Scalper1 News

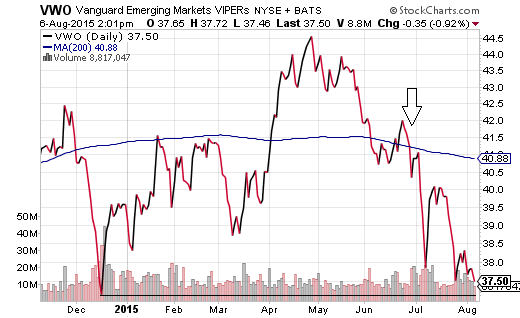

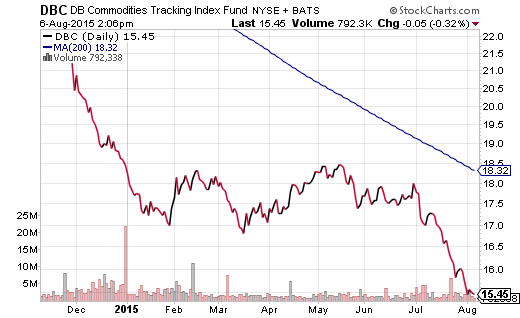

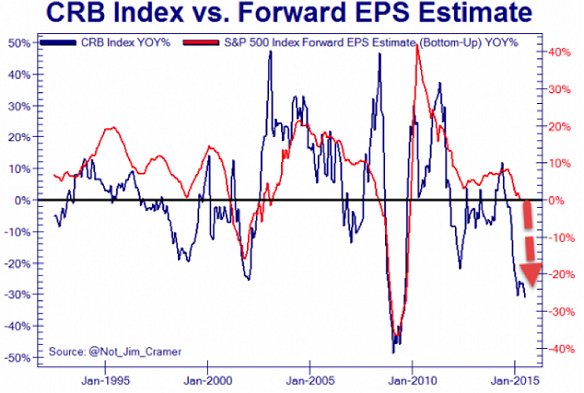

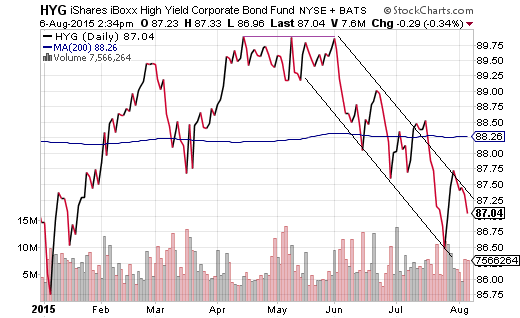

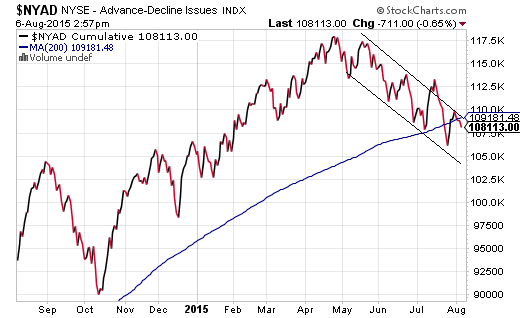

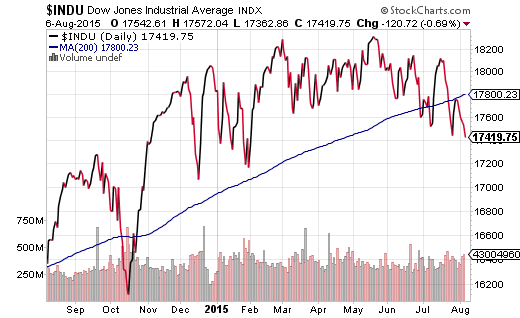

Investors tend to ignore financial markets until they really start to move significantly in one direction or the other. Ironically, investors who wait to buy undervalued securities when the technical backdrop is dramatically improving tend to miss out on sensible risk-taking opportunities. Don’t let the flatness fool you; risk-taking is subsiding and risk-aversion is gaining. More than a handful of people asked me if I would be watching the big debate. 10 candidates. One stage. Which politician will emerge as the clear-cut favorite to win the Republican party nomination? It may surprise some folks, but I have zero interest in the made-for-television event. Each individual will receive about as much air time as Bethe Correia earned in her UFC Title fight against Ronda Rousey. (America’s superstar dropped the Brazilian fighter in 34 seconds.) From my vantage point, a debate exists when two individuals (or two unique groups) express vastly different opinions. And I would be intrigued by an actual match-up with actual position distinctions. Scores of presidential hopefuls from one side of the aisle looking to land a sound byte? I’d rather watch multiple reruns of ESPN’s SportsCenter. In other words, I will tune in when it’s Walker v. Kasich and Hillary versus Joe. (I am name-dropping, not predicting.) In the same way that I might ignore political theater until it really starts to matter, investors tend to ignore financial markets until they really start to matter. And by really start to matter, I mean move significantly in one direction or the other. Ironically, investors who wait to buy undervalued securities when the technical backdrop is dramatically improving tend to miss out on sensible risk-taking opportunities. In the same vein, those who wait to reduce exposure to extremely overvalued stocks when the technical backdrop is weakening tend to miss out on sensible risk-reduction opportunities. What’s more, theoretical buy-n-holders shift to panicky sellers when the emotional pain of severe losses overwhelm them. Although the Dow is slightly negative in 2015, and the S&P 500 is slightly positive, risk has already been sneaking out the back door. Don’t let the flatness fool you; don’t be misled by ‘journalists’ with political agendas. Risk-taking is subsiding and risk-aversion is gaining. Here are three reasons why risk has been exiting the debate stage: 1. The Recovery Is Stalling . Bad news on the economy had been good news throughout the six-and-a-half year stock bull. The reason? The Fed maintained emergency level policies of quantitative easing (i.e., QE1, QE2, Operation Twist, QE3) as well as zero percent overnight lending rates. Today, however, the Fed desperately wants to flip the narrative such that committee members can claim the economy is healthy enough for rate tightening. The data suggest otherwise. For example, Wednesday’s ADP report of 185,000 jobs in July was 20% lower than July of 2014 a year earlier. It is also the lowest headline ADP number since Q1 2014 when an unusually rough winter shouldered the blame. This goes along with the worst wage growth since data have been kept (0.2%), U-6 unemployment between 10.8% ( BLS ) and 14.6% (Gallup), as well as the lowest percentage of employees participating in the working-aged labor pool (62.7%) since 1977. It gets worse. Factory orders have only experienced month-over-month growth in 3 of the last 12 months. Year-over-year, export activity is down 6.6%. Business spending via capital expenditures – dollars used to acquire or upgrade plants, equipment, property and other physical assets – has plummeted. Corporate revenue (sales) will be negative for the second consecutive quarter, perhaps contracting -3.8% in Q2 per FactSet. What’s more, the Conference Board’s Consumer Confidence sub-indexes are dismal; the future expectations gauge is falling at a faster month-over-month clip than the present situation measure. Consumer spending is sinking as well. In sum, risk aversion as well as outright bearish downturns are frequently associated with recessionary pressures. Is a recession imminent? Maybe not. Yet risk-off movement in the financial markets reflect understandable concerns that the U.S. economy may not be capable of absorbing multiple rounds of Federal Reserve tightening. 2. Commodities Are Tanking . One could easily wrap the commodities picture up into discussions about the U.S. economy. That said, I am pulling the topic out into a separate header because it reflects economic woes around the world. As it stands, the IMF’s most recent projections for global output in 2015 represent the slowest annual ‘expansion’ in four years. And the waning use of raw materials is a big part of the IMF’s anemic outlook as well as the collapse in commodity prices. For a year now, a wide variety of analysts have endeavored to explain the oil price decline in positive terms. They’ve been wrong. Consumers and businesses are not spending their energy savings. Meanwhile, energy companies are abandoning projects, laying off high-paying employees and witnessing a dramatic exodus from their stock shares. The Energy Select Sector SPDR ETF (NYSEARCA: XLE ) has depreciated by more than 30% already. Similarly, many of the world’s emerging markets (and some developed markets) depend upon the extraction of materials and natural resources. Granted, the U.S. stock market has been an island unto itself since 2011. However, no market is an island unto itself indefinitely. The Vanguard FTSE Emerging Markets ETF (NYSEARCA: VWO ) is reaching for 52-week lows. The PowerShares DB Commodity Index Tracking ETF (NYSEARCA: DBC ) is already there. And in the last two U.S. recessions, year-over-year commodity depreciation via the Core CRB Commodity Index led forward S&P earnings estimates significantly lower. 3. ‘Technicals’ Are Faltering . Overvalued equities can become even more overvalued, particularly when authorities are easing the rate reins and/or an economy is expanding at a brisk pace. In fact, expensive stocks often become even pricier before market participants typically become squeamish. Yet current technical data show that – across the entire risk spectrum – the smarter money may be seeking safer pastures. What’s more, authorities are talking about tightening at a time when the economy is not expanding briskly. In the bond market, the spread between the Composite Corporate Bond Rate (CCBR) and the 10-year yield is widening. That is a sign of risk aversion. Similarly, investment grade treasuries are witnessing higher highs and higher lows (bullish) whereas the iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA: HYG ) has seen lower highs and lower lows (bearish). These developments are also signs of risk leaving the room before the elephant. In equities, more stocks in the S&P 500 are below their long-term moving average (200-day) than above them. This is coming form a place where 85% of the components had been in technical uptrends. Historically speaking, this kind of narrowing in market breadth is typically associated with an eventual stock benchmark correction. Additionally, as I had identified in my commentary one week ago , the New York Stock Exchange Advance Decline Line (A/D) has a strong track record as a leading indicator of corrections/bears. It recently crossed below its 200-day for the first time in four years (as it did prior to the euro-zone crisis in 2011). In addition, decliners have been pressuring and outpacing advancers regularly since the beginning of May. Granted, the Dow Jones Industrials (DJI) Average and the Dow Jones Transportations (DJT) Average may not be as important as the S&P 500 in identifying technical breakdowns. (Dow Theorists would disagree with me on that.) Nevertheless, when the DJI and DJT are both signalling the potential for longer-term downtrends, there’s something going on. What’s going on? Risk is quietly tip-toeing off the stage. I’ve been telling folks for several months to rethink partying like it’s 1999 . Otherwise, you may find that you overstayed your welcome and that the punch bowl is empty. Is it too late to ratchet down the risk? Hardly. When sky-high valuations meet with weakness in market internals, a 65% growth/35% income investor might make a strategic shift toward 50% large-cap and mid-cap equity/30% investment-grade income/20% cash. You’ve reduced equity risk by avoiding small companies; you’ve reduced income risk by exiting higher-yielding junk. And you’ve given yourself the cash that put you in the right frame of mind to be able to “buy lower” in the next correction. Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

Investors tend to ignore financial markets until they really start to move significantly in one direction or the other. Ironically, investors who wait to buy undervalued securities when the technical backdrop is dramatically improving tend to miss out on sensible risk-taking opportunities. Don’t let the flatness fool you; risk-taking is subsiding and risk-aversion is gaining. More than a handful of people asked me if I would be watching the big debate. 10 candidates. One stage. Which politician will emerge as the clear-cut favorite to win the Republican party nomination? It may surprise some folks, but I have zero interest in the made-for-television event. Each individual will receive about as much air time as Bethe Correia earned in her UFC Title fight against Ronda Rousey. (America’s superstar dropped the Brazilian fighter in 34 seconds.) From my vantage point, a debate exists when two individuals (or two unique groups) express vastly different opinions. And I would be intrigued by an actual match-up with actual position distinctions. Scores of presidential hopefuls from one side of the aisle looking to land a sound byte? I’d rather watch multiple reruns of ESPN’s SportsCenter. In other words, I will tune in when it’s Walker v. Kasich and Hillary versus Joe. (I am name-dropping, not predicting.) In the same way that I might ignore political theater until it really starts to matter, investors tend to ignore financial markets until they really start to matter. And by really start to matter, I mean move significantly in one direction or the other. Ironically, investors who wait to buy undervalued securities when the technical backdrop is dramatically improving tend to miss out on sensible risk-taking opportunities. In the same vein, those who wait to reduce exposure to extremely overvalued stocks when the technical backdrop is weakening tend to miss out on sensible risk-reduction opportunities. What’s more, theoretical buy-n-holders shift to panicky sellers when the emotional pain of severe losses overwhelm them. Although the Dow is slightly negative in 2015, and the S&P 500 is slightly positive, risk has already been sneaking out the back door. Don’t let the flatness fool you; don’t be misled by ‘journalists’ with political agendas. Risk-taking is subsiding and risk-aversion is gaining. Here are three reasons why risk has been exiting the debate stage: 1. The Recovery Is Stalling . Bad news on the economy had been good news throughout the six-and-a-half year stock bull. The reason? The Fed maintained emergency level policies of quantitative easing (i.e., QE1, QE2, Operation Twist, QE3) as well as zero percent overnight lending rates. Today, however, the Fed desperately wants to flip the narrative such that committee members can claim the economy is healthy enough for rate tightening. The data suggest otherwise. For example, Wednesday’s ADP report of 185,000 jobs in July was 20% lower than July of 2014 a year earlier. It is also the lowest headline ADP number since Q1 2014 when an unusually rough winter shouldered the blame. This goes along with the worst wage growth since data have been kept (0.2%), U-6 unemployment between 10.8% ( BLS ) and 14.6% (Gallup), as well as the lowest percentage of employees participating in the working-aged labor pool (62.7%) since 1977. It gets worse. Factory orders have only experienced month-over-month growth in 3 of the last 12 months. Year-over-year, export activity is down 6.6%. Business spending via capital expenditures – dollars used to acquire or upgrade plants, equipment, property and other physical assets – has plummeted. Corporate revenue (sales) will be negative for the second consecutive quarter, perhaps contracting -3.8% in Q2 per FactSet. What’s more, the Conference Board’s Consumer Confidence sub-indexes are dismal; the future expectations gauge is falling at a faster month-over-month clip than the present situation measure. Consumer spending is sinking as well. In sum, risk aversion as well as outright bearish downturns are frequently associated with recessionary pressures. Is a recession imminent? Maybe not. Yet risk-off movement in the financial markets reflect understandable concerns that the U.S. economy may not be capable of absorbing multiple rounds of Federal Reserve tightening. 2. Commodities Are Tanking . One could easily wrap the commodities picture up into discussions about the U.S. economy. That said, I am pulling the topic out into a separate header because it reflects economic woes around the world. As it stands, the IMF’s most recent projections for global output in 2015 represent the slowest annual ‘expansion’ in four years. And the waning use of raw materials is a big part of the IMF’s anemic outlook as well as the collapse in commodity prices. For a year now, a wide variety of analysts have endeavored to explain the oil price decline in positive terms. They’ve been wrong. Consumers and businesses are not spending their energy savings. Meanwhile, energy companies are abandoning projects, laying off high-paying employees and witnessing a dramatic exodus from their stock shares. The Energy Select Sector SPDR ETF (NYSEARCA: XLE ) has depreciated by more than 30% already. Similarly, many of the world’s emerging markets (and some developed markets) depend upon the extraction of materials and natural resources. Granted, the U.S. stock market has been an island unto itself since 2011. However, no market is an island unto itself indefinitely. The Vanguard FTSE Emerging Markets ETF (NYSEARCA: VWO ) is reaching for 52-week lows. The PowerShares DB Commodity Index Tracking ETF (NYSEARCA: DBC ) is already there. And in the last two U.S. recessions, year-over-year commodity depreciation via the Core CRB Commodity Index led forward S&P earnings estimates significantly lower. 3. ‘Technicals’ Are Faltering . Overvalued equities can become even more overvalued, particularly when authorities are easing the rate reins and/or an economy is expanding at a brisk pace. In fact, expensive stocks often become even pricier before market participants typically become squeamish. Yet current technical data show that – across the entire risk spectrum – the smarter money may be seeking safer pastures. What’s more, authorities are talking about tightening at a time when the economy is not expanding briskly. In the bond market, the spread between the Composite Corporate Bond Rate (CCBR) and the 10-year yield is widening. That is a sign of risk aversion. Similarly, investment grade treasuries are witnessing higher highs and higher lows (bullish) whereas the iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA: HYG ) has seen lower highs and lower lows (bearish). These developments are also signs of risk leaving the room before the elephant. In equities, more stocks in the S&P 500 are below their long-term moving average (200-day) than above them. This is coming form a place where 85% of the components had been in technical uptrends. Historically speaking, this kind of narrowing in market breadth is typically associated with an eventual stock benchmark correction. Additionally, as I had identified in my commentary one week ago , the New York Stock Exchange Advance Decline Line (A/D) has a strong track record as a leading indicator of corrections/bears. It recently crossed below its 200-day for the first time in four years (as it did prior to the euro-zone crisis in 2011). In addition, decliners have been pressuring and outpacing advancers regularly since the beginning of May. Granted, the Dow Jones Industrials (DJI) Average and the Dow Jones Transportations (DJT) Average may not be as important as the S&P 500 in identifying technical breakdowns. (Dow Theorists would disagree with me on that.) Nevertheless, when the DJI and DJT are both signalling the potential for longer-term downtrends, there’s something going on. What’s going on? Risk is quietly tip-toeing off the stage. I’ve been telling folks for several months to rethink partying like it’s 1999 . Otherwise, you may find that you overstayed your welcome and that the punch bowl is empty. Is it too late to ratchet down the risk? Hardly. When sky-high valuations meet with weakness in market internals, a 65% growth/35% income investor might make a strategic shift toward 50% large-cap and mid-cap equity/30% investment-grade income/20% cash. You’ve reduced equity risk by avoiding small companies; you’ve reduced income risk by exiting higher-yielding junk. And you’ve given yourself the cash that put you in the right frame of mind to be able to “buy lower” in the next correction. Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

Scalper1 News