Scalper1 News

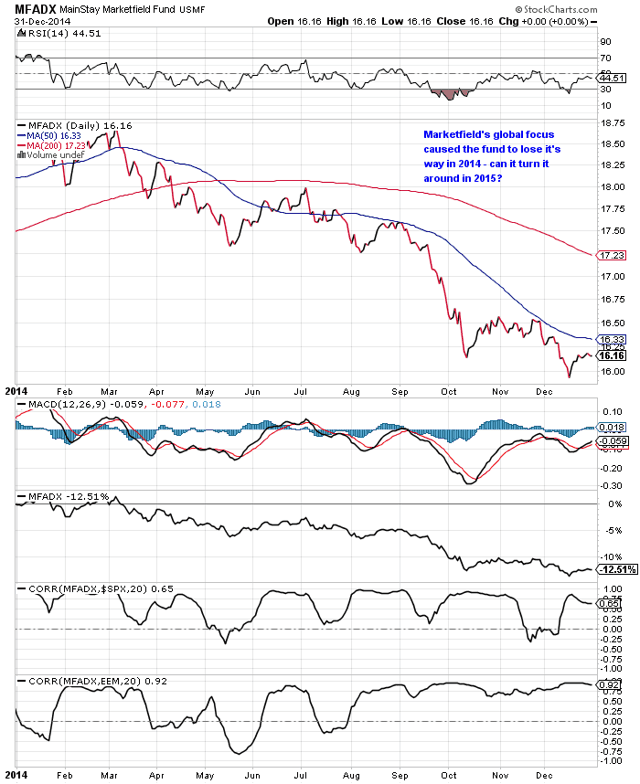

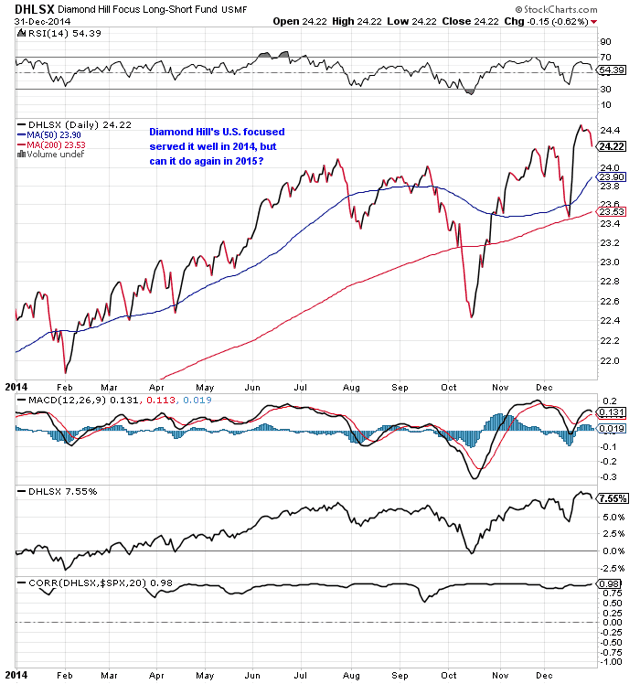

New Years Day is traditionally the time to make resolutions on how you can improve yourself in the coming year but instead of making some grand promise that you’ll finally lose those ten pounds, or stop drinking with lunch, why not focus on your financial future instead? Americans probably spend a fraction of the time focusing on their financial futures that they devote to avoiding Cool Ranch Doritos when they go to the market and yet most New Years Resolutions end in failure because people aren’t willing to put the time and mental energy into them to be successful. So to celebrate our first New Years resolution at the Yinzer Analyst, we’re going to share one of our biggest “d’oh” moments and the lesson we’re resolved to take forward in 2015 and by making my shame a matter of public record, you can all help me avoid repeating the misfortunes of 2014. Like many of the Yinzer Analysts’ biggest regrets, my worst moment in 2014 involved an ill-timed mutual fund investment in one of the year/s biggest losers and one of the worst “campers” I’ve ever invested with, Mainstay Marketfield (MUTF: MFADX ). At the start of the year, I had a minor “Hugh Hendry moment” and decided to up equity exposure, but instead of loading up on some large cap core fund, it was time to go hunting for “alpha” instead. Now alpha has to be one of the most widely used yet incredibly vague terms in existence. Everyone knows what it means but damn if they know how to go about getting it, just ask any of the 86% of core managers who underperformed their benchmark in 2014. In this context, I was focusing on managers who could deliver a healthy “risk-adjusted” return with low correlation to the S&P 500. My market expectations for the year were not TOO far off the mark; mid-to-upper single digits with higher volatility than in 2013. My goal was to find managers who could deliver a somewhat like market return with less drawdown. I didn’t expect market like performance, but I was hoping I could get 60% of the upside with less volatility. Being the Morningstar Direct wizard that I was, I naturally went through the category data until focusing more specifically on the Long/Short field. Now you couldn’t have found a bigger crop of losers than in long/short; as of 12/31/14 over the last five years they’ve managed to capture around 38% of the upside for about 51% of the downside for a five year annualized return of 6.85% compared to 15.45% for the S&P 500 TR. Not too impressive, especially given the relatively high fees charged by most managers. Now there were a select few managers I decided to pursue and ultimately focused on two names. The first was Mainstay which is really a global macro outfit that positions itself around global trends. Mainstay appeared to be the gem in the rough for a host of reasons: MFADX had a lower R2 to the S&P 500 but had managed to generate impressive performance through 2013 although it returned roughly half of the S&P 500’s 32% for that year. The subsequent beta it generated for to calculate alpha was then essentially worthless, but the positive return and lack of a reliable relationship to U.S. equities was a win in my book. Long Manager Track Record: The fund had a consistent management team that made itself readily available to answer questions. Part of my due diligence included a conference call with part of the management team. Global Focus: Much like the Yinzer Analyst, the fund looked favorably on Japan and Europe’s growth prospects versus the U.S. although it remained heavily invested at home. Information Sharing: One of the true hallmarks of a good fund is how much information its managers provide. When I was researching the fund in late 2013, you could access statements showing the monthly position in both long/short positions by market. But as I was going through my due diligence process, a few cracks in the story began to emerge that caused me more than a little hesitation: Prior Record: When going through the historical allocations, the first thing you would notice is how little their allocations actually changed from one period to the next. The fund was only down 12% in 2008 versus 37% for the S&P 500 but should have done even better. From what I can recollect, the fund had actually been adding equity exposure in late 2007 and was only saved from more serious losses by managing their inverse allocation. Over the next several years they made only small changes while leaving the core long equity allocation relatively unchanged. In 2009-2013 that was called prudent. Currently the fund has an annualized turnover of 32% and while not unusually low for long/short managers, MFADX does typically hold onto positions for extended periods. In other words, they’ve comfortable being wrong for a long period of time. Asset Growth: MFADX had very quickly grown into one of the largest long/short funds in America and in fact had one of the most impressive growth rates in 2013. Strong asset growth like that isn’t necessarily a negative, but tends to reinforce the belief amongst management that their investment philosophy is beyond reproach while also acting to limit their ability to make investment decisions. It’s a lot easier running a $100 million fund than a $10 billion dollar one. Ask Peter Lynch about it. Management: While having a long-term focus isn’t bad, that focus needs to be driven by a dynamic manager who can respond to changes in the market or their data but after 45 minutes of nonstop and entirely one sided dialogue, it became clear that intentionally unnamed manager, while very intelligent and well-spoken, was clearly locked into a specific market outlook. He was focused on a continuing global recovery that should see rates rise in the U.S. and abroad while focusing a large portion of the equity allocation on early global recovery leaders in the materials and capital goods fields. Think mining stocks and Joy Global while shorting Treasuries because you expect the ten year to burst through 3%. Oh, and also being long homebuilders and short utilities. Now that sounded like a great story but that’s what global macro investing is; focusing on selling a great story. Look at the December 2013 commentary if you want an example of this; it’s six pages devoted to the failure of global monetary policy and inflationary forces. What’s the old joke about economists? If you were to lock 2 in a room for an hour and ask them to tell you whether the economy is growing they’d come out with 3 different opinions. GDP growth in the U.S. stumbled early this year but has since recovered but the growth has been uneven. Wage growth has been anemic and the housing recovery went nowhere in 2014, killing Mainstay on several of its long and short positions. Utilities were one of the biggest winners in 2014, so their short Utilities Select Sector SPDR ETF ( XLU) position helped the fund stumble out of the gate. (click to enlarge) Meanwhile, the global recovery was stillborn so European and Japanese positions continued to lose ground, as did new positions in EM equities in select markets like Hong Kong, Mexico and Brazil. The downfall of Mainstay obviously wasn’t a 2% position in Brazilian equities, but how they reacted to their underperformance. They didn’t adjust many of their long positions quickly enough to prevent serious losses in the first half of 2014, only to add to EM equity exposure in their summer, just in time to take part in the summer shellacking. I would love to tell you more about their missteps, but after their July/August commentary they stopped publishing further updates, despite traditionally having done it on monthly basis. Never a good sign when a fund that loves to chat about their positions suddenly goes quiet. Once their portfolio holdings through year-end are made available I plan to do more digging, but it might be a lonely exercise this year. At the end of 2013, the fund had net assets of over $19 billion, while according to Morningstar it’s now closer to $9.1 billion. Those wirehouse boys sure are a fickle lot. While Marketfield may be a true global macro fund, my second choice was a very traditional long/short fund, Diamond Hill Long/Short (DHLSX.) I decided to pair a traditional long/short manager with a strict U.S. focus with a global macro manager both for diversification of return sources as well as a sort of academic exercise. Depending on how well they did, whoever performed the best would get the entire allocation. DHLSX had everything I liked; stable management, consistent returns in the top quartile of funds, they were very approachable when it came to answering questions and providing information but most of all, they had a specific approach to investing. Let’s be upfront about this, the Yinzer Analyst is a simple man and he likes to keep things simple. The more opaque you make the process, the more likely I am to think that you’re hiding something and I hate having to dig through old allocation reports or do a returns based analysis. What I enjoyed most about this fund was that Diamond Hill had a very simple approach to investing. They were classic, fundamental bottom up researchers who don’t care about how far their weightings might drift from the benchmark, although they do emphasize risk control on their short positions. To put it simply, they bought what they thought was cheap and sold short what they thought was too expensive; essentially the most basic definition of a long/short fund. While they didn’t set the long/short world on fire in 2014, they did manage a respectable 7.55% which, while underperforming a traditional 60/40 portfolio, its returns did have a monthly standard deviation in 2014 approximately half that of the S&P 500. Unfortunately, its July and September monthly losses were nearly as bad or worse than the broader market but with less upside in August and the late fall rally. (click to enlarge) So by know you’re asking the obvious question of why I would invest in a fund if I had such serious concerns about it? For the same reasons that most investors wind up making REALLY bad decisions; because they feel they have to do SOMETHING! My mistake wasn’t talking myself into investing with a manager who wasn’t nearly as active as he claimed to be, stuck in his rigid outlook and charging a high fee for his performance. My mistake was going against my gut and investing in a fund I knew had issues, but I was going to pull a Costanza and do the opposite of what my gut told me and hope for the best. Fortunately for me, I was able to trim my allocation after one quarter and sell-out completely after two, limiting my downside to less than 5% while the S&P 500 was up over 5%. If I have been stuck in the fund all year, I would have been drastically better of investing in what I call my naive portfolio of 60% SPDR S&P 500 Trust ETF (NYSEARCA: SPY )/40% i Shares Core Total U.S. Bond Market ETF ( AGG) to the tune of 2178 basis points difference in performance. So when the market opens tomorrow; what will you choose to do? Are you going to hold your nose and hope for the best or are you going to put the time into to make your resolutions a success? Scalper1 News

New Years Day is traditionally the time to make resolutions on how you can improve yourself in the coming year but instead of making some grand promise that you’ll finally lose those ten pounds, or stop drinking with lunch, why not focus on your financial future instead? Americans probably spend a fraction of the time focusing on their financial futures that they devote to avoiding Cool Ranch Doritos when they go to the market and yet most New Years Resolutions end in failure because people aren’t willing to put the time and mental energy into them to be successful. So to celebrate our first New Years resolution at the Yinzer Analyst, we’re going to share one of our biggest “d’oh” moments and the lesson we’re resolved to take forward in 2015 and by making my shame a matter of public record, you can all help me avoid repeating the misfortunes of 2014. Like many of the Yinzer Analysts’ biggest regrets, my worst moment in 2014 involved an ill-timed mutual fund investment in one of the year/s biggest losers and one of the worst “campers” I’ve ever invested with, Mainstay Marketfield (MUTF: MFADX ). At the start of the year, I had a minor “Hugh Hendry moment” and decided to up equity exposure, but instead of loading up on some large cap core fund, it was time to go hunting for “alpha” instead. Now alpha has to be one of the most widely used yet incredibly vague terms in existence. Everyone knows what it means but damn if they know how to go about getting it, just ask any of the 86% of core managers who underperformed their benchmark in 2014. In this context, I was focusing on managers who could deliver a healthy “risk-adjusted” return with low correlation to the S&P 500. My market expectations for the year were not TOO far off the mark; mid-to-upper single digits with higher volatility than in 2013. My goal was to find managers who could deliver a somewhat like market return with less drawdown. I didn’t expect market like performance, but I was hoping I could get 60% of the upside with less volatility. Being the Morningstar Direct wizard that I was, I naturally went through the category data until focusing more specifically on the Long/Short field. Now you couldn’t have found a bigger crop of losers than in long/short; as of 12/31/14 over the last five years they’ve managed to capture around 38% of the upside for about 51% of the downside for a five year annualized return of 6.85% compared to 15.45% for the S&P 500 TR. Not too impressive, especially given the relatively high fees charged by most managers. Now there were a select few managers I decided to pursue and ultimately focused on two names. The first was Mainstay which is really a global macro outfit that positions itself around global trends. Mainstay appeared to be the gem in the rough for a host of reasons: MFADX had a lower R2 to the S&P 500 but had managed to generate impressive performance through 2013 although it returned roughly half of the S&P 500’s 32% for that year. The subsequent beta it generated for to calculate alpha was then essentially worthless, but the positive return and lack of a reliable relationship to U.S. equities was a win in my book. Long Manager Track Record: The fund had a consistent management team that made itself readily available to answer questions. Part of my due diligence included a conference call with part of the management team. Global Focus: Much like the Yinzer Analyst, the fund looked favorably on Japan and Europe’s growth prospects versus the U.S. although it remained heavily invested at home. Information Sharing: One of the true hallmarks of a good fund is how much information its managers provide. When I was researching the fund in late 2013, you could access statements showing the monthly position in both long/short positions by market. But as I was going through my due diligence process, a few cracks in the story began to emerge that caused me more than a little hesitation: Prior Record: When going through the historical allocations, the first thing you would notice is how little their allocations actually changed from one period to the next. The fund was only down 12% in 2008 versus 37% for the S&P 500 but should have done even better. From what I can recollect, the fund had actually been adding equity exposure in late 2007 and was only saved from more serious losses by managing their inverse allocation. Over the next several years they made only small changes while leaving the core long equity allocation relatively unchanged. In 2009-2013 that was called prudent. Currently the fund has an annualized turnover of 32% and while not unusually low for long/short managers, MFADX does typically hold onto positions for extended periods. In other words, they’ve comfortable being wrong for a long period of time. Asset Growth: MFADX had very quickly grown into one of the largest long/short funds in America and in fact had one of the most impressive growth rates in 2013. Strong asset growth like that isn’t necessarily a negative, but tends to reinforce the belief amongst management that their investment philosophy is beyond reproach while also acting to limit their ability to make investment decisions. It’s a lot easier running a $100 million fund than a $10 billion dollar one. Ask Peter Lynch about it. Management: While having a long-term focus isn’t bad, that focus needs to be driven by a dynamic manager who can respond to changes in the market or their data but after 45 minutes of nonstop and entirely one sided dialogue, it became clear that intentionally unnamed manager, while very intelligent and well-spoken, was clearly locked into a specific market outlook. He was focused on a continuing global recovery that should see rates rise in the U.S. and abroad while focusing a large portion of the equity allocation on early global recovery leaders in the materials and capital goods fields. Think mining stocks and Joy Global while shorting Treasuries because you expect the ten year to burst through 3%. Oh, and also being long homebuilders and short utilities. Now that sounded like a great story but that’s what global macro investing is; focusing on selling a great story. Look at the December 2013 commentary if you want an example of this; it’s six pages devoted to the failure of global monetary policy and inflationary forces. What’s the old joke about economists? If you were to lock 2 in a room for an hour and ask them to tell you whether the economy is growing they’d come out with 3 different opinions. GDP growth in the U.S. stumbled early this year but has since recovered but the growth has been uneven. Wage growth has been anemic and the housing recovery went nowhere in 2014, killing Mainstay on several of its long and short positions. Utilities were one of the biggest winners in 2014, so their short Utilities Select Sector SPDR ETF ( XLU) position helped the fund stumble out of the gate. (click to enlarge) Meanwhile, the global recovery was stillborn so European and Japanese positions continued to lose ground, as did new positions in EM equities in select markets like Hong Kong, Mexico and Brazil. The downfall of Mainstay obviously wasn’t a 2% position in Brazilian equities, but how they reacted to their underperformance. They didn’t adjust many of their long positions quickly enough to prevent serious losses in the first half of 2014, only to add to EM equity exposure in their summer, just in time to take part in the summer shellacking. I would love to tell you more about their missteps, but after their July/August commentary they stopped publishing further updates, despite traditionally having done it on monthly basis. Never a good sign when a fund that loves to chat about their positions suddenly goes quiet. Once their portfolio holdings through year-end are made available I plan to do more digging, but it might be a lonely exercise this year. At the end of 2013, the fund had net assets of over $19 billion, while according to Morningstar it’s now closer to $9.1 billion. Those wirehouse boys sure are a fickle lot. While Marketfield may be a true global macro fund, my second choice was a very traditional long/short fund, Diamond Hill Long/Short (DHLSX.) I decided to pair a traditional long/short manager with a strict U.S. focus with a global macro manager both for diversification of return sources as well as a sort of academic exercise. Depending on how well they did, whoever performed the best would get the entire allocation. DHLSX had everything I liked; stable management, consistent returns in the top quartile of funds, they were very approachable when it came to answering questions and providing information but most of all, they had a specific approach to investing. Let’s be upfront about this, the Yinzer Analyst is a simple man and he likes to keep things simple. The more opaque you make the process, the more likely I am to think that you’re hiding something and I hate having to dig through old allocation reports or do a returns based analysis. What I enjoyed most about this fund was that Diamond Hill had a very simple approach to investing. They were classic, fundamental bottom up researchers who don’t care about how far their weightings might drift from the benchmark, although they do emphasize risk control on their short positions. To put it simply, they bought what they thought was cheap and sold short what they thought was too expensive; essentially the most basic definition of a long/short fund. While they didn’t set the long/short world on fire in 2014, they did manage a respectable 7.55% which, while underperforming a traditional 60/40 portfolio, its returns did have a monthly standard deviation in 2014 approximately half that of the S&P 500. Unfortunately, its July and September monthly losses were nearly as bad or worse than the broader market but with less upside in August and the late fall rally. (click to enlarge) So by know you’re asking the obvious question of why I would invest in a fund if I had such serious concerns about it? For the same reasons that most investors wind up making REALLY bad decisions; because they feel they have to do SOMETHING! My mistake wasn’t talking myself into investing with a manager who wasn’t nearly as active as he claimed to be, stuck in his rigid outlook and charging a high fee for his performance. My mistake was going against my gut and investing in a fund I knew had issues, but I was going to pull a Costanza and do the opposite of what my gut told me and hope for the best. Fortunately for me, I was able to trim my allocation after one quarter and sell-out completely after two, limiting my downside to less than 5% while the S&P 500 was up over 5%. If I have been stuck in the fund all year, I would have been drastically better of investing in what I call my naive portfolio of 60% SPDR S&P 500 Trust ETF (NYSEARCA: SPY )/40% i Shares Core Total U.S. Bond Market ETF ( AGG) to the tune of 2178 basis points difference in performance. So when the market opens tomorrow; what will you choose to do? Are you going to hold your nose and hope for the best or are you going to put the time into to make your resolutions a success? Scalper1 News

Scalper1 News