Scalper1 News

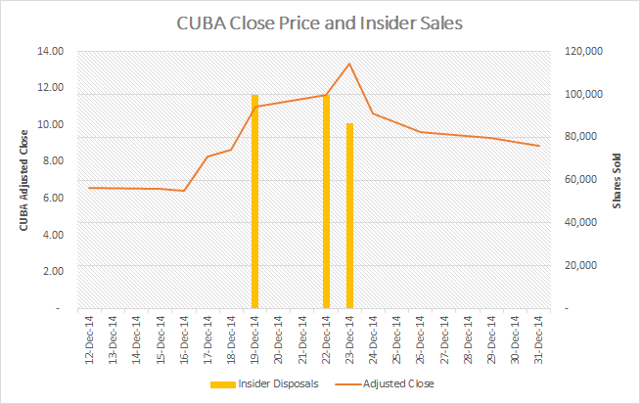

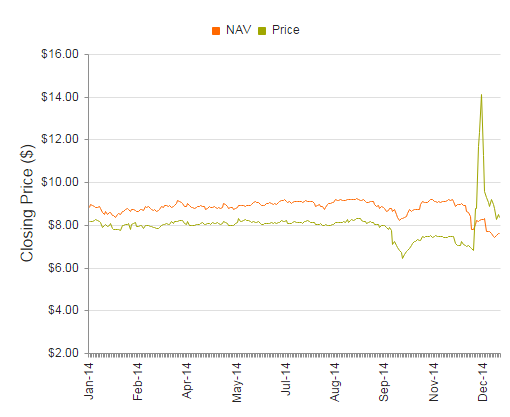

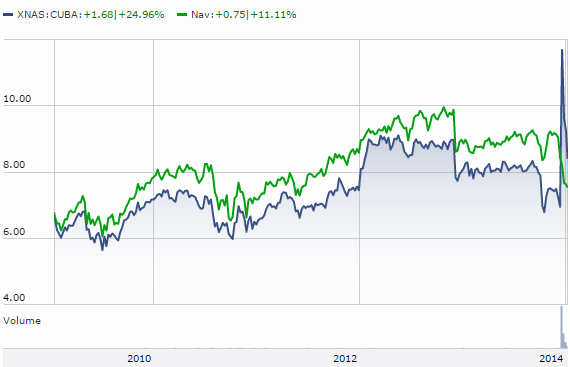

Summary ETFs and CEFs that track emerging market economies are often popular with foreign investors because they mitigate some risks of owning foreign equities such as accessibility, liquidity and local governance. However, emerging economies often have substantial risks that cannot be priced out by convenience, so these funds usually trade at a discount to their NAV. Occasionally, irrational exuberance will elevate an ETF or CEF above its NAV, creating an arbitrage opportunity. The CEF CUBA has been steadily returning to normalcy after a zealous run following President Obama’s Cuban Diplomacy announcement; ~20% profit potential is still on the table. Business As Usual Exchange traded funds (ETFs) and closed end funds (CEFs) are convenient – one can buy a single asset and have a basket of exposure. ETFs and CEFs can be especially useful when they track foreign stock markets. They can mitigate a host of risk factors, such as accessibility to a foreign stock market, the liquidity of foreign equities, and local governance’s barriers to entry for foreign capital. (Sourced from Google via Barclays ) While ETFs and CEFs can neatly catalog foreign equities into a convenient bundle, risks inherent to emerging markets remain. Currency woes, inflation battles, corruption – the list isn’t a short one. Therefore, it is rather common for ETFs and CEFs to trade at a discount to their net asset value (NAV). This is a combination of risk premium as well as management and expense fees. Typically the spread between a fund’s NAV and its tick price – its discount/premium – is fairly constant. EM risk factors and management fees are generally sticky, so there isn’t much reason for the spread to fluctuate. However, an exogenous event can distort the discount, even turning it into a premium. This creates potential arbitrage opportunities. Business Is… Unusual Three and a half weeks ago, President Obama ordered a return to full diplomatic relations with Cuba. While a significant departure from the decades old stalemate, significant hurdles remain. In particular, the 54-year-old trade embargo remains. (Source: Daily Mail UK ) This highly unexpected event ignited an energetic rally in any equity with even loose ties to Cuba or the Caribbean. The Herzfeld Caribbean Basin Closed End Fund (NASDAQ: CUBA ) was one such beneficiary. At one point, it traded nearly 50% above its NAV. Now that the political reality is beginning to sink in, CUBA’s premium has seen a steady reduction. However, it is still trading well above a rational value and the spread can be approximately arbitraged out, creating a nearly risk-free investment. The Nuts And Bolts Despite its suggestive ticker, the CUBA CEF is not relegated to Cuban assets (something that would be nearly impossible); in fact, it isn’t even meant to mimic the Cuban economy in particular. To quote from the fund management’s website : The Herzfeld Caribbean Basin Fund’s investment objective is long-term capital appreciation. To achieve its objective, the Fund invests in issuers that are likely, in the Advisor’s view, to benefit from economic, political, structural and technological developments in the countries in the Caribbean Basin, which consist of Cuba, Jamaica, Trinidad and Tobago, the Bahamas, the Dominican Republic, Barbados, Aruba, Haiti, the Netherlands Antilles, the Commonwealth of Puerto Rico, Mexico, Honduras, Guatemala, Belize, Costa Rica, Panama, Colombia and Venezuela. The fund invests at least 80% of its total assets in a broad range of securities of issuers including U.S.-based companies that engage in substantial trade with, and derive substantial revenue from, operations in the Caribbean Basin Countries. Since the fund’s investment scope has a loose mandate, let’s see what some of the actual assets are: CUBA Top 25 Holdings Company Ticker CUBA Weight Country Copa Holdings CPA 8.46% United States MasTec Inc MTZ 6.28% United States Coca-Cola Femsa SAB KOF 6.03% Mexico Royal Caribbean RCL 5.34% United States Seaboard Corp SEB 5.17% United States Lennar Corp LEN 4.80% United States Norwegian Cruse Line Holdings NCLH 4.01% United States Banco Latinamericano de Comercio Exterior BLX 3.96% United States Carnival Corporation CCL 3.80% United States Consolidated Water Co CWCO 3.71% United States America Movil AMX 3.44% Mexico BanColombia CIB 3.34% Colombia Watsco Inc WSO 3.24% United States Grupo Televisa TV 2.94% Mexico Chiquita Brands International CQB 2.77% United States Freeport-McMoRan Inc FCX 2.69% United States Fomento Economico Mexicano FMX 2.67% Mexico Cemex CX 2.26% Mexico Steiner Leisure STNR 2.24% United States TECO Energy TE 2.15% United States Norfolk Southern Corp NSC 1.87% United States Wal-Mart de Mexico OTCQX:WMMVY 1.62% Mexico Tahoe Resources Inc THO 1.48% Canada Fresh Del Monte Produce Inc FDP 1.35% United States Atlantic Tele-Network Inc ATNI 1.32% United States (Source: Morningstar ) The above table represents 86.94% of the closed end fund. Fund Insiders Sell Millions Fund insiders were clearly aware of their good fortune – it’s not every day that one’s holdings start to trade nearly 50% above their intrinsic value! Consider the chart below of insider disposals charted behind CUBA’s adjusted close price: (click to enlarge) (Chart created by author; data from SEC , NASDAQ and Yahoo Finance ) The above transactions add up to nearly $4,000,000 of equity disposals. CUBA is worth around $28 million now, so the disposals were of an meaningful magnitude. In fact, with around 3,700,000 common shares outstanding, insiders sold nearly 8% of the entire float. Those transactions were the only sales by insiders in the last 12 months. The Fun Isn’t Over While the boat may have sailed on the astronomical overvaluation of a few weeks ago, there is still plenty of juice left for a mean reversion trade (or for a nearly risk-free approximate arbitrage). The CEF still trades ~11% above its NAV, and that’s cream waiting to be scraped off the top. However, it is entirely reasonable to expect the potential profit to be closer to 20%. Over the past 3 years – including the data distorting recent spike – CUBA has traded at an average discount of 8.70% to its NAV. Over the past six months – inclusive of the recent spike, again – the average discount has been 8.76%. ( Source ) (Source: CEFConnect ) It is reasonable to expect an eventual reversion to the historical discount rate yielding a potential profit of ~20%. Let’s discuss why. Plus Ca Change, Plus C’est La Meme Chose Emerging market funds, whether bundled as an ETF or a CEF, typically trade at a discount to their NAV because of risk premia and management fees. The most recently reported fiscal year saw CUBA with a reported total expense ratio of 2.46%. ( Source ) General risks to emerging market funds apply: currency risks, inflationary tendencies, payments on foreign debt, and corruption, to name a few. Many of CUBA’s holdings are readily accessible for retail investors because they trade either: directly on American exchanges, as ADRs on American exchanges, or OTC. There is no meaningful reason for CUBA to continue to trade above its NAV. The premium is totally resultant from irrational exuberance relating to President Obama’s announcement and traders buying into an investment vehicle that is (superficially) related to the geopolitical news. This is clearly evident when comparing the CEF to its NAV over a long time frame. (Source: Morningstar ) This is not to say that premiums do not occur “often” in CEFs. It is rather regular for eager bidders to push CEFs above their NAV after some unexpected bullish event has occurred. What history tells us about moments like that, though, is that the funds return to their historical trading pattern of NAV discounting because the underlying factors, mentioned earlier, motivating the spread have not changed. Exciting news doesn’t change finance fundamentals – there is no practical reason for an asset to continue to trade above its NAV for an extended period of time – it simply changes the flow of buyers and sellers, which can create a short-term dislocation between ordinary price relationships. How To Play It If one is confident in the continuation of the historical financial relationships such as the ones discussed here, then shorting CUBA is sufficient to manifest that investment view. That would be a mean reversion play and is de facto volatility selling. It makes sense for this situation, considering the recent bout of volatility was caused by an unexpected political event. If one wants to try to arbitrage the relationship, then one would have to buy an approximate basket of weighted equities that CUBA holds and short sell CUBA. Throughout the article I have been saying things like “approximate arbitrage” rather than just arbitrage – that is because there are practical limitations to achieving a pure arbitrage here. While using a mirrored basket of equities limits “risk” in a sense, it is pragmatically problematic and rather cumbersome to do so. One would have to buy ~50 positions and then weigh the individual equities according to the CEF disclosures. To do so correctly one would have to invest a decent chunk of money so as to have a common denominator between individuals positions. There is also the practical problem of information lag – most CEFs report their holdings either quarterly or semiannually. If the fund is actively managed, then one would always have an imperfect basket, regardless of the pains taken to weigh each equity properly. Of course, one could create a basket of Carribbean related assets, and weigh them according to traditional portfolio metrics (as opposed to mirroring CUBA), and assume that the correlation between those two portfolios is “good enough”. In my opinion, short CUBA is “good enough”. Historical norms will return, and CUBA will likely begin to trade at the historical discount of nearly 10% that it has traded at for years. The Opportunity In Summary What happened: Nearly all emerging market closed end funds trade at a discount to their NAV. This relationship is due to EM risk premia and management fees. CUBA is a closed end fund that is currently trading ~10% above its NAV. This premium was recently as high as 50%. The richening of the valuation was catalyzed by President Obama’s announcement of resuming diplomatic relations with Cuba. Expectations: CUBA will return to its historical average discount to NAV of ~8-10%. This leaves about ~20% of juice left in the opportunity. Reasoning CUBA, the CEF, has very indirect exposure to Cuba, the country. This is by no fault of the fund managers – it is nearly impossible (and possibly illegal) to have direct exposure to a communist country that the U.S. forbids nearly all trade with. Therefore, the run up of CUBA was likely a case of benefit-by-association. The political quagmire that is the U.S. congress is highly unlikely to normalize trade relations with Cuba – especially in an efficient manner. This reality will become evident and likely impact Cuba-related equity premiums. Risk premia and relatively high management and expense fees (~2.5% all in) justify a discount to NAV, especially when many of the top holdings in the CEF are easily accessible to U.S. investors. A long CUBA position may be a nice investment one day – basket exposure to the Carribbean is enticing, especially with the long term expectation of Cuban trade with the U.S. However, waiting for the NAV discount to return to initiate such a position is wise, and taking some easy profits while that long-standing relationship returns to normalcy is an appealing opportunity. The downside is nearly non-existent and the upside of 20% makes the opportunity worthwhile. On a closing note, consider this graphic showing emerging market closed end fund discount/premium relationships. See if you can spot the one that’s different. (click to enlarge) (Source: Wall Street Journal ) Additional disclosure: I retain the right to open L/S positions in any equities mentioned. Scalper1 News

Summary ETFs and CEFs that track emerging market economies are often popular with foreign investors because they mitigate some risks of owning foreign equities such as accessibility, liquidity and local governance. However, emerging economies often have substantial risks that cannot be priced out by convenience, so these funds usually trade at a discount to their NAV. Occasionally, irrational exuberance will elevate an ETF or CEF above its NAV, creating an arbitrage opportunity. The CEF CUBA has been steadily returning to normalcy after a zealous run following President Obama’s Cuban Diplomacy announcement; ~20% profit potential is still on the table. Business As Usual Exchange traded funds (ETFs) and closed end funds (CEFs) are convenient – one can buy a single asset and have a basket of exposure. ETFs and CEFs can be especially useful when they track foreign stock markets. They can mitigate a host of risk factors, such as accessibility to a foreign stock market, the liquidity of foreign equities, and local governance’s barriers to entry for foreign capital. (Sourced from Google via Barclays ) While ETFs and CEFs can neatly catalog foreign equities into a convenient bundle, risks inherent to emerging markets remain. Currency woes, inflation battles, corruption – the list isn’t a short one. Therefore, it is rather common for ETFs and CEFs to trade at a discount to their net asset value (NAV). This is a combination of risk premium as well as management and expense fees. Typically the spread between a fund’s NAV and its tick price – its discount/premium – is fairly constant. EM risk factors and management fees are generally sticky, so there isn’t much reason for the spread to fluctuate. However, an exogenous event can distort the discount, even turning it into a premium. This creates potential arbitrage opportunities. Business Is… Unusual Three and a half weeks ago, President Obama ordered a return to full diplomatic relations with Cuba. While a significant departure from the decades old stalemate, significant hurdles remain. In particular, the 54-year-old trade embargo remains. (Source: Daily Mail UK ) This highly unexpected event ignited an energetic rally in any equity with even loose ties to Cuba or the Caribbean. The Herzfeld Caribbean Basin Closed End Fund (NASDAQ: CUBA ) was one such beneficiary. At one point, it traded nearly 50% above its NAV. Now that the political reality is beginning to sink in, CUBA’s premium has seen a steady reduction. However, it is still trading well above a rational value and the spread can be approximately arbitraged out, creating a nearly risk-free investment. The Nuts And Bolts Despite its suggestive ticker, the CUBA CEF is not relegated to Cuban assets (something that would be nearly impossible); in fact, it isn’t even meant to mimic the Cuban economy in particular. To quote from the fund management’s website : The Herzfeld Caribbean Basin Fund’s investment objective is long-term capital appreciation. To achieve its objective, the Fund invests in issuers that are likely, in the Advisor’s view, to benefit from economic, political, structural and technological developments in the countries in the Caribbean Basin, which consist of Cuba, Jamaica, Trinidad and Tobago, the Bahamas, the Dominican Republic, Barbados, Aruba, Haiti, the Netherlands Antilles, the Commonwealth of Puerto Rico, Mexico, Honduras, Guatemala, Belize, Costa Rica, Panama, Colombia and Venezuela. The fund invests at least 80% of its total assets in a broad range of securities of issuers including U.S.-based companies that engage in substantial trade with, and derive substantial revenue from, operations in the Caribbean Basin Countries. Since the fund’s investment scope has a loose mandate, let’s see what some of the actual assets are: CUBA Top 25 Holdings Company Ticker CUBA Weight Country Copa Holdings CPA 8.46% United States MasTec Inc MTZ 6.28% United States Coca-Cola Femsa SAB KOF 6.03% Mexico Royal Caribbean RCL 5.34% United States Seaboard Corp SEB 5.17% United States Lennar Corp LEN 4.80% United States Norwegian Cruse Line Holdings NCLH 4.01% United States Banco Latinamericano de Comercio Exterior BLX 3.96% United States Carnival Corporation CCL 3.80% United States Consolidated Water Co CWCO 3.71% United States America Movil AMX 3.44% Mexico BanColombia CIB 3.34% Colombia Watsco Inc WSO 3.24% United States Grupo Televisa TV 2.94% Mexico Chiquita Brands International CQB 2.77% United States Freeport-McMoRan Inc FCX 2.69% United States Fomento Economico Mexicano FMX 2.67% Mexico Cemex CX 2.26% Mexico Steiner Leisure STNR 2.24% United States TECO Energy TE 2.15% United States Norfolk Southern Corp NSC 1.87% United States Wal-Mart de Mexico OTCQX:WMMVY 1.62% Mexico Tahoe Resources Inc THO 1.48% Canada Fresh Del Monte Produce Inc FDP 1.35% United States Atlantic Tele-Network Inc ATNI 1.32% United States (Source: Morningstar ) The above table represents 86.94% of the closed end fund. Fund Insiders Sell Millions Fund insiders were clearly aware of their good fortune – it’s not every day that one’s holdings start to trade nearly 50% above their intrinsic value! Consider the chart below of insider disposals charted behind CUBA’s adjusted close price: (click to enlarge) (Chart created by author; data from SEC , NASDAQ and Yahoo Finance ) The above transactions add up to nearly $4,000,000 of equity disposals. CUBA is worth around $28 million now, so the disposals were of an meaningful magnitude. In fact, with around 3,700,000 common shares outstanding, insiders sold nearly 8% of the entire float. Those transactions were the only sales by insiders in the last 12 months. The Fun Isn’t Over While the boat may have sailed on the astronomical overvaluation of a few weeks ago, there is still plenty of juice left for a mean reversion trade (or for a nearly risk-free approximate arbitrage). The CEF still trades ~11% above its NAV, and that’s cream waiting to be scraped off the top. However, it is entirely reasonable to expect the potential profit to be closer to 20%. Over the past 3 years – including the data distorting recent spike – CUBA has traded at an average discount of 8.70% to its NAV. Over the past six months – inclusive of the recent spike, again – the average discount has been 8.76%. ( Source ) (Source: CEFConnect ) It is reasonable to expect an eventual reversion to the historical discount rate yielding a potential profit of ~20%. Let’s discuss why. Plus Ca Change, Plus C’est La Meme Chose Emerging market funds, whether bundled as an ETF or a CEF, typically trade at a discount to their NAV because of risk premia and management fees. The most recently reported fiscal year saw CUBA with a reported total expense ratio of 2.46%. ( Source ) General risks to emerging market funds apply: currency risks, inflationary tendencies, payments on foreign debt, and corruption, to name a few. Many of CUBA’s holdings are readily accessible for retail investors because they trade either: directly on American exchanges, as ADRs on American exchanges, or OTC. There is no meaningful reason for CUBA to continue to trade above its NAV. The premium is totally resultant from irrational exuberance relating to President Obama’s announcement and traders buying into an investment vehicle that is (superficially) related to the geopolitical news. This is clearly evident when comparing the CEF to its NAV over a long time frame. (Source: Morningstar ) This is not to say that premiums do not occur “often” in CEFs. It is rather regular for eager bidders to push CEFs above their NAV after some unexpected bullish event has occurred. What history tells us about moments like that, though, is that the funds return to their historical trading pattern of NAV discounting because the underlying factors, mentioned earlier, motivating the spread have not changed. Exciting news doesn’t change finance fundamentals – there is no practical reason for an asset to continue to trade above its NAV for an extended period of time – it simply changes the flow of buyers and sellers, which can create a short-term dislocation between ordinary price relationships. How To Play It If one is confident in the continuation of the historical financial relationships such as the ones discussed here, then shorting CUBA is sufficient to manifest that investment view. That would be a mean reversion play and is de facto volatility selling. It makes sense for this situation, considering the recent bout of volatility was caused by an unexpected political event. If one wants to try to arbitrage the relationship, then one would have to buy an approximate basket of weighted equities that CUBA holds and short sell CUBA. Throughout the article I have been saying things like “approximate arbitrage” rather than just arbitrage – that is because there are practical limitations to achieving a pure arbitrage here. While using a mirrored basket of equities limits “risk” in a sense, it is pragmatically problematic and rather cumbersome to do so. One would have to buy ~50 positions and then weigh the individual equities according to the CEF disclosures. To do so correctly one would have to invest a decent chunk of money so as to have a common denominator between individuals positions. There is also the practical problem of information lag – most CEFs report their holdings either quarterly or semiannually. If the fund is actively managed, then one would always have an imperfect basket, regardless of the pains taken to weigh each equity properly. Of course, one could create a basket of Carribbean related assets, and weigh them according to traditional portfolio metrics (as opposed to mirroring CUBA), and assume that the correlation between those two portfolios is “good enough”. In my opinion, short CUBA is “good enough”. Historical norms will return, and CUBA will likely begin to trade at the historical discount of nearly 10% that it has traded at for years. The Opportunity In Summary What happened: Nearly all emerging market closed end funds trade at a discount to their NAV. This relationship is due to EM risk premia and management fees. CUBA is a closed end fund that is currently trading ~10% above its NAV. This premium was recently as high as 50%. The richening of the valuation was catalyzed by President Obama’s announcement of resuming diplomatic relations with Cuba. Expectations: CUBA will return to its historical average discount to NAV of ~8-10%. This leaves about ~20% of juice left in the opportunity. Reasoning CUBA, the CEF, has very indirect exposure to Cuba, the country. This is by no fault of the fund managers – it is nearly impossible (and possibly illegal) to have direct exposure to a communist country that the U.S. forbids nearly all trade with. Therefore, the run up of CUBA was likely a case of benefit-by-association. The political quagmire that is the U.S. congress is highly unlikely to normalize trade relations with Cuba – especially in an efficient manner. This reality will become evident and likely impact Cuba-related equity premiums. Risk premia and relatively high management and expense fees (~2.5% all in) justify a discount to NAV, especially when many of the top holdings in the CEF are easily accessible to U.S. investors. A long CUBA position may be a nice investment one day – basket exposure to the Carribbean is enticing, especially with the long term expectation of Cuban trade with the U.S. However, waiting for the NAV discount to return to initiate such a position is wise, and taking some easy profits while that long-standing relationship returns to normalcy is an appealing opportunity. The downside is nearly non-existent and the upside of 20% makes the opportunity worthwhile. On a closing note, consider this graphic showing emerging market closed end fund discount/premium relationships. See if you can spot the one that’s different. (click to enlarge) (Source: Wall Street Journal ) Additional disclosure: I retain the right to open L/S positions in any equities mentioned. Scalper1 News

Scalper1 News