Scalper1 News

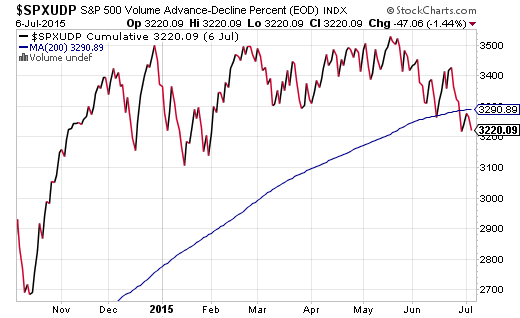

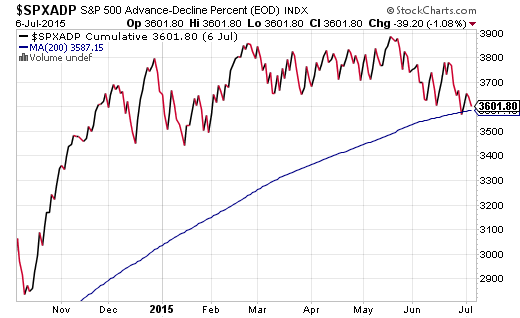

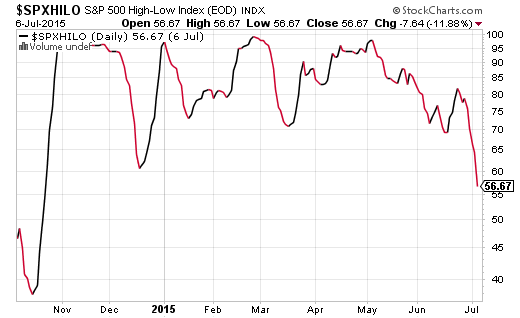

Investors erroneously focus on which human interest story, or combination of issues, is/are of greatest importance. However, the root cause of every high-profile concern is debt-fueled excess. It follows that a responsible media should refrain from concocting unknowable storms and, instead, hone in on the risks associated with ultra-low borrowing costs and/or exceptionally easy credit terms around the world. Lately, I have been fielding a host of “which is worse” questions. Is it the possibility of Greece exiting the euro-zone or is it the potential for Puerto Rico to default on its debt? Is it the 25%-plus bearish retrenchment of China’s Shanghai SSE Composite or is it the likelihood of eventual rate hikes by the U.S. Federal Reserve? In truth, investors erroneously focus on which human interest story, or combination of issues, is/are of greatest importance. However, the root cause of every high-profile concern is debt-fueled excess . It follows that a responsible media should refrain from concocting unknowable storms and, instead, hone in on the risks associated with ultra-low borrowing costs and/or exceptionally easy credit terms around the world. For the purpose of understanding, let’s discuss the debt concerns of Greece, Puerto Rico and China, beginning with the Greek tragedy. Since the origin of the euro-zone, less productive and less economically successful countries had been able to borrow-n-spend at the same favorable rates as the most productive and most successful countries. That’s like giving a $50,000 line of credit to individuals with very different abilities to handle debt – like offering a card to a $200,000 per year earner with a 760 credit score as well as providing a card to a $50,000 per year earner with a 520 credit score. Sooner or later, one of the individuals will not be able to keep up. And in this case, Greece cannot keep up with Germany, Austria or Finland. (Neither can Portugal, Spain or Italy.) Easy borrowing and reckless spending has left Greece with few viable alternatives. Now let’s shift gears to Puerto Rico. Whereas the working-aged population employment rate/labor participation rate in the United States is 62.7%, this number is a mere 40% in Puerto Rico. Over the last decade, corporate tax breaks disappeared for a number of U.S. corporations operating in Puerto Rico, forcing the companies to leave and to take many of those jobs with them. Residents also left over the last decade due to limited job prospects and exorbitant local taxes as high as 33%. Less jobs, less people, high taxation… none of that stopped the Puerto Rican government from borrowing way beyond its means and running enormous deficits. Ironically, U.S. states are not allowed to use debt to increase budget deficits. Puerto Rico did. Eventually, the territory will be bailed out by congressional/While House decree or be permitted to seek some from of bankruptcy protection (after a law or two is passed). Now we come to China. And yes, I will stipulate that the recent turbulence in Chinese stocks as well as China’s underachieving economy as more critical to the performance of risk assets around the globe than Greece or Puerto Rico. This is China – the world’s 2nd largest economy behind only the United States. Of course China matters more than tiny countries or territories. So when loose rules surrounding margin debt helped fuel the miraculous rise in China’s Shanghai SSE Composite, and when the People’s Bank of China (PBOC) recently cut interest rates to ease lenders’ capital settings, and when the Securities Association of China announced that the country’s big brokerages had agreed to put up 120 billion yuan ($26 billion) to prop up Chinese blue-chip equities, one might have hoped for the party to go on. That’s not the case, though. Once again, investors need to take note of why China is struggling at all. Rate cuts mean easier money and excessive margin debt implies debt-fueled excess. As if that weren’t enough, the country’s total government, corporate and household debt load as of mid-2014 is roughly equal to 282 percent of the country’s total annual economic output. China’s debts are growing at a pace that is unsustainable. Debt-fueled excess explained the financial crisis in 2008 for the U.S. Is it any surprise, then, that Greece, Puerto Rico and China have been dealing with similar concerns related to easy credit? (Note: I am not saying that China is a lost cause the way Greece and Puerto Rico are, but simply, noticing the similarity in the genesis of debt-fueled excesses.) What does it all mean for risk assets stateside? Perhaps ironically, there is boundless love for the Federal Reserve in the United States. Nobody seems to believe that the Fed has ever made or will ever make a policy mistake. Yet the Fed erred in its rate policy leading up to the 2000 dot-com collapse; it faltered in keeping rates too low for too long leading up to the 2008 financial crisis, and then failing to recognize the severity of the coming recession in not cutting rates quickly enough. Will Greece, Puerto Rico and even China push the Fed toward keeping zero percent rates in place for all of 2015? Will seven years of zero-percent, ultra-easy rate policy be a good thing, then? And if so, when does it become a bad thing? As I have pointed out in previous columns, sky-high stock valuations and a lusterless domestic economy may not matter in the near-term. Yet they may begin to matter alongside battered faith in the central banks of Europe and/or China; they may begin to matter if waning confidence spreads to the Fed. One of the best ways to determine whether confidence is waning or holding firm is to check in on the market internals (a.k.a. breadth indicators ). Here are three considerations: The Advancing-Declining Volume Line (AD Volume Line) measures the buying and selling pressure behind a market advance or market decline. It goes up when advancing volume is positive; it falls when it is negative. In other words, if there is significant volume behind declining stocks, you have selling pressure and reason for caution. The pressure today is powerful enough for the volume behind decliners to push the AD Volume Line for the S&P 500 below its 200-day moving average for the first time since 2012. We can also look at the Advance/Decline (A/D) Line for the S&P 500. Although there has not been a definitive breakdown in the number of advancers participating in the bull market relative to decliners, the drop-off since mid-May is worthy of continued vigilance. Finally, investors should be mindful of the High-Low Index, This breadth indicator is based on new 52-week highs and new 52-week lows. In essence, when the High-Low Index is above 50, the stock index may be thought to be in an uptrend; when the index is below 50 – when new lows outnumber new highs – the trend may be considered bearish. The S&P 500 Hi-Lo at 56.67 is still positive today, though it sits at its lowest level in 2015. Income assets have been trimmed at the longest-end of the yield curve as well as the middle of the asset risk spectrum. We have concentrated our income in funds like the i Shares 3-7 Year Treasury Bond ETF (NYSEARCA: IEI ) and the BulletShares 2016 High Yield Corporate Bond ETF (NYSEARCA: BSJG ). Most notably, we have raised our cash component of the income picture. Growth assets have been trimmed in the foreign holdings arena. Several had hit stop-limit loss orders , leaving the combined cash from growth-n-income trimmings at roughly 15%-20%. Growth at 50%-55% of most portfolios is primarily comprised of funds that we have held onto for years, including funds like the Health Care Select Sect SPDR ETF (NYSEARCA: XLV ) , the iShares MSCI USA Minimum Volatility ETF (NYSEARCA: USMV ) and the Vanguard Mid-Cap Value ETF (NYSEARCA: VOE ). Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

Investors erroneously focus on which human interest story, or combination of issues, is/are of greatest importance. However, the root cause of every high-profile concern is debt-fueled excess. It follows that a responsible media should refrain from concocting unknowable storms and, instead, hone in on the risks associated with ultra-low borrowing costs and/or exceptionally easy credit terms around the world. Lately, I have been fielding a host of “which is worse” questions. Is it the possibility of Greece exiting the euro-zone or is it the potential for Puerto Rico to default on its debt? Is it the 25%-plus bearish retrenchment of China’s Shanghai SSE Composite or is it the likelihood of eventual rate hikes by the U.S. Federal Reserve? In truth, investors erroneously focus on which human interest story, or combination of issues, is/are of greatest importance. However, the root cause of every high-profile concern is debt-fueled excess . It follows that a responsible media should refrain from concocting unknowable storms and, instead, hone in on the risks associated with ultra-low borrowing costs and/or exceptionally easy credit terms around the world. For the purpose of understanding, let’s discuss the debt concerns of Greece, Puerto Rico and China, beginning with the Greek tragedy. Since the origin of the euro-zone, less productive and less economically successful countries had been able to borrow-n-spend at the same favorable rates as the most productive and most successful countries. That’s like giving a $50,000 line of credit to individuals with very different abilities to handle debt – like offering a card to a $200,000 per year earner with a 760 credit score as well as providing a card to a $50,000 per year earner with a 520 credit score. Sooner or later, one of the individuals will not be able to keep up. And in this case, Greece cannot keep up with Germany, Austria or Finland. (Neither can Portugal, Spain or Italy.) Easy borrowing and reckless spending has left Greece with few viable alternatives. Now let’s shift gears to Puerto Rico. Whereas the working-aged population employment rate/labor participation rate in the United States is 62.7%, this number is a mere 40% in Puerto Rico. Over the last decade, corporate tax breaks disappeared for a number of U.S. corporations operating in Puerto Rico, forcing the companies to leave and to take many of those jobs with them. Residents also left over the last decade due to limited job prospects and exorbitant local taxes as high as 33%. Less jobs, less people, high taxation… none of that stopped the Puerto Rican government from borrowing way beyond its means and running enormous deficits. Ironically, U.S. states are not allowed to use debt to increase budget deficits. Puerto Rico did. Eventually, the territory will be bailed out by congressional/While House decree or be permitted to seek some from of bankruptcy protection (after a law or two is passed). Now we come to China. And yes, I will stipulate that the recent turbulence in Chinese stocks as well as China’s underachieving economy as more critical to the performance of risk assets around the globe than Greece or Puerto Rico. This is China – the world’s 2nd largest economy behind only the United States. Of course China matters more than tiny countries or territories. So when loose rules surrounding margin debt helped fuel the miraculous rise in China’s Shanghai SSE Composite, and when the People’s Bank of China (PBOC) recently cut interest rates to ease lenders’ capital settings, and when the Securities Association of China announced that the country’s big brokerages had agreed to put up 120 billion yuan ($26 billion) to prop up Chinese blue-chip equities, one might have hoped for the party to go on. That’s not the case, though. Once again, investors need to take note of why China is struggling at all. Rate cuts mean easier money and excessive margin debt implies debt-fueled excess. As if that weren’t enough, the country’s total government, corporate and household debt load as of mid-2014 is roughly equal to 282 percent of the country’s total annual economic output. China’s debts are growing at a pace that is unsustainable. Debt-fueled excess explained the financial crisis in 2008 for the U.S. Is it any surprise, then, that Greece, Puerto Rico and China have been dealing with similar concerns related to easy credit? (Note: I am not saying that China is a lost cause the way Greece and Puerto Rico are, but simply, noticing the similarity in the genesis of debt-fueled excesses.) What does it all mean for risk assets stateside? Perhaps ironically, there is boundless love for the Federal Reserve in the United States. Nobody seems to believe that the Fed has ever made or will ever make a policy mistake. Yet the Fed erred in its rate policy leading up to the 2000 dot-com collapse; it faltered in keeping rates too low for too long leading up to the 2008 financial crisis, and then failing to recognize the severity of the coming recession in not cutting rates quickly enough. Will Greece, Puerto Rico and even China push the Fed toward keeping zero percent rates in place for all of 2015? Will seven years of zero-percent, ultra-easy rate policy be a good thing, then? And if so, when does it become a bad thing? As I have pointed out in previous columns, sky-high stock valuations and a lusterless domestic economy may not matter in the near-term. Yet they may begin to matter alongside battered faith in the central banks of Europe and/or China; they may begin to matter if waning confidence spreads to the Fed. One of the best ways to determine whether confidence is waning or holding firm is to check in on the market internals (a.k.a. breadth indicators ). Here are three considerations: The Advancing-Declining Volume Line (AD Volume Line) measures the buying and selling pressure behind a market advance or market decline. It goes up when advancing volume is positive; it falls when it is negative. In other words, if there is significant volume behind declining stocks, you have selling pressure and reason for caution. The pressure today is powerful enough for the volume behind decliners to push the AD Volume Line for the S&P 500 below its 200-day moving average for the first time since 2012. We can also look at the Advance/Decline (A/D) Line for the S&P 500. Although there has not been a definitive breakdown in the number of advancers participating in the bull market relative to decliners, the drop-off since mid-May is worthy of continued vigilance. Finally, investors should be mindful of the High-Low Index, This breadth indicator is based on new 52-week highs and new 52-week lows. In essence, when the High-Low Index is above 50, the stock index may be thought to be in an uptrend; when the index is below 50 – when new lows outnumber new highs – the trend may be considered bearish. The S&P 500 Hi-Lo at 56.67 is still positive today, though it sits at its lowest level in 2015. Income assets have been trimmed at the longest-end of the yield curve as well as the middle of the asset risk spectrum. We have concentrated our income in funds like the i Shares 3-7 Year Treasury Bond ETF (NYSEARCA: IEI ) and the BulletShares 2016 High Yield Corporate Bond ETF (NYSEARCA: BSJG ). Most notably, we have raised our cash component of the income picture. Growth assets have been trimmed in the foreign holdings arena. Several had hit stop-limit loss orders , leaving the combined cash from growth-n-income trimmings at roughly 15%-20%. Growth at 50%-55% of most portfolios is primarily comprised of funds that we have held onto for years, including funds like the Health Care Select Sect SPDR ETF (NYSEARCA: XLV ) , the iShares MSCI USA Minimum Volatility ETF (NYSEARCA: USMV ) and the Vanguard Mid-Cap Value ETF (NYSEARCA: VOE ). Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

Scalper1 News