream “bargain” at those valuations. A closer look at individual companies however yields a much different picture. Gazprom ( OTCQX:GZPFY ), the country’s largest company by market cap, currently trades at a P/E of 1.66 with a (P/B) ratio at 0.18. Sberbank ( OTCPK:SBRCY ), the country’s largest bank, trades at a P/E of 1.91 with a P/B at 0.35. OAO Tatneft ( OTCPK:OAOFY ), an oil and gas exploration company, trades at a P/E of 3.21 and P/B at 0.53 All of these companies are directly impacted by current and potential future sanctions, low oil prices, and the overall economic decline. They deserve to be trading at discounts to their foreign peers and historical averages. However, current valuations for these companies are absurdly low considering that they do have real value in their owned assets and their potential future earnings. When you can purchase $1.00 worth of assets for $0.18, as is the case with Gazprom based on their P/B ratio, or $0.35 and $0.53 on the dollar with Sberbenk and Tatneft respectively; I believe it to be a worthwhile endeavor to take a closer look at the potential opportunity. It is unlikely that all-out war will break out between NATO and Russia, as it would benefit no one. I also find it more likely that sanctions will begin to ease rather than tighten as the European Union is suffering economically from the imposed sanctions as well. It looks more and more likely that the EU will also fall into recession next year and I would expect them to start pushing back against any further sanctions suggested by the U.S. in an attempt to restore their own economies. It’s also important to remember that Europe is highly dependent on Russian energy exports for their own well-being and while finding replacement sources is not impossible it is substantially more expensive. While market participants’ sentiments may not have reached the point of maximum pessimism, and additional problems can certainly arise; at some point this market will bottom. Russia will continue to not only exist in the future but grow economically. An excellent contrarian play is developing. I wouldn’t attempt to call a bottom at current levels but when the situation does begin to improve, either through conciliatory actions by the Russian government leading to easing of sanctions or a price recovery in oil, or both, the market upside could be substantial for the brave few who take advantage at the right time. Scalper1 News

Scalper1 News