Scalper1 News

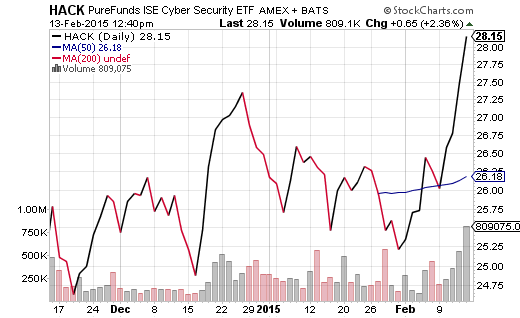

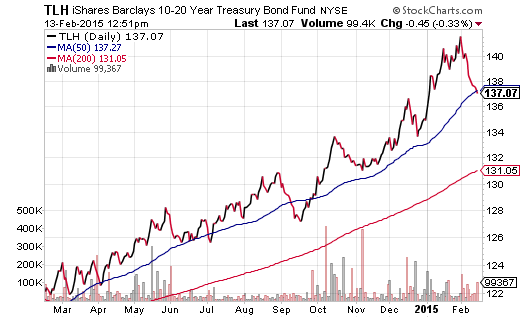

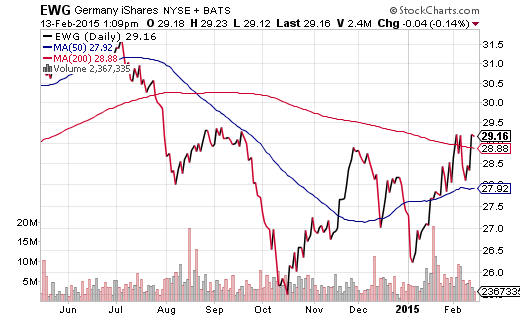

The craziness in currency manipulation is occurring on every continent and in every region. So why are these devaluation endeavors happening on such a massive scale? Investors need to take these activities into account in the assessment of risk versus reward. David Bowie and Mick Jagger may believe that people are dancing on every street corner around the world. In actuality, however, they’re desperately competing with neighbors by devaluing their currencies. The craziness in currency manipulation is occurring on every continent and in every region. Japan’s brazen quantitative easing (QE) program has seen the battered yen hurt China’s export-dependent economy, leading to speculation that the People’s Bank of China (PBOC) may need to weaken its yuan. Europe’s recently launched QE program has decimated the euro at the expense of non-member nations. In response, Denmark and Sweden have put forward negative interest rates to keep the Danish krone and Swedish krona from rising against the euro. And in the Americas? Mexico, Peru, Chile and Venezuela have all come under fire from neighboring countries for rate cut activity that has depreciated their respective currencies. So why are these devaluation endeavors happening on such a massive scale? The most obvious reason is the belief that weaker currencies promote exports that will stimulate a nation or region’s economic well-being. In today’s battle, however, strong currencies also force import prices down and that can create deflation. All across the globe, the threat of deflation-based recessionary pressure has caused central banks to loosen monetary policy. Lowering rates to zero percent, “going negative,” buying assets with electronically-created credits (a.k.a. “quantitative easing”) all lead to lower currencies against rivals. Since every major central bank, and even the minor ones, are now engaged in unusual efforts to stimulate respective economies – since everyone is debasing paper money – investors need to take these activities into account in the assessment of risk versus reward. We know that the U.S. Federal Reserve succeeded in reflating the value of market-based securities as well real estate. Yet we also know that the world’s “strongest economy” is not quite as strong as advertised, and that the dollar’s surge against world rivals has already created exporter hardship domestically. For U.S. stocks, go with the momentum that mega-cap growth and Apple have been serving up. That might mean sticking with the stock uptrend via the Vanguard Mega-Cap Growth ETF (NYSEARCA: MGK ), until and unless it falls below and stays below a 200-day trendline. Also consider thematic/satellite holdings such as the PureFunds ISE Cyber Security ETF (NYSEARCA: HACK ). This exchange-traded tracker has been hitting “higher lows” ever since its recent introduction – a bullish technical sign to accompany the high profile concerns of “cyber-terrorism” and “identity theft.” On the flip side of the ledger, “risk-on” U.S. assets need some insurance against a policy mistake by the Fed (e.g.,raising rates too soon, failing to communicate intentions where credibility is lost, etc.). Not only did the trade deficit soar and consumer confidence drop dramatically in January, but corporate earnings and GDP guidance are both being revised downward. This means investors should buy the long treasury bond dips for protection, relative value and price gain potential . Consider buying a fund like the iShares 10-20 Treasury Bond ETF (NYSEARCA: TLH ) on this reversion to its 50-day MA. Finally, there’s reason to believe that, historically speaking, it makes sense to allocate a portion of one’s risk assets to places where valuations are lower than the U.S. It is true that European equities may struggle to make progress as long as the potential for an ugly divorce between Greece and the euro-zone exists. That said, if a path forward buys time for Greece and, by extension, Spain and Italy, export superstars in the euro-zone should profit immensely from the decimated regional currency. Many of my clients hold the iShares Currency Hedged MSCI Germany ETF (NYSEARCA: HEWG ) or the WisdomTree Europe Hedged Equity ETF (NYSEARCA: HEDJ ) to mitigate the fear of additional euro depreciation. Others might want the other side of that “bet” by picking up the iShares MSCI Germany ETF (NYSEARCA: EWG ). After all, the dollar could fall against the euro if the Fed pushes off interest rate hikes into 2016. Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

The craziness in currency manipulation is occurring on every continent and in every region. So why are these devaluation endeavors happening on such a massive scale? Investors need to take these activities into account in the assessment of risk versus reward. David Bowie and Mick Jagger may believe that people are dancing on every street corner around the world. In actuality, however, they’re desperately competing with neighbors by devaluing their currencies. The craziness in currency manipulation is occurring on every continent and in every region. Japan’s brazen quantitative easing (QE) program has seen the battered yen hurt China’s export-dependent economy, leading to speculation that the People’s Bank of China (PBOC) may need to weaken its yuan. Europe’s recently launched QE program has decimated the euro at the expense of non-member nations. In response, Denmark and Sweden have put forward negative interest rates to keep the Danish krone and Swedish krona from rising against the euro. And in the Americas? Mexico, Peru, Chile and Venezuela have all come under fire from neighboring countries for rate cut activity that has depreciated their respective currencies. So why are these devaluation endeavors happening on such a massive scale? The most obvious reason is the belief that weaker currencies promote exports that will stimulate a nation or region’s economic well-being. In today’s battle, however, strong currencies also force import prices down and that can create deflation. All across the globe, the threat of deflation-based recessionary pressure has caused central banks to loosen monetary policy. Lowering rates to zero percent, “going negative,” buying assets with electronically-created credits (a.k.a. “quantitative easing”) all lead to lower currencies against rivals. Since every major central bank, and even the minor ones, are now engaged in unusual efforts to stimulate respective economies – since everyone is debasing paper money – investors need to take these activities into account in the assessment of risk versus reward. We know that the U.S. Federal Reserve succeeded in reflating the value of market-based securities as well real estate. Yet we also know that the world’s “strongest economy” is not quite as strong as advertised, and that the dollar’s surge against world rivals has already created exporter hardship domestically. For U.S. stocks, go with the momentum that mega-cap growth and Apple have been serving up. That might mean sticking with the stock uptrend via the Vanguard Mega-Cap Growth ETF (NYSEARCA: MGK ), until and unless it falls below and stays below a 200-day trendline. Also consider thematic/satellite holdings such as the PureFunds ISE Cyber Security ETF (NYSEARCA: HACK ). This exchange-traded tracker has been hitting “higher lows” ever since its recent introduction – a bullish technical sign to accompany the high profile concerns of “cyber-terrorism” and “identity theft.” On the flip side of the ledger, “risk-on” U.S. assets need some insurance against a policy mistake by the Fed (e.g.,raising rates too soon, failing to communicate intentions where credibility is lost, etc.). Not only did the trade deficit soar and consumer confidence drop dramatically in January, but corporate earnings and GDP guidance are both being revised downward. This means investors should buy the long treasury bond dips for protection, relative value and price gain potential . Consider buying a fund like the iShares 10-20 Treasury Bond ETF (NYSEARCA: TLH ) on this reversion to its 50-day MA. Finally, there’s reason to believe that, historically speaking, it makes sense to allocate a portion of one’s risk assets to places where valuations are lower than the U.S. It is true that European equities may struggle to make progress as long as the potential for an ugly divorce between Greece and the euro-zone exists. That said, if a path forward buys time for Greece and, by extension, Spain and Italy, export superstars in the euro-zone should profit immensely from the decimated regional currency. Many of my clients hold the iShares Currency Hedged MSCI Germany ETF (NYSEARCA: HEWG ) or the WisdomTree Europe Hedged Equity ETF (NYSEARCA: HEDJ ) to mitigate the fear of additional euro depreciation. Others might want the other side of that “bet” by picking up the iShares MSCI Germany ETF (NYSEARCA: EWG ). After all, the dollar could fall against the euro if the Fed pushes off interest rate hikes into 2016. Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

Scalper1 News