Scalper1 News

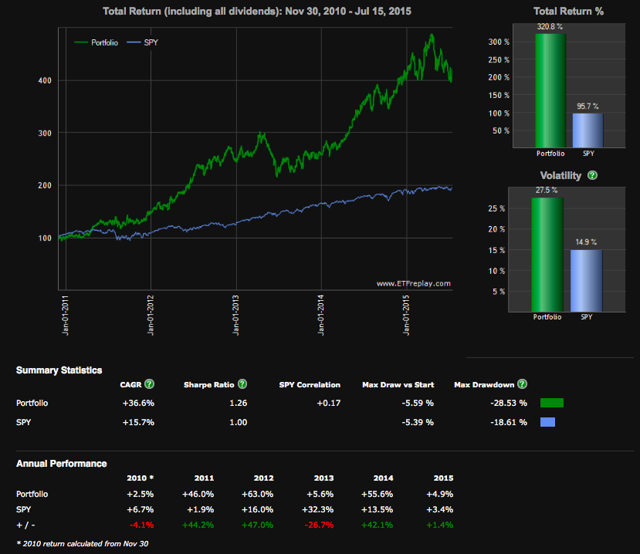

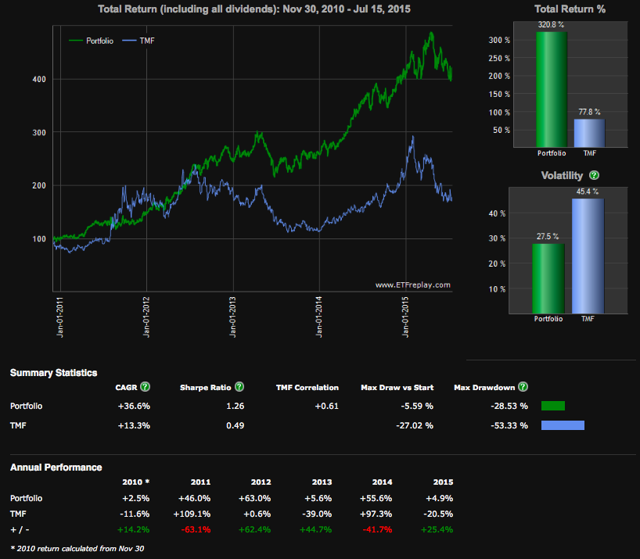

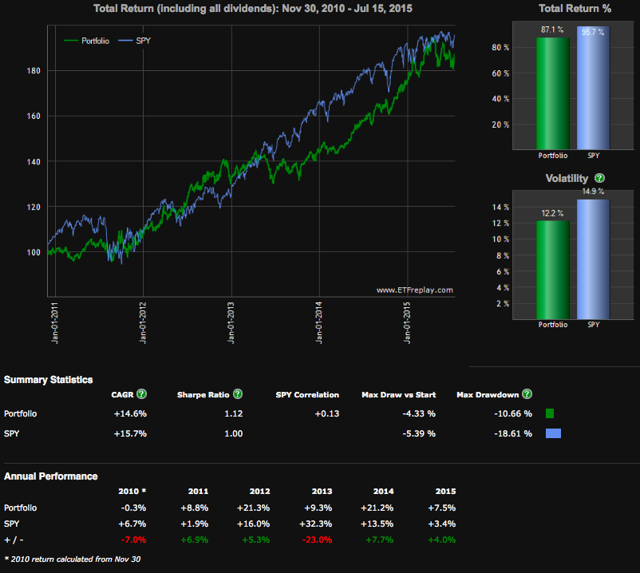

Adding long dollar index exposure is highly logical. It reduces the strategy index’s correlation to bonds. And it provides multiple forms of statistical hedging. As long time readers know, the idea behind Structural Arbitrage is that profits are possible by acting as a synthetic insurance company which sells expensive insurance in the volatility market, and then synthetically reinsures that market risk with long duration government bonds. To review, here are the basic strategy index’s rules: I. Buy XIV (NASDAQ: XIV ) with 40% of the dollar value of the portfolio. II. Buy TMF (NYSEARCA: TMF ) with 60% of the dollar value of the portfolio. III. Rebalance weekly to maintain the 40%/ 60% dollar value split between the positions. XIV is the inverse short term volatility ETN. TMF is the 3X leveraged 20+ year government bond ETF. Here are the strategy’s results in a linear scale: (click to enlarge) For those of you who don’t believe that such a simple strategy index could work, I made the strategy public in an ebook back in 2013. If a relationship is robust, it can still make money even if it is widely studied. The potential problem, though, is the correlation of the strategy to bonds, as we can see in the graph below which compares the strategy to its TMF component: (click to enlarge) Even though the R squared value of a 0.61 correlation to TMF isn’t horrible, it’s not great either. And as I’ve said again and again , I believe that the strategy in its original form should be abandoned, due to the risk of a prolonged bear market in bonds. A simple improvement would be to add long dollar index exposure through an instrument such as UUP. The logic is “if then” logic. If interest rates rise, TMF will fall, but the dollar might strengthen, since the higher yield makes dollars more attractive than alternatives. What exactly would an improvement consist of? Here are the improved strategy’s rules: I. Buy XIV (NASDAQ:) with 15% of the dollar value of the portfolio. II. Buy TMF (NYSEARCA:) with 15% of the dollar value of the portfolio. III. Buy UUP (NYSEARCA: UUP ) with 70% of the dollar value of the portfolio. IV. Rebalance annually to maintain the 15%/ 15%/70% dollar value split between the positions. Here are the strategy’s results in a linear scale: (click to enlarge) The strategy now lags the S&P by 1.1% per year, but the drawdown is reduced by almost 8 percentage points, far improving the CAGR/Max drawdown ratio, called the MAR, compared to that of S&P 500. Let’s take a look at the correlation of the strategy to its long bond TMF component: (click to enlarge) The improved strategy index’s correlation to TMF dropped from 0.61 to 0.35. And the improved strategy index’s correlation to the S&P 500 is only 0.13 (pretty amazing) dropping from an already impressive 0.17 level. For the investor who is looking for a return stream which is largely uncorrelated to stocks and uncorrelated to bonds , this improved strategy index is pretty neat. Both long bonds and long dollar index exposure can often statistically hedge short volatility exposure. The lesson here is that multiple forms of hedging are usually better if the goal is robustness and non-correlation. Thanks for reading. Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in XIV, TMF, UUP over the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Scalper1 News

Adding long dollar index exposure is highly logical. It reduces the strategy index’s correlation to bonds. And it provides multiple forms of statistical hedging. As long time readers know, the idea behind Structural Arbitrage is that profits are possible by acting as a synthetic insurance company which sells expensive insurance in the volatility market, and then synthetically reinsures that market risk with long duration government bonds. To review, here are the basic strategy index’s rules: I. Buy XIV (NASDAQ: XIV ) with 40% of the dollar value of the portfolio. II. Buy TMF (NYSEARCA: TMF ) with 60% of the dollar value of the portfolio. III. Rebalance weekly to maintain the 40%/ 60% dollar value split between the positions. XIV is the inverse short term volatility ETN. TMF is the 3X leveraged 20+ year government bond ETF. Here are the strategy’s results in a linear scale: (click to enlarge) For those of you who don’t believe that such a simple strategy index could work, I made the strategy public in an ebook back in 2013. If a relationship is robust, it can still make money even if it is widely studied. The potential problem, though, is the correlation of the strategy to bonds, as we can see in the graph below which compares the strategy to its TMF component: (click to enlarge) Even though the R squared value of a 0.61 correlation to TMF isn’t horrible, it’s not great either. And as I’ve said again and again , I believe that the strategy in its original form should be abandoned, due to the risk of a prolonged bear market in bonds. A simple improvement would be to add long dollar index exposure through an instrument such as UUP. The logic is “if then” logic. If interest rates rise, TMF will fall, but the dollar might strengthen, since the higher yield makes dollars more attractive than alternatives. What exactly would an improvement consist of? Here are the improved strategy’s rules: I. Buy XIV (NASDAQ:) with 15% of the dollar value of the portfolio. II. Buy TMF (NYSEARCA:) with 15% of the dollar value of the portfolio. III. Buy UUP (NYSEARCA: UUP ) with 70% of the dollar value of the portfolio. IV. Rebalance annually to maintain the 15%/ 15%/70% dollar value split between the positions. Here are the strategy’s results in a linear scale: (click to enlarge) The strategy now lags the S&P by 1.1% per year, but the drawdown is reduced by almost 8 percentage points, far improving the CAGR/Max drawdown ratio, called the MAR, compared to that of S&P 500. Let’s take a look at the correlation of the strategy to its long bond TMF component: (click to enlarge) The improved strategy index’s correlation to TMF dropped from 0.61 to 0.35. And the improved strategy index’s correlation to the S&P 500 is only 0.13 (pretty amazing) dropping from an already impressive 0.17 level. For the investor who is looking for a return stream which is largely uncorrelated to stocks and uncorrelated to bonds , this improved strategy index is pretty neat. Both long bonds and long dollar index exposure can often statistically hedge short volatility exposure. The lesson here is that multiple forms of hedging are usually better if the goal is robustness and non-correlation. Thanks for reading. Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in XIV, TMF, UUP over the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Scalper1 News

Scalper1 News