Scalper1 News

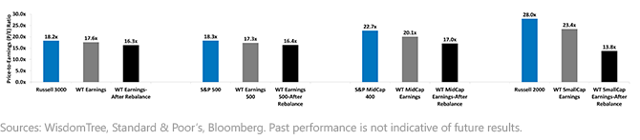

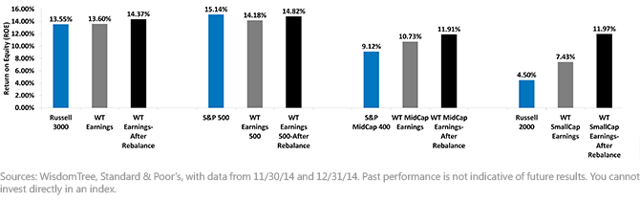

By Jeremy Schwartz A key process driving the WisdomTree earnings-weighted Index approach is a rebalancing process that refreshes constituent weights based on changes in Earnings Stream® and relative value. In earnings-weighted indexes, changes at the rebalance are made based on each stock’s relative price appreciation compared to its relative earnings growth: Companies whose stock prices increased compared to their peers’ while their earnings decreased compared to their peers’ would typically see reduced weight in the WisdomTree Earnings Indexes. In a market cap-weighted index, the only driver of weight is the relative change in market capitalization, which is usually driven by the stock price. Companies whose stock prices fell while their earnings were flat or grew would typically see increased weight in the WisdomTree Earnings Indexes. Companies that have not been profitable on a cumulative basis over the previous four quarters are removed to ensure the continued focus on earnings-generating stocks-one element that improves the quality of the basket by removing more speculative, unprofitable ventures. Weight is also shifted to the relatively more profitable companies and those that have seen highest earnings growth. One way to gauge the impact of the rebalance process is to look at the price-to-earnings (P/E) ratio, essentially the price of the Index divided by its earnings per share before and after the rebalance. Below we show the P/E multiples across market segments. As will be shown, the rebalance can have a large impact on a portfolio’s P/E ratio. U.S. Equity Index Estimated 12-Month P/E Ratios* (as of 11/30/14) (click to enlarge) For definitions of terms and indexes in the chart, visit our glossary . A Lower P/E Ratio Approach: Even prior to the 2014 rebalance, each earnings-weighted Index exhibited a lower P/E ratio than its market capitalization-weighted counterpart. After the rebalance, the P/E ratios dropped even more significantly compared to these benchmarks. This is a key benefit of the annual rebalance process that forces the discipline of reweighting to the fundamental value of the underlying constituents in the Index. Multiples Contracted Anywhere between 7% and 40% across All Indexes: The WisdomTree SmallCap Earnings Index saw multiples contract the greatest at approximately 40%. WisdomTree requires each constituent of its earnings family to demonstrate profitability. This addresses the problem seen in the Russell 2000 Index -namely, a high index-level P/E ratio that is due to index-level earnings being depressed by constituents with negative earnings-by eliminating firms that have had negative earnings over the prior 12 months. Since there are more constituents in small-cap indexes that have delivered negative earnings over the prior 12 months than there are in large-cap indexes, this effect is more pronounced within this size segment. Rebalance Track Record-Consistency in Raising Return on Equity (ROE) Now that we have studied the impact of the rebalance on lowering P/E multiples, we will show the impact of the rebalance in helping to raise the “quality” of the earnings Indexes, measured by the ROE. Post-Rebalance Raising ROE and Improving Quality (click to enlarge) For definitions of terms and indexes in the chart, visit our glossary. This chart illustrates how the rebalance has raised the ROE across four WisdomTree Earnings Indexes. In the 2014 rebalance, for example, the ROE of the WisdomTree SmallCap Earnings Index before and after the rebalance was 7.43% and 11.97%, respectively. As the bull market in equities carries on, it becomes ever more important to pay attention to the underlying valuations and market fundamentals. Above we show how the rebalance both lowered the P/E ratios of each WisdomTree Earnings Index and raised the ROE, a key metric of quality. We believe these are attractive attributes of market exposures, made even more important by the continued gains in the market we have seen in recent years. Important Risks Related to this Article Investments focusing on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. Jeremy Schwartz, Director of Research As WisdomTree’s Director of Research, Jeremy Schwartz offers timely ideas and timeless wisdom on a bi-monthly basis. Prior to joining WisdomTree, Jeremy was Professor Jeremy Siegel’s head research assistant and helped with the research and writing of Stocks for the Long Run and The Future for Investors. He is also the co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” and the Wall Street Journal article “The Great American Bond Bubble.” Scalper1 News

By Jeremy Schwartz A key process driving the WisdomTree earnings-weighted Index approach is a rebalancing process that refreshes constituent weights based on changes in Earnings Stream® and relative value. In earnings-weighted indexes, changes at the rebalance are made based on each stock’s relative price appreciation compared to its relative earnings growth: Companies whose stock prices increased compared to their peers’ while their earnings decreased compared to their peers’ would typically see reduced weight in the WisdomTree Earnings Indexes. In a market cap-weighted index, the only driver of weight is the relative change in market capitalization, which is usually driven by the stock price. Companies whose stock prices fell while their earnings were flat or grew would typically see increased weight in the WisdomTree Earnings Indexes. Companies that have not been profitable on a cumulative basis over the previous four quarters are removed to ensure the continued focus on earnings-generating stocks-one element that improves the quality of the basket by removing more speculative, unprofitable ventures. Weight is also shifted to the relatively more profitable companies and those that have seen highest earnings growth. One way to gauge the impact of the rebalance process is to look at the price-to-earnings (P/E) ratio, essentially the price of the Index divided by its earnings per share before and after the rebalance. Below we show the P/E multiples across market segments. As will be shown, the rebalance can have a large impact on a portfolio’s P/E ratio. U.S. Equity Index Estimated 12-Month P/E Ratios* (as of 11/30/14) (click to enlarge) For definitions of terms and indexes in the chart, visit our glossary . A Lower P/E Ratio Approach: Even prior to the 2014 rebalance, each earnings-weighted Index exhibited a lower P/E ratio than its market capitalization-weighted counterpart. After the rebalance, the P/E ratios dropped even more significantly compared to these benchmarks. This is a key benefit of the annual rebalance process that forces the discipline of reweighting to the fundamental value of the underlying constituents in the Index. Multiples Contracted Anywhere between 7% and 40% across All Indexes: The WisdomTree SmallCap Earnings Index saw multiples contract the greatest at approximately 40%. WisdomTree requires each constituent of its earnings family to demonstrate profitability. This addresses the problem seen in the Russell 2000 Index -namely, a high index-level P/E ratio that is due to index-level earnings being depressed by constituents with negative earnings-by eliminating firms that have had negative earnings over the prior 12 months. Since there are more constituents in small-cap indexes that have delivered negative earnings over the prior 12 months than there are in large-cap indexes, this effect is more pronounced within this size segment. Rebalance Track Record-Consistency in Raising Return on Equity (ROE) Now that we have studied the impact of the rebalance on lowering P/E multiples, we will show the impact of the rebalance in helping to raise the “quality” of the earnings Indexes, measured by the ROE. Post-Rebalance Raising ROE and Improving Quality (click to enlarge) For definitions of terms and indexes in the chart, visit our glossary. This chart illustrates how the rebalance has raised the ROE across four WisdomTree Earnings Indexes. In the 2014 rebalance, for example, the ROE of the WisdomTree SmallCap Earnings Index before and after the rebalance was 7.43% and 11.97%, respectively. As the bull market in equities carries on, it becomes ever more important to pay attention to the underlying valuations and market fundamentals. Above we show how the rebalance both lowered the P/E ratios of each WisdomTree Earnings Index and raised the ROE, a key metric of quality. We believe these are attractive attributes of market exposures, made even more important by the continued gains in the market we have seen in recent years. Important Risks Related to this Article Investments focusing on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. Jeremy Schwartz, Director of Research As WisdomTree’s Director of Research, Jeremy Schwartz offers timely ideas and timeless wisdom on a bi-monthly basis. Prior to joining WisdomTree, Jeremy was Professor Jeremy Siegel’s head research assistant and helped with the research and writing of Stocks for the Long Run and The Future for Investors. He is also the co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” and the Wall Street Journal article “The Great American Bond Bubble.” Scalper1 News

Scalper1 News